You might also like

- Bizmates Trainers' Briefing On BIR ComplianceDocument8 pagesBizmates Trainers' Briefing On BIR Compliancejoahnabulanadi100% (2)

- Your RBC Personal Savings Account StatementDocument1 pageYour RBC Personal Savings Account Statementmilad safiNo ratings yet

- ANSWER KEY Adjustments Quiz 2Document6 pagesANSWER KEY Adjustments Quiz 2Christine Mae BurgosNo ratings yet

- Credit DerivativeDocument5 pagesCredit DerivativedomomwambiNo ratings yet

- Chapter 3 Adjusting The Accounts PDFDocument56 pagesChapter 3 Adjusting The Accounts PDFJed Riel BalatanNo ratings yet

- Financing Mining Projects PDFDocument7 pagesFinancing Mining Projects PDFEmil AzhibayevNo ratings yet

- Partnership LiquidationDocument5 pagesPartnership LiquidationChristian PaulNo ratings yet

- Hull OFOD10e MultipleChoice Questions and Answers Ch07Document7 pagesHull OFOD10e MultipleChoice Questions and Answers Ch07Kevin Molly KamrathNo ratings yet

- Bailment: (Pactum de Commodando)Document19 pagesBailment: (Pactum de Commodando)Jerry YanNo ratings yet

- I. True or False: Pre TestDocument18 pagesI. True or False: Pre TestErina SmithNo ratings yet

- Adjusting The Book of AccountsDocument33 pagesAdjusting The Book of Accountsjoshua zabala100% (1)

- ACC101 Quiz Test 2 STDocument6 pagesACC101 Quiz Test 2 STNguyen Thi Kim ChuyenNo ratings yet

- Activity 6 - Adjusting Entries - Depreciation (Ans)Document5 pagesActivity 6 - Adjusting Entries - Depreciation (Ans)angela flores100% (1)

- Adjusting Entries ExampleDocument5 pagesAdjusting Entries ExampleSiak Ni LynnLadyNo ratings yet

- Lesson 1 ExtendDocument6 pagesLesson 1 ExtendRoel Cababao50% (2)

- 12 - Tolentino V GonzalesDocument3 pages12 - Tolentino V GonzalesAthanasia Zoe Gonzales100% (2)

- C. Identification, Recording, Communication.: ExceptDocument9 pagesC. Identification, Recording, Communication.: ExceptSylvia Al-a'maNo ratings yet

- ADDU Worksheet, FS, CJE and EtcDocument67 pagesADDU Worksheet, FS, CJE and EtcKen BorjaNo ratings yet

- FABM Assignment WS FS P C TB 1Document34 pagesFABM Assignment WS FS P C TB 1memae0044No ratings yet

- 2021 FAR Straight Problem - Hyc2Document2 pages2021 FAR Straight Problem - Hyc2Mariecris BatasNo ratings yet

- Accounting 1Document117 pagesAccounting 1Mary Alyssa Claire Capate II100% (1)

- PDF Journal Entries Tradingdocx CompressDocument79 pagesPDF Journal Entries Tradingdocx CompressMaskter TwinsetsNo ratings yet

- Theory of AccountDocument1 pageTheory of Accountzee abadilla100% (1)

- Accounting For A Service CompanyDocument9 pagesAccounting For A Service CompanyAnnie RapanutNo ratings yet

- Mr. Lindbergh Lendl S. Soriano Practice Set 2Document33 pagesMr. Lindbergh Lendl S. Soriano Practice Set 2Kevin MagdayNo ratings yet

- Adjustments Quiz 2Document6 pagesAdjustments Quiz 2Loey ParkNo ratings yet

- 2.0assessment ExamDocument2 pages2.0assessment ExamyeshaNo ratings yet

- Lesson 21 - Closing Entries, Post-Closing, Trial Balance and Reversing EntriesDocument8 pagesLesson 21 - Closing Entries, Post-Closing, Trial Balance and Reversing EntriesMayeng MonayNo ratings yet

- Chapter 3 Basic AccountingDocument35 pagesChapter 3 Basic AccountingDeanna LuiseNo ratings yet

- 162 001Document1 page162 001Christian Mark AbarquezNo ratings yet

- Comprehensive ProblemDocument1 pageComprehensive ProblemDavid Con RiveroNo ratings yet

- Effects of Transactions Instructions: Indicate The Effects of Each Transaction by Writing The ChoicesDocument1 pageEffects of Transactions Instructions: Indicate The Effects of Each Transaction by Writing The ChoicesHessiel Mae Jumalon Garcines100% (1)

- Cost Accounting Midterm ExamDocument37 pagesCost Accounting Midterm Examshynebright.phNo ratings yet

- Accounting ExercisesDocument41 pagesAccounting ExercisesKayla MirandaNo ratings yet

- Module 2 - Completing The Accounting CycleDocument45 pagesModule 2 - Completing The Accounting CycleShane TorrieNo ratings yet

- Chapter 5 Double Entry Bookkeeping For A Service ProviderDocument8 pagesChapter 5 Double Entry Bookkeeping For A Service ProviderPaw Verdillo100% (1)

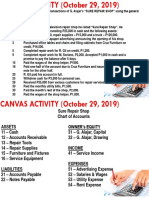

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- JE, GL, TB Magpantay RevisedDocument22 pagesJE, GL, TB Magpantay RevisedJasmine Acta100% (1)

- Santos ChaDocument18 pagesSantos ChaSANTOS, CHARISH ANNNo ratings yet

- FSDocument44 pagesFSMaria Beatriz Aban Munda100% (2)

- Inventory Sample ProblemDocument2 pagesInventory Sample ProblemJohn Rey Bantay RodriguezNo ratings yet

- Acctg Equation and Journal EntriesDocument3 pagesAcctg Equation and Journal EntriesNiño Dwayne TuboNo ratings yet

- Journalizing To Adjusting Entries QuizDocument3 pagesJournalizing To Adjusting Entries QuizNemar Jay Capitania100% (1)

- Set IDocument2 pagesSet IAdoree RamosNo ratings yet

- Basic Accounting ModelDocument3 pagesBasic Accounting Modeldlinds2X1No ratings yet

- 2 Abm Fabm2 12 W2 3 Melc 4 1Document9 pages2 Abm Fabm2 12 W2 3 Melc 4 1Rializa Caro BlanzaNo ratings yet

- Accounting CycleDocument21 pagesAccounting CycleJc GappiNo ratings yet

- Problem 3 ACCA101Document3 pagesProblem 3 ACCA101Nicole FidelsonNo ratings yet

- Tutorial Week 6Document7 pagesTutorial Week 6Mai Hoàng100% (1)

- Journalizing Merchandising TransactionsDocument3 pagesJournalizing Merchandising TransactionsMarian Augelio PolancoNo ratings yet

- Financial Accounting and ReportingDocument1 pageFinancial Accounting and ReportingPaula BautistaNo ratings yet

- Semis 1 WorksheetDocument15 pagesSemis 1 WorksheetDexter BangayanNo ratings yet

- Basic Accounting Equation ExercisesDocument7 pagesBasic Accounting Equation ExerciseshIgh QuaLIty SVT100% (1)

- Lesson 7.1 - AJE Accrued ExpensesDocument22 pagesLesson 7.1 - AJE Accrued ExpensesYra Dominique ChuaNo ratings yet

- Partnership OperationDocument3 pagesPartnership OperationShane NayahNo ratings yet

- Exam Questionaire in IntermediateDocument5 pagesExam Questionaire in IntermediateJester IlaganNo ratings yet

- Midterm 2nd 3rd Meeting RevisedDocument6 pagesMidterm 2nd 3rd Meeting RevisedChristopher CristobalNo ratings yet

- Answer Key - Chapter 6 - ACCOUNTING1Document19 pagesAnswer Key - Chapter 6 - ACCOUNTING1IL MareNo ratings yet

- ACTIVITY 2-Fundamentals of Accounting 1Document1 pageACTIVITY 2-Fundamentals of Accounting 1shelou_domantay100% (1)

- Basic Acctg 4th SatDocument11 pagesBasic Acctg 4th SatJerome Eziekel Posada PanaliganNo ratings yet

- Darantan, KC T. - FAR Module 6Document3 pagesDarantan, KC T. - FAR Module 6Li LiNo ratings yet

- List Accounting 2 2013Document5 pagesList Accounting 2 2013Ondoy PorlaresNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument2 pagesAccounting Cycle of A Merchandising BusinessAnne Alag100% (1)

- Accounting ReviewerDocument21 pagesAccounting ReviewerAdriya Ley PangilinanNo ratings yet

- Pilar Company Bank Reconciliation Statement SEPTEMBER 30, 2020 Balance Per Bank Statement Add: Deposit in Transit Receipts Not Yet Deposited Total: P139,314.20 Deduct: Outstanding ChecksDocument16 pagesPilar Company Bank Reconciliation Statement SEPTEMBER 30, 2020 Balance Per Bank Statement Add: Deposit in Transit Receipts Not Yet Deposited Total: P139,314.20 Deduct: Outstanding ChecksStudent Core GroupNo ratings yet

- Activity 2 - Cash and Cash EquivalentsDocument2 pagesActivity 2 - Cash and Cash EquivalentsSean Lester S. NombradoNo ratings yet

- Sep 2022 - Current Acc 30681946Document17 pagesSep 2022 - Current Acc 30681946Linella LinellaNo ratings yet

- Asish PMDocument59 pagesAsish PMAryan Sharma54No ratings yet

- SBI & BMB MergerDocument12 pagesSBI & BMB MergerShubham naharwal (PGDM 17-19)No ratings yet

- Tianjin PlasticsDocument19 pagesTianjin PlasticsruccaruNo ratings yet

- Cgi DD XML MappingDocument3 pagesCgi DD XML MappingRajendra PilludaNo ratings yet

- 5 Deposit ProductsDocument19 pages5 Deposit ProductsLAMOUCHI RIMNo ratings yet

- BoholDocument11 pagesBoholLevi L. BinamiraNo ratings yet

- Vanguard Acct Xfer Forms 06 PDFDocument62 pagesVanguard Acct Xfer Forms 06 PDFwlamillerNo ratings yet

- Cashback Redemption FormDocument1 pageCashback Redemption FormPapuKaliyaNo ratings yet

- Introduction YES BankDocument29 pagesIntroduction YES Bankparag03No ratings yet

- E - Commerce Chapter 11Document19 pagesE - Commerce Chapter 11Md. RuHul A.No ratings yet

- MBF Homework 5Document19 pagesMBF Homework 5JerryNo ratings yet

- State Bank of India - VaibhavDocument1 pageState Bank of India - VaibhavVaibhav GuptaNo ratings yet

- Jorion VaR DisclosuresDocument35 pagesJorion VaR DisclosuresMatheus Monteiro RossaNo ratings yet

- Book ReportDocument4 pagesBook ReportMarivicTalomaNo ratings yet

- My ResumeDocument2 pagesMy Resumeanon-477710No ratings yet

- International Escorted Group Tours 2014Document208 pagesInternational Escorted Group Tours 2014Prabhat JainNo ratings yet

- Hsslive XII Comp Accounting Model Practical Book Binoy PDFDocument56 pagesHsslive XII Comp Accounting Model Practical Book Binoy PDFSusmitha kNo ratings yet

- KrazyBee Services Private LimitedDocument9 pagesKrazyBee Services Private LimitedBalakrishnan IyerNo ratings yet

- 65 Less YearsDocument5 pages65 Less YearsBhanu Pratap Singh YadavNo ratings yet

- Checklist Japan Visa Application PDFDocument3 pagesChecklist Japan Visa Application PDFRossanne TagabanNo ratings yet

- Financial TheoryDocument21 pagesFinancial Theoryমুসফেকআহমেদনাহিদ0% (1)