You might also like

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Edurev - In-Social Studies SST Class 10Document9 pagesEdurev - In-Social Studies SST Class 10asfiyarahmath2008No ratings yet

- SST Chapterwise PYQs Shobhit NirwanDocument29 pagesSST Chapterwise PYQs Shobhit NirwanMaydhansh Kadge100% (1)

- 3 - Money & CreditDocument3 pages3 - Money & CreditsonurazadNo ratings yet

- 07e3564d-dde0-4d5f-9f0a-d74787a7939eDocument4 pages07e3564d-dde0-4d5f-9f0a-d74787a7939eBucket Of MemesNo ratings yet

- Credit CreationDocument46 pagesCredit Creationrizw_anNo ratings yet

- TestDocument6 pagesTestMayank JainNo ratings yet

- Important Quess) Tions ch-3Document9 pagesImportant Quess) Tions ch-3AnnaNo ratings yet

- Money and Credit Class X CBSEDocument5 pagesMoney and Credit Class X CBSERaj Rai100% (1)

- Money and CreditDocument7 pagesMoney and Creditx.makiyana.xNo ratings yet

- CH3 Money Credit Practice MS 2022-23Document5 pagesCH3 Money Credit Practice MS 2022-23ARSHAD JAMILNo ratings yet

- Money and CreditDocument6 pagesMoney and CreditArshpreet KaurNo ratings yet

- Money and CreditDocument12 pagesMoney and CreditthinkiitNo ratings yet

- CH 8 Sources of Business Finance Class 11 BSTDocument19 pagesCH 8 Sources of Business Finance Class 11 BSTRaman SachdevaNo ratings yet

- Class 10 Social Money and Credit Notes 1639753090Document10 pagesClass 10 Social Money and Credit Notes 1639753090KrizsNo ratings yet

- MONEY X EconomicsDocument7 pagesMONEY X EconomicsAvika SinghNo ratings yet

- Money Banking & FinanceDocument37 pagesMoney Banking & FinanceAhmad BelalNo ratings yet

- PobDocument24 pagesPobgillyhicksNo ratings yet

- ASSIGNMENT - MONEY AND CREDIT - UpdatedDocument10 pagesASSIGNMENT - MONEY AND CREDIT - UpdatedKing UtkarshNo ratings yet

- Rafiqul SirDocument7 pagesRafiqul SirShakiul RanaNo ratings yet

- Money and CreditDocument15 pagesMoney and CreditManas DasNo ratings yet

- Boca Assignment: Issues and Challenges of Banking Sector and Alloted Bank: Bank of IndiaDocument5 pagesBoca Assignment: Issues and Challenges of Banking Sector and Alloted Bank: Bank of IndiaRahul KumarNo ratings yet

- Study Material Question Bank and Answer Key Economics: Money and CreditDocument14 pagesStudy Material Question Bank and Answer Key Economics: Money and CreditsaanviNo ratings yet

- Money and CreditDocument4 pagesMoney and Creditvibrantbhabha7No ratings yet

- 5 Tiwxm MR Be 8 RKAk T0 UsgDocument28 pages5 Tiwxm MR Be 8 RKAk T0 Usgshanmuga Priya (Shan)No ratings yet

- Banking LawDocument63 pagesBanking Lawpraveen ramanjaneyaluNo ratings yet

- PPBADocument5 pagesPPBAMANISHNo ratings yet

- Money and Credit PadhleakshayDocument22 pagesMoney and Credit Padhleakshayshortstube2025No ratings yet

- Loan SyndicationDocument12 pagesLoan SyndicationArpit Jain100% (1)

- Money and Credit Important Questions and Answers PDFDocument12 pagesMoney and Credit Important Questions and Answers PDFAkkajNo ratings yet

- Money and CreditDocument14 pagesMoney and CreditRajau RajputanaNo ratings yet

- Commercial Banking System and Role of RBI PG QP JUNE 2024 PDFDocument4 pagesCommercial Banking System and Role of RBI PG QP JUNE 2024 PDFBalamuralikrishna YadavNo ratings yet

- 1) Threat of New Entrants: (A) Trust FactorDocument4 pages1) Threat of New Entrants: (A) Trust FactorVijay RamanNo ratings yet

- Chapter - 1Document49 pagesChapter - 1KarunaNo ratings yet

- Money and CreditDocument5 pagesMoney and CreditBhargav Srinivas100% (1)

- ECONOMICS Most Important Questions (Prashant Kirad)Document6 pagesECONOMICS Most Important Questions (Prashant Kirad)Sanju SamNo ratings yet

- Famd Assingnment: The Sources of FinanceDocument11 pagesFamd Assingnment: The Sources of FinanceCoulibaly YounoussouNo ratings yet

- Commercial Bank PDFDocument22 pagesCommercial Bank PDFA ThakurNo ratings yet

- Money and CreditDocument13 pagesMoney and CreditRengavadivelammaal .CNo ratings yet

- TB Bank loans-đã chuyển sang wordDocument8 pagesTB Bank loans-đã chuyển sang wordVi TrươngNo ratings yet

- NCERT Solutions Class 10 Social Science Economics Chapter 3 Money and CreditDocument4 pagesNCERT Solutions Class 10 Social Science Economics Chapter 3 Money and CreditTaksh MehrotraNo ratings yet

- Banking-Law Notes11Document66 pagesBanking-Law Notes11BharatNo ratings yet

- Banking and Financial InstitutionsDocument6 pagesBanking and Financial InstitutionsAriel ManaloNo ratings yet

- Chapter1: Introduction of Indian BankDocument46 pagesChapter1: Introduction of Indian BankRupal Rohan DalalNo ratings yet

- 1.money and CreditDocument18 pages1.money and CreditNandita KrishnanNo ratings yet

- NCERT Solutions For Class 10 Social Science Chapter-3 Money and CreditDocument5 pagesNCERT Solutions For Class 10 Social Science Chapter-3 Money and Creditclevermind2407No ratings yet

- Retail BankingDocument25 pagesRetail BankingTrusha Hodiwala80% (5)

- Chapter 1: IntroductionDocument77 pagesChapter 1: IntroductionMohiuddin ansariNo ratings yet

- Credit Sources and Credit CardsDocument11 pagesCredit Sources and Credit CardsPoonam VermaNo ratings yet

- Commercial BankingDocument14 pagesCommercial BankingSudheer Kumar SNo ratings yet

- Banking Law PYQDocument11 pagesBanking Law PYQxakij19914No ratings yet

- Advertising Strategies of Banking Sectors in IndiaDocument77 pagesAdvertising Strategies of Banking Sectors in Indiakevalcool250No ratings yet

- Dipali Project ReportDocument58 pagesDipali Project ReportAshish MOHARENo ratings yet

- Banking Financial Services Management - Unit 1: Overview of Indian Banking SystemDocument64 pagesBanking Financial Services Management - Unit 1: Overview of Indian Banking SystemtkashvinNo ratings yet

- Ch.3 Money and Credit (Economics-X)Document11 pagesCh.3 Money and Credit (Economics-X)Ayush ChaurasiaNo ratings yet

- Fiim S02Document45 pagesFiim S02Ali MohammedNo ratings yet

- ProjectDocument72 pagesProject9463684355No ratings yet

- BFSI Training Manual - PDF - 20230810 - 164502 - 0000Document136 pagesBFSI Training Manual - PDF - 20230810 - 164502 - 0000deepak643aNo ratings yet

- Auto Debit Arrangement - 20201019 - 095034 PDFDocument3 pagesAuto Debit Arrangement - 20201019 - 095034 PDFRobert Adrian De RuedaNo ratings yet

- Deutsche For Infogs Page Final 1Document2 pagesDeutsche For Infogs Page Final 1jayNo ratings yet

- Accenture Counterparty Credit Risk Basel Framework Successful ImplementationDocument17 pagesAccenture Counterparty Credit Risk Basel Framework Successful ImplementationszbillNo ratings yet

- Marketing management-Assignment-IIDocument13 pagesMarketing management-Assignment-IITeke TarekegnNo ratings yet

- Case Title: BANK OF THE PHILIPPINE ISLANDS, Petitioner, vs. THEDocument83 pagesCase Title: BANK OF THE PHILIPPINE ISLANDS, Petitioner, vs. THEJoseph MacalintalNo ratings yet

- A. The History of World BankDocument1 pageA. The History of World BankFatimah Rahima JingonaNo ratings yet

- Marketing Strategies of ICICI BankDocument8 pagesMarketing Strategies of ICICI BankSidharth AggarwalNo ratings yet

- Live CAMS PrepDocument187 pagesLive CAMS Prepvinttt13409No ratings yet

- 19.format Hum A Study of Pradhan Mantri Jan Dhan YojanaDocument6 pages19.format Hum A Study of Pradhan Mantri Jan Dhan YojanaImpact JournalsNo ratings yet

- I 4 UX1 C9 GTVe FR5 D MDocument6 pagesI 4 UX1 C9 GTVe FR5 D MsriNo ratings yet

- Clipper Logistics PLC PDFDocument156 pagesClipper Logistics PLC PDFWilliamK96No ratings yet

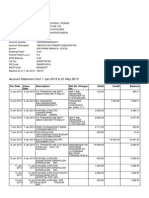

- Account StatementDocument6 pagesAccount StatementDeepaBabukumarNo ratings yet

- Vehicle Insurance PopDocument2 pagesVehicle Insurance PopTadiwanashe ChikoworeNo ratings yet

- Banking Sector ReformsDocument7 pagesBanking Sector ReformsanamikaNo ratings yet

- Tata Capital Financial Services LTDDocument23 pagesTata Capital Financial Services LTDsweetmadhavi100% (1)

- Reporting Portal FAQs - V5.2Document137 pagesReporting Portal FAQs - V5.2Karthik YadavNo ratings yet

- NOTES Onthe Bank Secrecy Law (RA1405)Document9 pagesNOTES Onthe Bank Secrecy Law (RA1405)edrianclydeNo ratings yet

- Export - Import Bank: Fiscal Years 2007-2014: Overview StudyDocument28 pagesExport - Import Bank: Fiscal Years 2007-2014: Overview StudyCatherine CampbellNo ratings yet

- Accounting Class No. 2-3 (Case 4-7)Document2 pagesAccounting Class No. 2-3 (Case 4-7)Мария НиколенкоNo ratings yet

- 231AA Order To Grant Refuse Reduced Rate of Withholding On Transaction in BankDocument2 pages231AA Order To Grant Refuse Reduced Rate of Withholding On Transaction in BankMuhammad Imran KhanNo ratings yet

- Joe Owen: Contact MeDocument2 pagesJoe Owen: Contact MeRia LedNo ratings yet

- Job Description Job Title Level Division Company No of Positions Location Reporting ToDocument2 pagesJob Description Job Title Level Division Company No of Positions Location Reporting Tosuganth samuelNo ratings yet

- 2014feb Mock Ans EngDocument24 pages2014feb Mock Ans EngKaito MagicNo ratings yet

- Your Adv Plus Banking: Account SummaryDocument6 pagesYour Adv Plus Banking: Account SummaryЮлия ПNo ratings yet

- Internship ProgrammeDocument8 pagesInternship ProgrammeMayank PrakashNo ratings yet

- UNIT-3 Merchant Banking:: Commercial BanksDocument26 pagesUNIT-3 Merchant Banking:: Commercial BanksTeja SwiNo ratings yet

- Alice Blue Financial Service PVT LTD: Client Registration FormDocument26 pagesAlice Blue Financial Service PVT LTD: Client Registration FormAzhar ShaikhNo ratings yet

- CTBC App-SignedDocument2 pagesCTBC App-SignedLloyd MoloNo ratings yet

- Astron Paper & Board - RHPDocument468 pagesAstron Paper & Board - RHPsubham agrawalNo ratings yet

- Audit of Liabilities SolManDocument3 pagesAudit of Liabilities SolManReyn Saplad PeralesNo ratings yet

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (82)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- The Best Team Wins: The New Science of High PerformanceFrom EverandThe Best Team Wins: The New Science of High PerformanceRating: 4.5 out of 5 stars4.5/5 (31)

- Sacred Success: A Course in Financial MiraclesFrom EverandSacred Success: A Course in Financial MiraclesRating: 5 out of 5 stars5/5 (15)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouFrom EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouRating: 5 out of 5 stars5/5 (5)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)From EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Rating: 3.5 out of 5 stars3.5/5 (9)

- Altcoins Coins The Future is Now Enjin Dogecoin Polygon Matic Ada: blockchain technology seriesFrom EverandAltcoins Coins The Future is Now Enjin Dogecoin Polygon Matic Ada: blockchain technology seriesRating: 5 out of 5 stars5/5 (1)

- How to Save Money: 100 Ways to Live a Frugal LifeFrom EverandHow to Save Money: 100 Ways to Live a Frugal LifeRating: 5 out of 5 stars5/5 (1)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- Money Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayFrom EverandMoney Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayRating: 3.5 out of 5 stars3.5/5 (2)

- Happy Go Money: Spend Smart, Save Right and Enjoy LifeFrom EverandHappy Go Money: Spend Smart, Save Right and Enjoy LifeRating: 5 out of 5 stars5/5 (4)

- The New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningFrom EverandThe New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningRating: 4.5 out of 5 stars4.5/5 (8)

- Buy the Milk First: ... and Other Secrets to Financial Prosperity, Regardless of Your IncomeFrom EverandBuy the Milk First: ... and Other Secrets to Financial Prosperity, Regardless of Your IncomeNo ratings yet

- Minding Your Own Business: A Common Sense Guide to Home Management and IndustryFrom EverandMinding Your Own Business: A Common Sense Guide to Home Management and IndustryRating: 5 out of 5 stars5/5 (1)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessFrom EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessRating: 4.5 out of 5 stars4.5/5 (4)

- Smart, Not Spoiled: The 7 Money Skills Kids Must Master Before Leaving the NestFrom EverandSmart, Not Spoiled: The 7 Money Skills Kids Must Master Before Leaving the NestRating: 5 out of 5 stars5/5 (1)

- Bitcoin Secrets Revealed - The Complete Bitcoin Guide To Buying, Selling, Mining, Investing And Exchange Trading In Bitcoin CurrencyFrom EverandBitcoin Secrets Revealed - The Complete Bitcoin Guide To Buying, Selling, Mining, Investing And Exchange Trading In Bitcoin CurrencyRating: 4 out of 5 stars4/5 (4)

- The Complete Strategy Guide to Day Trading for a Living in 2019: Revealing the Best Up-to-Date Forex, Options, Stock and Swing Trading Strategies of 2019 (Beginners Guide)From EverandThe Complete Strategy Guide to Day Trading for a Living in 2019: Revealing the Best Up-to-Date Forex, Options, Stock and Swing Trading Strategies of 2019 (Beginners Guide)Rating: 4 out of 5 stars4/5 (34)

- Summary of You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You Want by Jesse MechamFrom EverandSummary of You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You Want by Jesse MechamRating: 5 out of 5 stars5/5 (1)