You might also like

- Primer on Social Bonds and Recent Developments in AsiaFrom EverandPrimer on Social Bonds and Recent Developments in AsiaNo ratings yet

- Wa0001Document94 pagesWa0001Akash Ðaya SinhaNo ratings yet

- Chapter 1Document94 pagesChapter 1Narendran SrinivasanNo ratings yet

- Punjab National BankDocument50 pagesPunjab National BankHitesh KumarNo ratings yet

- Punjab National Bank - Banking ReportDocument36 pagesPunjab National Bank - Banking ReportGoutham SunilNo ratings yet

- Introduction of Pnb,,,Improved FileDocument10 pagesIntroduction of Pnb,,,Improved FileJitin BhutaniNo ratings yet

- Study On Financial Products of PNBDocument17 pagesStudy On Financial Products of PNBPragati BahlNo ratings yet

- Overview of Banking Giant PNB and the Nirav Modi ScamDocument10 pagesOverview of Banking Giant PNB and the Nirav Modi ScamShubham LalwaniNo ratings yet

- Report On Institutional Training at Canara BankDocument51 pagesReport On Institutional Training at Canara BankPoojaNo ratings yet

- A Project Report On Comparison Between HDFC Bank & ICICI BankDocument75 pagesA Project Report On Comparison Between HDFC Bank & ICICI Bankvarun_bawa25191592% (12)

- Project On Indian Overseas BanklDocument58 pagesProject On Indian Overseas BanklPrathamesh BhabalNo ratings yet

- Rahul Gupta 12 - MergedDocument55 pagesRahul Gupta 12 - MergedJd GuptaNo ratings yet

- HDFC Bank Summer ReportDocument55 pagesHDFC Bank Summer Reportilover_140085% (20)

- HDFC BankDocument72 pagesHDFC Banknitish_goel91No ratings yet

- Bank Traning Project Report On IOB BankDocument76 pagesBank Traning Project Report On IOB BankLokeshlion89% (9)

- Iob ProfileDocument13 pagesIob ProfileNeethu GesanNo ratings yet

- 1.1history of BankingDocument18 pages1.1history of BankingHarika KollatiNo ratings yet

- Icici BankDocument43 pagesIcici BankRosalie StryderNo ratings yet

- Canara Bank - Vishal NihalaniDocument15 pagesCanara Bank - Vishal NihalanivishnihalaniNo ratings yet

- Black Book of Bob and IciciDocument42 pagesBlack Book of Bob and IciciDHAIRYA09No ratings yet

- Chapter-4 Organizational Structure of HDFC BankDocument17 pagesChapter-4 Organizational Structure of HDFC Bankshraddha100% (1)

- A study on home loans of icici bank (1)Document50 pagesA study on home loans of icici bank (1)Saumya BajpaiNo ratings yet

- Khushabu Singh B 66Document24 pagesKhushabu Singh B 66smellsinghNo ratings yet

- Project Reort Risk ManagementDocument89 pagesProject Reort Risk ManagementDinesh ChahalNo ratings yet

- Introduction Chapter 1Document13 pagesIntroduction Chapter 1markcalawaywwe211No ratings yet

- A Project Report On Employees Satisfaction Regarding HDFC BankDocument77 pagesA Project Report On Employees Satisfaction Regarding HDFC Bankvarun_bawa25191578% (23)

- SBI Overview: History, Leadership and OperationsDocument58 pagesSBI Overview: History, Leadership and Operationspuneetbansal14No ratings yet

- Project Reort New ShubhamDocument92 pagesProject Reort New ShubhamDinesh ChahalNo ratings yet

- Banking in India SumeshDocument26 pagesBanking in India Sumeshsumesh894No ratings yet

- HDFC Bank SWOT Analysis and CompetitorsDocument7 pagesHDFC Bank SWOT Analysis and CompetitorsAishwarya GangawaneNo ratings yet

- A Project Report ON: Submitted in Partial Fulfillment of The Requirement of Bachelor of BusinessDocument87 pagesA Project Report ON: Submitted in Partial Fulfillment of The Requirement of Bachelor of BusinessAnonymous l5X3VhTNo ratings yet

- Axis Bank Corporate Strategy AnalysisDocument34 pagesAxis Bank Corporate Strategy AnalysisDeep Ghose DastidarNo ratings yet

- Comparison of Public & Private Sector Banks On The Basis of 9 P's - Project ReportDocument47 pagesComparison of Public & Private Sector Banks On The Basis of 9 P's - Project ReportAkash Rajput67% (3)

- Axis Bank ReportDocument55 pagesAxis Bank ReportAjay RohillaNo ratings yet

- Introduction Chapter -1Document13 pagesIntroduction Chapter -1rkopubg316No ratings yet

- HDFC Bank Ltd. - Customer Attitude Towards ATM Services55555555555555555555555555Document110 pagesHDFC Bank Ltd. - Customer Attitude Towards ATM Services55555555555555555555555555Vaibhav MishraNo ratings yet

- Marketing Strategies of HDFC BankDocument72 pagesMarketing Strategies of HDFC Banksunit2658No ratings yet

- Banking Industry Profile: India's Banking Sector and Canara Bank(39Document16 pagesBanking Industry Profile: India's Banking Sector and Canara Bank(39active1cafeNo ratings yet

- Rubika Final ProjectDocument73 pagesRubika Final ProjectRubika MunusamyNo ratings yet

- Credit AppraisalDocument122 pagesCredit AppraisalKunal GoelNo ratings yet

- FINALbank of BarodaDocument27 pagesFINALbank of BarodaAbdussamad ChandiwalaNo ratings yet

- Introduction of Bank of BarodaDocument23 pagesIntroduction of Bank of BarodaDhananjay AwareNo ratings yet

- Synopsis Icici & Customer SatisfactionDocument17 pagesSynopsis Icici & Customer SatisfactionbhatiaharryjassiNo ratings yet

- A1 Merged PDFDocument121 pagesA1 Merged PDFMahesh BabuNo ratings yet

- Business StrategyDocument4 pagesBusiness StrategyArimuthukumarNambiNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Finding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificFrom EverandFinding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificNo ratings yet

- Promoting Local Currency Sustainable Finance in ASEAN+3From EverandPromoting Local Currency Sustainable Finance in ASEAN+3No ratings yet

- India's Store Wars: Retail Revolution and the Battle for the Next 500 Million ShoppersFrom EverandIndia's Store Wars: Retail Revolution and the Battle for the Next 500 Million ShoppersNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- Developing a local currency government Bond market in an emerging economy after COVID-19: Case for the Lao People’s Democratic RepublicFrom EverandDeveloping a local currency government Bond market in an emerging economy after COVID-19: Case for the Lao People’s Democratic RepublicNo ratings yet

- Promoting Social Bonds for Impact Investments in AsiaFrom EverandPromoting Social Bonds for Impact Investments in AsiaNo ratings yet

- Road Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificFrom EverandRoad Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificNo ratings yet

- Financing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesFrom EverandFinancing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesNo ratings yet

- Grammar Response Profile CommandsDocument3 pagesGrammar Response Profile CommandsPavan Kumar SuralaNo ratings yet

- Definition of 'HackingDocument5 pagesDefinition of 'HackingPavan Kumar SuralaNo ratings yet

- Grammar Response Profile CommandsDocument3 pagesGrammar Response Profile CommandsPavan Kumar SuralaNo ratings yet

- Grammar Response CommandsDocument2 pagesGrammar Response CommandsPavan Kumar SuralaNo ratings yet

- Export DefaultDocument3 pagesExport DefaultPavan Kumar SuralaNo ratings yet

- Functions of Commercial Banks: Primary and Secondary FunctionsDocument3 pagesFunctions of Commercial Banks: Primary and Secondary FunctionsPavan Kumar SuralaNo ratings yet

- Web DegDocument1 pageWeb DegPavan Kumar SuralaNo ratings yet

- Project On HDFC LoansDocument61 pagesProject On HDFC LoansPallavi80% (15)

- MethodologyDocument9 pagesMethodologyPavan Kumar SuralaNo ratings yet

- PdaDocument41 pagesPdaPavan Kumar SuralaNo ratings yet

- PKDocument2 pagesPKPavan Kumar SuralaNo ratings yet

- MethodologyDocument9 pagesMethodologyPavan Kumar SuralaNo ratings yet

- MethodologyDocument9 pagesMethodologyPavan Kumar SuralaNo ratings yet

- Web DegDocument1 pageWeb DegPavan Kumar SuralaNo ratings yet

- BankingDocument2 pagesBankingPavan Kumar SuralaNo ratings yet

- SpecialDocument4 pagesSpecialPavan Kumar SuralaNo ratings yet

- SpecialDocument4 pagesSpecialPavan Kumar SuralaNo ratings yet

- Qatar AirwaysDocument3 pagesQatar AirwaysJess Elias ObarNo ratings yet

- How To Get Paid: Purchase LedgerDocument3 pagesHow To Get Paid: Purchase LedgerJames BarnesNo ratings yet

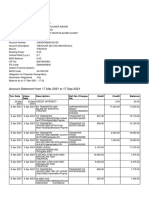

- Account Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManoj PrabhakarNo ratings yet

- Online Bank Management System ReportDocument9 pagesOnline Bank Management System ReportUmaNo ratings yet

- Account Opening Tier 3Document4 pagesAccount Opening Tier 3Benedict WannyamNo ratings yet

- Cswip Renewal FormDocument4 pagesCswip Renewal FormGobinderSinghSidhu0% (1)

- Zalora Chat ScriptDocument6 pagesZalora Chat ScriptGraciella De GuzmanNo ratings yet

- AccountDocument8 pagesAccountSaral JainNo ratings yet

- Intro To EMVDocument15 pagesIntro To EMVLokesh100% (2)

- Account STMTDocument6 pagesAccount STMTNaveenchdrNo ratings yet

- Strategic Management A Case Study On Virtual OrganisationDocument49 pagesStrategic Management A Case Study On Virtual OrganisationAlfiya ShaikhNo ratings yet

- User GuideDocument96 pagesUser GuideRajanNo ratings yet

- RPP EspDocument11 pagesRPP EspKrissiana PermataNo ratings yet

- Debit Credit NoteDocument4 pagesDebit Credit NoteMập Xấu TínhNo ratings yet

- Dispute Form Bigpay BPMYDocument1 pageDispute Form Bigpay BPMYharithh.rahsiaNo ratings yet

- Anz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlanceDocument12 pagesAnz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlancevtmnewsltdNo ratings yet

- Retail Banking Indusind BankDocument54 pagesRetail Banking Indusind BankNithin NitNo ratings yet

- Annual Report 2007Document168 pagesAnnual Report 2007anithaasriiNo ratings yet

- Bharti Airtel LTD.: Your Account Summary This Month'S ChargesDocument5 pagesBharti Airtel LTD.: Your Account Summary This Month'S ChargesMadhukar Reddy KukunoorNo ratings yet

- Cof f89 t89 r59 NoeDocument50 pagesCof f89 t89 r59 Noejames0% (1)

- LowesCompanies 10K 20180402Document93 pagesLowesCompanies 10K 20180402divya mNo ratings yet

- Sekar AcDocument7 pagesSekar AcP.sekaran P.sekaranNo ratings yet

- How To Check Visa Card Balance - Google SearchDocument1 pageHow To Check Visa Card Balance - Google SearchmyytextnowwNo ratings yet

- Aman Gupta Mini Project 2Document81 pagesAman Gupta Mini Project 2Suneet kumarNo ratings yet

- How To Reach Us: Account Summary Account #Document4 pagesHow To Reach Us: Account Summary Account #jmsmithNo ratings yet

- Airport Security Asia 2012Document6 pagesAirport Security Asia 2012Sg2012No ratings yet

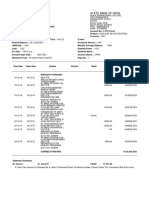

- Statement of Account: State Bank of IndiaDocument9 pagesStatement of Account: State Bank of IndiaBhati HusenshaNo ratings yet

- Mandate Hub User GuideDocument53 pagesMandate Hub User GuideMuruganand RamalingamNo ratings yet

- Statement of Account: State Bank of IndiaDocument9 pagesStatement of Account: State Bank of IndiaharishNo ratings yet

- Ing Vysya BankDocument60 pagesIng Vysya BankRaghvendra Pratap SinghNo ratings yet