You might also like

- Fringe Benefit TaxDocument11 pagesFringe Benefit TaxJonard Godoy75% (4)

- Bsa1202 FS2122 Incometax 04Document9 pagesBsa1202 FS2122 Incometax 04Katring O.No ratings yet

- Chapter 3Document88 pagesChapter 3giezele ballatanNo ratings yet

- Module 3.1 Fringe Benefits and de Minimis BenefitsDocument4 pagesModule 3.1 Fringe Benefits and de Minimis BenefitsGabs SolivenNo ratings yet

- Far Eastern University - Manila Income Taxation TAX1101 Fringe Benefit TaxDocument10 pagesFar Eastern University - Manila Income Taxation TAX1101 Fringe Benefit TaxRyan Christian BalanquitNo ratings yet

- Tax exempt fringe benefitsDocument11 pagesTax exempt fringe benefitskenshin sclanimirNo ratings yet

- Fringe Benefits TaxationDocument12 pagesFringe Benefits TaxationKaila Mae Tan DuNo ratings yet

- Chapter 3 Fringe & de Minimis BenefitsDocument6 pagesChapter 3 Fringe & de Minimis BenefitsNovelyn Hiso-anNo ratings yet

- Withholding Tax GuideDocument6 pagesWithholding Tax GuideAnselmo Rodiel IVNo ratings yet

- Income-Taxation 3Document44 pagesIncome-Taxation 3Maria Maganda MalditaNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- 06 Gross IncomeDocument103 pages06 Gross IncomeJSNo ratings yet

- Fringe Benefit Tax 2Document20 pagesFringe Benefit Tax 2shpo.porras.uiNo ratings yet

- Week 3 Intro - To Tax 2023 24 Part 1Document28 pagesWeek 3 Intro - To Tax 2023 24 Part 1Arellano Rhovic R.No ratings yet

- Fringe Benefits TaxDocument3 pagesFringe Benefits TaxGrace EspirituNo ratings yet

- Updated RR 2-98 Sec 2.78.1 (A) CompensationDocument5 pagesUpdated RR 2-98 Sec 2.78.1 (A) CompensationJaymar DetoitoNo ratings yet

- Fringe Benefits, de Minimis, Convenience of EmployerDocument2 pagesFringe Benefits, de Minimis, Convenience of Employerlossesabound100% (1)

- Bam031 Income Taxation P2 NotesDocument8 pagesBam031 Income Taxation P2 NotesRyan Malanum AbrioNo ratings yet

- ACP Allowable Deductions Under Philippine Tax LawDocument20 pagesACP Allowable Deductions Under Philippine Tax LawRon Ramos100% (1)

- 2018-Train ActDocument65 pages2018-Train ActAnthonette ManagaytayNo ratings yet

- Gross Income Inc Exc DedDocument9 pagesGross Income Inc Exc DedMelbert BallaraNo ratings yet

- Fringe BenefitsDocument5 pagesFringe BenefitsJune Romeo ObiasNo ratings yet

- Tax Treatment of Fringe Benefits in The PhilippinesDocument7 pagesTax Treatment of Fringe Benefits in The PhilippinesGerard Nelson ManaloNo ratings yet

- De-Minimis-Benefits-2024Document1 pageDe-Minimis-Benefits-2024Love Heart BantilesNo ratings yet

- Chapter 03 Fringe Benefit TaxDocument42 pagesChapter 03 Fringe Benefit TaxVisperas, Jana Mae U.No ratings yet

- De Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosDocument3 pagesDe Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosKathNo ratings yet

- Fringe Benefits in The PhilippinesDocument4 pagesFringe Benefits in The PhilippinesMarivie Uy100% (1)

- Gross Income: Learning ObjectivesDocument12 pagesGross Income: Learning ObjectivesClaire BarbaNo ratings yet

- Wala LangDocument5 pagesWala LangHOSPITAL EMERGENCY ROOMNo ratings yet

- Northern CPAR: Taxation - Fringe Benefit Taxation: Rex B. Banggawan, Cpa, MbaDocument7 pagesNorthern CPAR: Taxation - Fringe Benefit Taxation: Rex B. Banggawan, Cpa, MbaLouiseNo ratings yet

- Taxation Module 3 5Document57 pagesTaxation Module 3 5Ma VyNo ratings yet

- Tax Chapter 10, 11, 12Document13 pagesTax Chapter 10, 11, 12Sheraldine MendozaNo ratings yet

- Special Treatment of Fringe BenefitsDocument20 pagesSpecial Treatment of Fringe BenefitsMartin EstreraNo ratings yet

- Fringe BenefitsDocument5 pagesFringe BenefitsZandra LeighNo ratings yet

- Fringe Benefit TaxDocument30 pagesFringe Benefit Taxrav danoNo ratings yet

- Tax Treatment of Fringe Benefits for EmployeesDocument13 pagesTax Treatment of Fringe Benefits for EmployeesAngela Nicole Nobleta100% (2)

- Chapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitDocument8 pagesChapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitMARIA BELEN GUTIERREZNo ratings yet

- 1601 CDocument8 pages1601 CMhyckee GuinoNo ratings yet

- Importance of Withholding Tax SystemDocument7 pagesImportance of Withholding Tax SystemALAJID, KIM EMMANUELNo ratings yet

- Module 6 TaxDocument6 pagesModule 6 TaxEunice OriasNo ratings yet

- The Proceeds of Life Insurance Policies They Do The Heirs or Beneficiaries Upon Death of The Insured Shall Be Exempt From Income TaxDocument18 pagesThe Proceeds of Life Insurance Policies They Do The Heirs or Beneficiaries Upon Death of The Insured Shall Be Exempt From Income TaxXhien YeeNo ratings yet

- Gross Income RRsDocument27 pagesGross Income RRsslumbaNo ratings yet

- RR No. 8 2018Document35 pagesRR No. 8 2018zul fanNo ratings yet

- Tax Treatments of Fringe BenefitsDocument63 pagesTax Treatments of Fringe BenefitsAdmNo ratings yet

- Tax Treatments of Fringe BenefitsDocument14 pagesTax Treatments of Fringe BenefitsAdmNo ratings yet

- DRAFT REVENUE REGULATIONS IMPLEMENT TRAIN LAWDocument25 pagesDRAFT REVENUE REGULATIONS IMPLEMENT TRAIN LAWGenesis ManaliliNo ratings yet

- Legal Opinion de MinimisDocument6 pagesLegal Opinion de MinimisjoyiveeongNo ratings yet

- Tax Guide for Minimum Wage Earners and IndividualsDocument41 pagesTax Guide for Minimum Wage Earners and IndividualsAllan BacudioNo ratings yet

- RR No. 10-2008Document37 pagesRR No. 10-2008Kristan John ZernaNo ratings yet

- Revenue Regulations 10-2008Document43 pagesRevenue Regulations 10-2008mary lou100% (29)

- FringeDocument7 pagesFringeJoyce Anne TilanNo ratings yet

- BIR How To Compute Fringe Benefit Tax REL PARTYDocument69 pagesBIR How To Compute Fringe Benefit Tax REL PARTYRyoNo ratings yet

- TAXATION OF EMPLOYEE INCOMEDocument6 pagesTAXATION OF EMPLOYEE INCOMEShane Mark CabiasaNo ratings yet

- Revenue Regulations (RR) No 10-08Document0 pagesRevenue Regulations (RR) No 10-08sj_adenipNo ratings yet

- FS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoDocument11 pagesFS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- Taxation I - Part Ii Compilation of Cited Bir Issuances, EtcDocument186 pagesTaxation I - Part Ii Compilation of Cited Bir Issuances, Etccmv mendozaNo ratings yet

- Bir Ruling Da 469 06Document6 pagesBir Ruling Da 469 06juliusNo ratings yet

- In Addition To Basic Salaries, To An Individual Employee, Other Than A Rank and File EmployeeDocument13 pagesIn Addition To Basic Salaries, To An Individual Employee, Other Than A Rank and File EmployeeNOW BIENo ratings yet

- Fringe Benefits TaxDocument4 pagesFringe Benefits TaxKathleen Jane SolmayorNo ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Act 1Document1 pageAct 1Christelle JosonNo ratings yet

- Prelim Exams in Human BehaviorDocument2 pagesPrelim Exams in Human BehaviorChristelle JosonNo ratings yet

- Olcae05 Act3Document1 pageOlcae05 Act3Christelle JosonNo ratings yet

- Financial Management Case StudyDocument11 pagesFinancial Management Case StudyChristelle JosonNo ratings yet

- Strong Brand ImageDocument1 pageStrong Brand ImageChristelle JosonNo ratings yet

- Activity2 Olcae5Document1 pageActivity2 Olcae5Christelle JosonNo ratings yet

- Act 4 Olprofe01Document1 pageAct 4 Olprofe01Christelle JosonNo ratings yet

- Act10 OlliteDocument1 pageAct10 OlliteChristelle JosonNo ratings yet

- CH9 Estate TaxDocument40 pagesCH9 Estate TaxZtrick 123472% (18)

- Act10 Olbl4Document2 pagesAct10 Olbl4Christelle JosonNo ratings yet

- Act9-10 Olbl7Document1 pageAct9-10 Olbl7Christelle JosonNo ratings yet

- Act9 OlliteDocument1 pageAct9 OlliteChristelle JosonNo ratings yet

- Prelim Exam in Financial ManagementDocument2 pagesPrelim Exam in Financial ManagementChristelle JosonNo ratings yet

- Act8 Olrzl1Document1 pageAct8 Olrzl1Christelle JosonNo ratings yet

- Act8 Olbl7Document1 pageAct8 Olbl7Christelle JosonNo ratings yet

- ACT7 Anflj Aplkwj D AsdDocument1 pageACT7 Anflj Aplkwj D AsdChristelle JosonNo ratings yet

- Act10 Olcae1Document1 pageAct10 Olcae1Christelle JosonNo ratings yet

- Act8 Olcae1Document1 pageAct8 Olcae1Christelle JosonNo ratings yet

- Act3 Olcae1Document9 pagesAct3 Olcae1Christelle JosonNo ratings yet

- ACT7 Adfsadas AdasdasdDocument1 pageACT7 Adfsadas AdasdasdChristelle JosonNo ratings yet

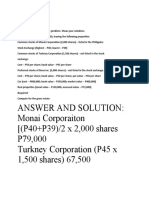

- Answer and Solution: Monai Corporaiton ( (P40+P39) /2 X 2,000 Shares P79,000 Turkney Corporation (P45 X 1,500 Shares) 67,500Document2 pagesAnswer and Solution: Monai Corporaiton ( (P40+P39) /2 X 2,000 Shares P79,000 Turkney Corporation (P45 X 1,500 Shares) 67,500Christelle JosonNo ratings yet

- Act1 Olcae4Document1 pageAct1 Olcae4Christelle JosonNo ratings yet

- Act1 Olrzl1Document1 pageAct1 Olrzl1Christelle JosonNo ratings yet

- Act 2 Olcae4Document1 pageAct 2 Olcae4Christelle JosonNo ratings yet

- Act1 Olbl7Document2 pagesAct1 Olbl7Christelle JosonNo ratings yet

- Act1 Olcae1Document2 pagesAct1 Olcae1Christelle JosonNo ratings yet

- A-P3,500.00 B-P2,500.00 C-P4,000.00. Each A, B and C Have P10,000 and Compute It in Their Percentage and That The Loss of Their DistributedDocument1 pageA-P3,500.00 B-P2,500.00 C-P4,000.00. Each A, B and C Have P10,000 and Compute It in Their Percentage and That The Loss of Their DistributedChristelle JosonNo ratings yet

- Accounting Concepts, Principles & IFRS FrameworkDocument6 pagesAccounting Concepts, Principles & IFRS FrameworkDaniel MadagascarNo ratings yet

- Cbtax01 Chapter4Document11 pagesCbtax01 Chapter4Christelle JosonNo ratings yet

- Bpactg Chapter1Document11 pagesBpactg Chapter1Christelle JosonNo ratings yet

- Module 1 Taxation ConceptsDocument13 pagesModule 1 Taxation ConceptsShelleyNo ratings yet

- Order in Respect of Application Filed by Gokul M Jaykrishna Family Trust Under Regulation 11 of Takeover Regulations, 2011 For Acquisition of Shares in Asahi Songwon Colors LimitedDocument10 pagesOrder in Respect of Application Filed by Gokul M Jaykrishna Family Trust Under Regulation 11 of Takeover Regulations, 2011 For Acquisition of Shares in Asahi Songwon Colors LimitedShyam SunderNo ratings yet

- Eliminating Water from Capital StructuresDocument4 pagesEliminating Water from Capital StructuresAnugrah EdoNo ratings yet

- 05 Ringor V RingorDocument12 pages05 Ringor V RingorJed MendozaNo ratings yet

- EquityDocument25 pagesEquityAli Azam Khan100% (11)

- DEED OF TRUST (Sample 1)Document5 pagesDEED OF TRUST (Sample 1)Siti Nur Hafiziyah IsmailNo ratings yet

- TwelveBiggestMistakes EstatePlanning PDFDocument37 pagesTwelveBiggestMistakes EstatePlanning PDFDanno N100% (1)

- Banking Laws Final Examinations: Instruments (Iuis)Document2 pagesBanking Laws Final Examinations: Instruments (Iuis)Patrick D GuetaNo ratings yet

- Voting Trust AgreementDocument4 pagesVoting Trust AgreementPablo Jan Marc Filio100% (3)

- GAIL INDIA ATC ITB - 4 - MrunalinichawareDocument176 pagesGAIL INDIA ATC ITB - 4 - MrunalinichawareSanjay AmberkarNo ratings yet

- waterAID 2009Document60 pageswaterAID 2009Amos Tawiah AntwiNo ratings yet

- Xxx-Tax Information & Avoidance AgreementDocument8 pagesXxx-Tax Information & Avoidance AgreementrajdeeppawarNo ratings yet

- Cad. Lot No. 25 Covered by Tax Declaration No. 11950Document11 pagesCad. Lot No. 25 Covered by Tax Declaration No. 11950Eugene DayanNo ratings yet

- Annual Return for Foreign Trust TransactionsDocument6 pagesAnnual Return for Foreign Trust TransactionsFAQMD2No ratings yet

- Cristobal Vs Gomez DigestDocument2 pagesCristobal Vs Gomez DigestJS100% (1)

- Duty of trustee to provide full accountingDocument1 pageDuty of trustee to provide full accountingjNo ratings yet

- Why File A Ucc1Document10 pagesWhy File A Ucc1kbarn389100% (4)

- Simple Medical Clinic Lease AgreementDocument110 pagesSimple Medical Clinic Lease AgreementIbrahim Hassan JrNo ratings yet

- AFFIDAVIT OF NEIL J. GILLESPIE Re Non-Jury Home Foreclosure Trial July 18, 2017 PDFDocument45 pagesAFFIDAVIT OF NEIL J. GILLESPIE Re Non-Jury Home Foreclosure Trial July 18, 2017 PDFNeil Gillespie100% (1)

- Code of Judicial ConductDocument3 pagesCode of Judicial ConductKristine Bernadette CruzNo ratings yet

- 1992 Bar Examination Topic: Corporation Voting Trust Agreement (1992)Document2 pages1992 Bar Examination Topic: Corporation Voting Trust Agreement (1992)Dustin NitroNo ratings yet

- 1.1 Account Opening Checklist (Corporation)Document2 pages1.1 Account Opening Checklist (Corporation)angkalabawNo ratings yet

- How to Obtain a ProbateDocument22 pagesHow to Obtain a ProbateSyarah Syazwan Satury100% (3)

- Merrimon v. Unum Life Insurance Company, 1st Cir. (2014)Document29 pagesMerrimon v. Unum Life Insurance Company, 1st Cir. (2014)Scribd Government DocsNo ratings yet

- Implied Trust Under Art. 1448 Does Not Apply If Property Was In Name Of Purchaser's ChildDocument1 pageImplied Trust Under Art. 1448 Does Not Apply If Property Was In Name Of Purchaser's ChildavrilleNo ratings yet

- Lawyers and Clients' Moneys and PropertiesDocument6 pagesLawyers and Clients' Moneys and PropertiesAl BautistaNo ratings yet

- United States Court of Appeals, Third CircuitDocument14 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Estate and Donor's TaxDocument6 pagesEstate and Donor's TaxKimberly SendinNo ratings yet

- Complete Initial BriefDocument15 pagesComplete Initial BriefDwayne ZookNo ratings yet

- Canezo v. Roxas G.R. No. 148788 November 23, 2007Document4 pagesCanezo v. Roxas G.R. No. 148788 November 23, 2007Rosalia L. Completano LptNo ratings yet