You might also like

- Homeloans IciciDocument83 pagesHomeloans Icicitajju_121No ratings yet

- Final Project Report - Docx Axis BankDocument73 pagesFinal Project Report - Docx Axis BankSuraj GhongeNo ratings yet

- Icici BankDocument43 pagesIcici BankRosalie StryderNo ratings yet

- Rahul Gupta 12 - MergedDocument55 pagesRahul Gupta 12 - MergedJd GuptaNo ratings yet

- Ib Presen SandyDocument20 pagesIb Presen Sandysandeepbist88No ratings yet

- Classification of BanksDocument39 pagesClassification of BanksPrajith VNo ratings yet

- Banking 130730020756 Phpapp02Document48 pagesBanking 130730020756 Phpapp02Vaibhav BairagiNo ratings yet

- Industry and Company ProfileDocument26 pagesIndustry and Company ProfileNIMMANAGANTI RAMAKRISHNANo ratings yet

- Industry ProfileDocument67 pagesIndustry ProfilegurdithNo ratings yet

- Chapter - 2 Theoretical BackgroundDocument16 pagesChapter - 2 Theoretical BackgroundASWATHYNo ratings yet

- Unit 1 Introduction To BankingDocument61 pagesUnit 1 Introduction To Bankingceweli8890No ratings yet

- Corporation BankDocument70 pagesCorporation Bankrangudasar100% (2)

- Function of Public Sector BanksDocument51 pagesFunction of Public Sector BanksdynamicdeepsNo ratings yet

- Commercial Banking NotesDocument68 pagesCommercial Banking NotesG NagarajanNo ratings yet

- Structure of Banking CompaniesDocument18 pagesStructure of Banking Companiesbeena antuNo ratings yet

- Chapter-4 Organizational Structure of HDFC BankDocument17 pagesChapter-4 Organizational Structure of HDFC Bankshraddha100% (1)

- Introduction To BankingDocument24 pagesIntroduction To Bankingmihir kothariNo ratings yet

- Customer Preference Towards Private Vs Public Sector Banks During The Curren Ttime of RecessionDocument75 pagesCustomer Preference Towards Private Vs Public Sector Banks During The Curren Ttime of Recessionswatisabherwal80% (5)

- A Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)Document56 pagesA Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)geetha_kannan32No ratings yet

- Bank & Bill Discounting: Lalita Choudhary TYBBI, 11Document40 pagesBank & Bill Discounting: Lalita Choudhary TYBBI, 11VIVEK MEHTANo ratings yet

- Indian Banking SectorDocument18 pagesIndian Banking Sectorapurva JainNo ratings yet

- Summer Internship ProgramDocument56 pagesSummer Internship Programtom pierceNo ratings yet

- Summer Internship Program: Leveraging Digital Channels For EnhancingDocument52 pagesSummer Internship Program: Leveraging Digital Channels For Enhancingtom pierceNo ratings yet

- Final Blackbook PalakDocument96 pagesFinal Blackbook PalakPalak MehtaNo ratings yet

- Growth in Banking SectorDocument30 pagesGrowth in Banking SectorHarish Rawal Harish RawalNo ratings yet

- Banking Structure in IndiaDocument24 pagesBanking Structure in Indiasandeep95No ratings yet

- Banking 1Document69 pagesBanking 1Shaifali GargNo ratings yet

- PNB BOB MergerDocument36 pagesPNB BOB MergerAarzoo BadruNo ratings yet

- FINAL - PROJECT Report On HSBCDocument72 pagesFINAL - PROJECT Report On HSBCgururaj77167% (3)

- Fundamental Analysis of Private and Public Sector - 230131 - 103604Document57 pagesFundamental Analysis of Private and Public Sector - 230131 - 103604Abirami ThevarNo ratings yet

- I Am Sharing 'Fundamental Analysis of Private and Public Sector - 230131 - 103604' With YouDocument45 pagesI Am Sharing 'Fundamental Analysis of Private and Public Sector - 230131 - 103604' With YouAbirami ThevarNo ratings yet

- Corporation Bank MP Birla InternshipDocument20 pagesCorporation Bank MP Birla InternshipsrikanthkgNo ratings yet

- Banking: Prepared by DR Deepak Tandon IMI New DelhiDocument118 pagesBanking: Prepared by DR Deepak Tandon IMI New Delhidev mhaispurkarNo ratings yet

- Banking Mob 1Document79 pagesBanking Mob 1Deepak TandonNo ratings yet

- Banking Operations Unit 2Document18 pagesBanking Operations Unit 2rajshree balaniNo ratings yet

- BANKING AND FINANCE IN INDIA Post-IndepeDocument22 pagesBANKING AND FINANCE IN INDIA Post-IndepePravin ThoratNo ratings yet

- Customer SatisfactionDocument65 pagesCustomer SatisfactionChandan SrivastavaNo ratings yet

- Banking Unit 1Document69 pagesBanking Unit 1Shaifali ChauhanNo ratings yet

- Aaqib Final ProjectDocument58 pagesAaqib Final ProjectJkgi InstitutionsNo ratings yet

- Growth in Banking SectorDocument30 pagesGrowth in Banking SectorLatha Ravishankar50% (2)

- Bank of Bengal Bank of Bombay Bank of MadrasDocument7 pagesBank of Bengal Bank of Bombay Bank of MadrasShilpa JainNo ratings yet

- Private Banks in India: Public Sector Banks Are Those Banks Run Under The Control of Government and TheirDocument6 pagesPrivate Banks in India: Public Sector Banks Are Those Banks Run Under The Control of Government and TheirKajol GhoshNo ratings yet

- Banking Process and Basics of Operations.Document34 pagesBanking Process and Basics of Operations.amritaa chaurrasiaNo ratings yet

- Synopsis Icici & Customer SatisfactionDocument17 pagesSynopsis Icici & Customer SatisfactionbhatiaharryjassiNo ratings yet

- Working Capital Management: The Technological Institute of Textile & Sciences, BhiwaniDocument24 pagesWorking Capital Management: The Technological Institute of Textile & Sciences, BhiwaniMohitNo ratings yet

- (Batch 2020 - 2022) : Prestige Institute of Management and Research, IndoreDocument14 pages(Batch 2020 - 2022) : Prestige Institute of Management and Research, IndoreanjaliNo ratings yet

- Fundamental Analysis of Banking SectorsDocument56 pagesFundamental Analysis of Banking SectorsRajesh BathulaNo ratings yet

- Chapter - One: Banking in IndiaDocument56 pagesChapter - One: Banking in IndiaDivya SinghNo ratings yet

- Project On ICICI BankDocument104 pagesProject On ICICI BankVrinda KaushalNo ratings yet

- ICICI Project ReportDocument53 pagesICICI Project ReportPawan MeenaNo ratings yet

- Growth in Indian Banking SectorDocument59 pagesGrowth in Indian Banking SectorKishan KudiaNo ratings yet

- BankDocument94 pagesBankNaren JangirNo ratings yet

- 4cb2indian Banking SystemDocument25 pages4cb2indian Banking SystemFaisal BatlaNo ratings yet

- Chapter - 1Document49 pagesChapter - 1ASWATHYNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- Lu Fee Receipt ApplicationDetails - 20245000420Document2 pagesLu Fee Receipt ApplicationDetails - 20245000420Saumya BajpaiNo ratings yet

- Lecture2 RBIDocument12 pagesLecture2 RBIbackupsanthosh21 dataNo ratings yet

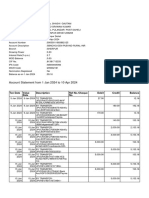

- Statement 1 Jan 24 To 10apr 24Document4 pagesStatement 1 Jan 24 To 10apr 24Saumya BajpaiNo ratings yet

- Role of Reserve Bank in Indian Banking System: Conference PaperDocument11 pagesRole of Reserve Bank in Indian Banking System: Conference PaperVanraj MakwanaNo ratings yet

- PG Admission Information Brochure University of Lucknow - 2023-2024.cdrDocument40 pagesPG Admission Information Brochure University of Lucknow - 2023-2024.cdrS M SHEKAR AND CONo ratings yet

- Acknowledgement Receipt IIBS MBA 24 12163Document1 pageAcknowledgement Receipt IIBS MBA 24 12163Saumya BajpaiNo ratings yet

- Zaber and ZubairDocument5 pagesZaber and ZubairMaliha SalsabilNo ratings yet

- Midwest Lesson Plan 1Document9 pagesMidwest Lesson Plan 1api-269401169No ratings yet

- Trading in Securities and RegulationsDocument25 pagesTrading in Securities and Regulationsgunn RastogiNo ratings yet

- Tallyerp9book Sample PageDocument24 pagesTallyerp9book Sample PagerudramanvNo ratings yet

- Group 1 - TA AssignmentDocument10 pagesGroup 1 - TA AssignmentAlka RajpalNo ratings yet

- Kunci Jawaban Modul AKL Bu Iin - OlivethewennoDocument17 pagesKunci Jawaban Modul AKL Bu Iin - OlivethewennoOliviane Theodora WennoNo ratings yet

- Original PDF The Economics of Women Men and Work 8th PDFDocument41 pagesOriginal PDF The Economics of Women Men and Work 8th PDFthomas.coffelt514100% (36)

- 659 Anwesh-008Document12 pages659 Anwesh-008moodautiasapnaNo ratings yet

- Chapter 3 - International TradeDocument70 pagesChapter 3 - International TradeHay JirenyaaNo ratings yet

- Capsim Cheat SheetDocument8 pagesCapsim Cheat Sheetyog s100% (1)

- 300 GA Questions For RBI Phase 1Document88 pages300 GA Questions For RBI Phase 1cidric cidNo ratings yet

- VarianceDocument5 pagesVarianceMuhammad Hussnain100% (1)

- Demand Side EquilibriumDocument97 pagesDemand Side EquilibriumChi Jui James TienNo ratings yet

- Liran Ben Asuly - CVDocument2 pagesLiran Ben Asuly - CVBaizhan TuyakbayNo ratings yet

- Dfi 501 Course OutlineDocument3 pagesDfi 501 Course OutlineblackshizoNo ratings yet

- Value Chain AnalysisDocument76 pagesValue Chain AnalysisA B M Rafiqul Hasan Khan67% (3)

- Noida, Hyderabad: India Locations-Mumbai, New Delhi, Gurgaon, Banglore, Chennai, PuneDocument4 pagesNoida, Hyderabad: India Locations-Mumbai, New Delhi, Gurgaon, Banglore, Chennai, PunesujeetkrNo ratings yet

- 2nd Meeting - Mind Map C. 2 - Introduction To Cost Terms and Cost Purposes - A3 PDFDocument1 page2nd Meeting - Mind Map C. 2 - Introduction To Cost Terms and Cost Purposes - A3 PDFIsna Fauziah BiljannahNo ratings yet

- HuaweiDocument10 pagesHuaweiمهدي مهديNo ratings yet

- Introduction To MicroeconomicsDocument43 pagesIntroduction To MicroeconomicsVũ Thùy DươngNo ratings yet

- Pas 11Document2 pagesPas 11AngelicaNo ratings yet

- Taxation (United Kingdom) : Tuesday 12 June 2012Document12 pagesTaxation (United Kingdom) : Tuesday 12 June 2012Iftekhar IfteNo ratings yet

- Concept Map On IAS 12 - Income TaxesDocument2 pagesConcept Map On IAS 12 - Income TaxesRey OnateNo ratings yet

- Cost Volume Profit AnalysisDocument7 pagesCost Volume Profit AnalysisMeng DanNo ratings yet

- What Good Can One Solor Light Do ?Document5 pagesWhat Good Can One Solor Light Do ?ஷாலினி Shaliny Panneir SelvamNo ratings yet

- Case in Financial Management-Case 14, Triad CampDocument13 pagesCase in Financial Management-Case 14, Triad CampIbah JungminNo ratings yet

- 01-09-2015 PDFDocument4 pages01-09-2015 PDFWa Riz LaiNo ratings yet

- EON Annual Report 2014 enDocument232 pagesEON Annual Report 2014 enlajosNo ratings yet

- Investor AgreementDocument4 pagesInvestor AgreementAshmika RajNo ratings yet

- Kochi Airport - PPP Model Study: A Project OnDocument10 pagesKochi Airport - PPP Model Study: A Project Onsankhaghosh04No ratings yet