You might also like

- Future of Internet in India ReportDocument56 pagesFuture of Internet in India ReportNASSCOM0% (1)

- Hurun India Future Unicorn 2021 Fina Press ReleaselDocument14 pagesHurun India Future Unicorn 2021 Fina Press ReleaselnikunjbubnaNo ratings yet

- Strategic Analysis of InfosysDocument18 pagesStrategic Analysis of InfosysKeshav NarayanNo ratings yet

- Why Indian Startups Are Failing?Document5 pagesWhy Indian Startups Are Failing?yashmalhotra1998No ratings yet

- TataElxsi Vs LTTS Investyadnya 20210607Document74 pagesTataElxsi Vs LTTS Investyadnya 20210607Financial WisdomNo ratings yet

- Artificial Intelligence Machine Learning Program BrochureDocument20 pagesArtificial Intelligence Machine Learning Program BrochurebiswajitntpcNo ratings yet

- India Staffing - GS (Detailed - Feb 2021)Document45 pagesIndia Staffing - GS (Detailed - Feb 2021)anil1820No ratings yet

- JioDocument44 pagesJioWasimAkram100% (2)

- Healthcare Data - Tracxn Business Model Report - 22 Sep 2020Document162 pagesHealthcare Data - Tracxn Business Model Report - 22 Sep 2020Gautam NatrajanNo ratings yet

- PG 4. Gccs in India - To Be or Not To Be... PG 41. Interview: MR Sashidharan Balasundaram, Isg ResearchDocument52 pagesPG 4. Gccs in India - To Be or Not To Be... PG 41. Interview: MR Sashidharan Balasundaram, Isg ResearchRaghvendra N DhootNo ratings yet

- Haptik Overview IndiaDocument38 pagesHaptik Overview IndiaAdi ShanNo ratings yet

- Semiconductor Industry ReportDocument15 pagesSemiconductor Industry ReportJames Salig Jr.No ratings yet

- IMT Placement Brochure 2011Document60 pagesIMT Placement Brochure 2011Prashant ChaudharyNo ratings yet

- Jio's Marketing Plan & Strategy: Prachi Aggarwal (819020) MBA 2019-21 NiftemDocument12 pagesJio's Marketing Plan & Strategy: Prachi Aggarwal (819020) MBA 2019-21 NiftemPrachi AggarwalNo ratings yet

- M&A Research ReportDocument19 pagesM&A Research ReportoliverNo ratings yet

- NASSCOM-Zinnov-GCCs 3.0-Final-May 2019Document93 pagesNASSCOM-Zinnov-GCCs 3.0-Final-May 2019deepak162162No ratings yet

- A Review On Digital India and Cyber SecurityDocument2 pagesA Review On Digital India and Cyber SecurityvivekNo ratings yet

- Artificial Intelligence in Indian Bankin PDFDocument7 pagesArtificial Intelligence in Indian Bankin PDFAvNo ratings yet

- Fintech in India – Opportunities, Challenges, and AdoptionDocument14 pagesFintech in India – Opportunities, Challenges, and Adoptioncaalokpandey2007No ratings yet

- Growth of Fintech Industry in IndiaDocument4 pagesGrowth of Fintech Industry in Indiasaurabhgupta5798No ratings yet

- State of Healthcare ReportDocument19 pagesState of Healthcare ReportISM Inc.No ratings yet

- Bharti AirtelDocument14 pagesBharti AirtelShweta ChaturvediNo ratings yet

- Tech TrendsDocument19 pagesTech TrendsPeter Kiss0% (1)

- Problem StatementsDocument21 pagesProblem StatementsMahak BansalNo ratings yet

- Incubator Database From WebsiteDocument49 pagesIncubator Database From Websiteankit.g0% (1)

- Artificial Intelligence & Machine Learning: Career GuideDocument18 pagesArtificial Intelligence & Machine Learning: Career Guidekallol100% (1)

- Ites Companies in IndiaDocument7 pagesItes Companies in IndiaYashas PariharNo ratings yet

- Government launches ONDC pilot in 5 Indian cities to revolutionize digital commerceDocument6 pagesGovernment launches ONDC pilot in 5 Indian cities to revolutionize digital commercerishabhNo ratings yet

- Role of Artificial Intelligence (AI) in Marketing: August 2021Document14 pagesRole of Artificial Intelligence (AI) in Marketing: August 2021Ankita SinghNo ratings yet

- Unlock Metaverse Potentials in FinanceDocument11 pagesUnlock Metaverse Potentials in FinanceAbd RahmanNo ratings yet

- Indus Valley Annual Report 2023Document125 pagesIndus Valley Annual Report 2023Acevagner_StonedAceFrehleyNo ratings yet

- BYJU'S BDA Role Helps Students LearnDocument4 pagesBYJU'S BDA Role Helps Students LearnAkshathaNo ratings yet

- I'm currently working as a Machine Learning Engineer at a startup in Bangalore.P1: Can you tell me about your work? What technologies are you using? What kind of projects are you working onDocument51 pagesI'm currently working as a Machine Learning Engineer at a startup in Bangalore.P1: Can you tell me about your work? What technologies are you using? What kind of projects are you working onKaranbir SinghNo ratings yet

- India Skills Report 2015Document28 pagesIndia Skills Report 2015virad25No ratings yet

- CB Insights - Game Changers 2022Document43 pagesCB Insights - Game Changers 2022ngothientaiNo ratings yet

- Case WokasDocument5 pagesCase WokasSudipta SarangiNo ratings yet

- The Future of Semiconductor IndustryDocument2 pagesThe Future of Semiconductor IndustryLearnyzenNo ratings yet

- ISR Report 2023Document112 pagesISR Report 2023Vamsi KrishnaNo ratings yet

- TATA AIA Afava: How Has Been Your 1st Time of JoiningDocument5 pagesTATA AIA Afava: How Has Been Your 1st Time of JoiningShivani raikarNo ratings yet

- Tata ElsxiDocument52 pagesTata ElsxiSUKHSAGAR AGGARWALNo ratings yet

- Office Market Update: Q4 2020: Research ReportDocument20 pagesOffice Market Update: Q4 2020: Research ReportsanthoshNo ratings yet

- Key IT Players in IndiaDocument6 pagesKey IT Players in IndiaprasannaNo ratings yet

- Everest Group - Global In-House Center (GIC) Landscape Annual Report 2018 - CADocument9 pagesEverest Group - Global In-House Center (GIC) Landscape Annual Report 2018 - CAsravan malluNo ratings yet

- Tata Consultancy ServicesDocument5 pagesTata Consultancy ServicesNithin NallusamyNo ratings yet

- Ranking of top Silicon Valley tech companies by sales, profits and market capDocument1 pageRanking of top Silicon Valley tech companies by sales, profits and market capRonn Falling Into BluesNo ratings yet

- Getting Hyped for Your First Day as a PMDocument43 pagesGetting Hyped for Your First Day as a PMjhocigigNo ratings yet

- AI in Focus - The Bank Technology Roadmap PlaybookDocument18 pagesAI in Focus - The Bank Technology Roadmap PlaybookAnasNo ratings yet

- Induction Master Project at UNITECHDocument21 pagesInduction Master Project at UNITECHsatishkakaniNo ratings yet

- MicrosoftDocument20 pagesMicrosoftSagar PatelNo ratings yet

- ListofstartupsDocument53 pagesListofstartupsAppu AkNo ratings yet

- Challenges Faced by Jio as Secondary OperatorDocument24 pagesChallenges Faced by Jio as Secondary Operatorsubhi kesharwaniNo ratings yet

- Marketing Strategy of JioDocument7 pagesMarketing Strategy of JioDeepNo ratings yet

- Digital IndiaDocument3 pagesDigital Indiasuny587No ratings yet

- Insurance Companies in IndiaDocument4 pagesInsurance Companies in IndiaJash DalalNo ratings yet

- India Fintech Report 1640158829Document100 pagesIndia Fintech Report 1640158829Simrita BindraNo ratings yet

- Final Project Report - Rohit KumarDocument38 pagesFinal Project Report - Rohit KumarAnirvan Kumar RoyNo ratings yet

- MJK Investments - ER&D Services ExplainedDocument79 pagesMJK Investments - ER&D Services Explainedశ్యామ్ సుధీర్No ratings yet

- Asia Insurance Market Review ReportDocument52 pagesAsia Insurance Market Review ReportTrung Võ0% (1)

- MEDICI IFR 2020 ReportDocument125 pagesMEDICI IFR 2020 ReportAtul YadavNo ratings yet

- Group 7A - HelpAge IndiaDocument12 pagesGroup 7A - HelpAge IndiaAshutosh PatidarNo ratings yet

- About ICICI Securities LimitedDocument2 pagesAbout ICICI Securities LimitedAshutosh PatidarNo ratings yet

- About ICICI Securities LimitedDocument1 pageAbout ICICI Securities LimitedAshutosh PatidarNo ratings yet

- Please Affix Your Latest Passport Sizes Photo HereDocument4 pagesPlease Affix Your Latest Passport Sizes Photo HereAshutosh PatidarNo ratings yet

- Group 07: Managing Non ProfitDocument12 pagesGroup 07: Managing Non ProfitAshutosh PatidarNo ratings yet

- Realty and The Second Wave: SpeakersDocument23 pagesRealty and The Second Wave: SpeakersAshutosh PatidarNo ratings yet

- 18may 2021 - India - DailyDocument105 pages18may 2021 - India - DailyAshutosh PatidarNo ratings yet

- Larsen & Toubro Strong Operating Performance and Balance SheetDocument32 pagesLarsen & Toubro Strong Operating Performance and Balance SheetAshutosh PatidarNo ratings yet

- FAME Booklet - FIDD Central Office PDFDocument40 pagesFAME Booklet - FIDD Central Office PDFHitendra PanchalNo ratings yet

- RUR Group4 ProductIdeaDocument7 pagesRUR Group4 ProductIdeaAshutosh PatidarNo ratings yet

- SSAVAJ PosterDocument1 pageSSAVAJ PosterAshutosh PatidarNo ratings yet

- Pre Read Material-Introduction To FRADocument11 pagesPre Read Material-Introduction To FRAAshutosh PatidarNo ratings yet

- Pre Read Business DesignDocument1 pagePre Read Business DesignAshutosh PatidarNo ratings yet

- Pre-Read Video MakingDocument4 pagesPre-Read Video MakingAshutosh PatidarNo ratings yet

- Case 1 - John HigginsDocument4 pagesCase 1 - John HigginsSanjeev ManekNo ratings yet

- Case 1 - John HigginsDocument4 pagesCase 1 - John HigginsSanjeev ManekNo ratings yet

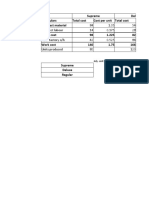

- 84 1.05 54 B. Direct Labour 14 0.175 28 Add: Factory O/h 42 0.525 84 Units Produced 80 120Document6 pages84 1.05 54 B. Direct Labour 14 0.175 28 Add: Factory O/h 42 0.525 84 Units Produced 80 120Ashutosh PatidarNo ratings yet

- STATE LAND INVESTMENT CORPORATION V. COMMISSIONER OF INTERNAL REVENUEDocument5 pagesSTATE LAND INVESTMENT CORPORATION V. COMMISSIONER OF INTERNAL REVENUEMary Louisse Rulona100% (1)

- TCS Configuration PDFDocument20 pagesTCS Configuration PDFrishisap2No ratings yet

- Chapter 4 Canadian Constitutional Law IntroDocument62 pagesChapter 4 Canadian Constitutional Law Introapi-241505258No ratings yet

- Sharon Pearson For Oberlin City CouncilDocument2 pagesSharon Pearson For Oberlin City CouncilThe Morning JournalNo ratings yet

- Requirements For Marriage Licenses in El Paso County, Texas: Section 2.005. See Subsections (B 1-19)Document2 pagesRequirements For Marriage Licenses in El Paso County, Texas: Section 2.005. See Subsections (B 1-19)Edgar vallesNo ratings yet

- Project Management - Harvard Management orDocument68 pagesProject Management - Harvard Management ortusharnbNo ratings yet

- Case Study - Generative AI Applications in Key IndustriesDocument2 pagesCase Study - Generative AI Applications in Key Industriessujankumar2308No ratings yet

- Filtro Tambor RotatorioDocument4 pagesFiltro Tambor Rotatoriocquibajo100% (2)

- Beth Moore Part 2Document3 pagesBeth Moore Part 2elizabeth_prata_1No ratings yet

- Assignment On Procurement and Contract AdministrationDocument5 pagesAssignment On Procurement and Contract Administrationasterayemetsihet87No ratings yet

- And of Clay We Are CreatedDocument10 pagesAnd of Clay We Are CreatedDaniela Villarreal100% (1)

- UK Automotive Composites Supply Chain Study Public Summary 2Document31 pagesUK Automotive Composites Supply Chain Study Public Summary 2pallenNo ratings yet

- DH 4012286Document5 pagesDH 4012286Edwin KurniawanNo ratings yet

- Rephrasingtranslation 2º BachDocument2 pagesRephrasingtranslation 2º BachJessie WattsNo ratings yet

- Health - Mandate Letter - FINAL - SignedDocument4 pagesHealth - Mandate Letter - FINAL - SignedCTV CalgaryNo ratings yet

- Assessing Contribution of Research in Business To PracticeDocument5 pagesAssessing Contribution of Research in Business To PracticeAga ChindanaNo ratings yet

- IataDocument2,002 pagesIataJohn StanleyNo ratings yet

- Lean Management Tools: Presented By: Theresa Moore Thedacare Improvement SystemDocument42 pagesLean Management Tools: Presented By: Theresa Moore Thedacare Improvement SystemPradeep Poornishankar PNo ratings yet

- RRTK Historical ListsDocument52 pagesRRTK Historical ListsJMMPdos100% (3)

- Finance 5Document3 pagesFinance 5Jheannie Jenly Mia SabulberoNo ratings yet

- Attitude StrengthDocument3 pagesAttitude StrengthJoanneVivienSardinoBelderolNo ratings yet

- Chapter 3Document9 pagesChapter 3Safitri Eka LestariNo ratings yet

- Wind BandDocument19 pagesWind BandRokas Põdelis50% (2)

- In A Grove PDFDocument9 pagesIn A Grove PDFsheelaNo ratings yet

- Jack Miles Discusses New Book "God in the Qur'anDocument1 pageJack Miles Discusses New Book "God in the Qur'anKazi Galib100% (1)

- "Wealth Builder": Mr. Rahul SharmaDocument5 pages"Wealth Builder": Mr. Rahul Sharmakrishna-almightyNo ratings yet

- Republic of the Philippines Batangas State University Taxation and Land Reform ExamDocument5 pagesRepublic of the Philippines Batangas State University Taxation and Land Reform ExamMeynard MagsinoNo ratings yet

- Chapter 1 1Document4 pagesChapter 1 1Arhann Anthony Almachar Adriatico67% (3)

- LLF 2017 ProgramDocument2 pagesLLF 2017 ProgramFasih Ahmed100% (2)

- Japan Coal Phase-Out: The Path to Phase-Out by 2030Document24 pagesJapan Coal Phase-Out: The Path to Phase-Out by 2030LuthfanNo ratings yet