You might also like

- Poverty and the Policy Response to the Economic Crisis in LiberiaFrom EverandPoverty and the Policy Response to the Economic Crisis in LiberiaNo ratings yet

- ShumoDocument39 pagesShumolemesa abdisaNo ratings yet

- Project Report: Annexure-1Document15 pagesProject Report: Annexure-1Epsita PaulNo ratings yet

- Banking and Insurance Law Assignment (Abhinav)Document18 pagesBanking and Insurance Law Assignment (Abhinav)Samiksha SakshiNo ratings yet

- A Web Based Application For Automating Bank Loan Eligibility Using Machine LearningDocument43 pagesA Web Based Application For Automating Bank Loan Eligibility Using Machine LearningPatrick NgaboNo ratings yet

- Business Law 2Document23 pagesBusiness Law 2Karman AulakhNo ratings yet

- A Study of E-Commerce SiteDocument21 pagesA Study of E-Commerce SiteBndn GemereNo ratings yet

- Abdurhman DekeboDocument85 pagesAbdurhman DekeboAdem EsmaelNo ratings yet

- Library Management System Document CompleteDocument33 pagesLibrary Management System Document CompletemogirejudNo ratings yet

- Mba ProjectDocument100 pagesMba ProjectRajat Aneja67% (3)

- Kirui - The Effect of Internet Banking On Kenya S Economic DevelopmentDocument55 pagesKirui - The Effect of Internet Banking On Kenya S Economic DevelopmentNJUGUNA AUSTIN KIMUHUNo ratings yet

- Torts Shaurya Sir 2Document25 pagesTorts Shaurya Sir 2ShauryaNo ratings yet

- An Report On Digitalization in Banking in NepalDocument21 pagesAn Report On Digitalization in Banking in Nepalanimeninja224No ratings yet

- Graduation Project ReportDocument38 pagesGraduation Project ReportHamdallah Anwar KhasawnehNo ratings yet

- Gram Edited Final Year Project Proposal (Karani Jackson Muthoi J77-11807-2017)Document51 pagesGram Edited Final Year Project Proposal (Karani Jackson Muthoi J77-11807-2017)muthoijackson93No ratings yet

- Research ReportDocument63 pagesResearch ReportwinfridamdeeNo ratings yet

- Project Report On Liability Towards Dishonor ofDocument55 pagesProject Report On Liability Towards Dishonor ofdjdavidjose640% (5)

- Online Banking in India: Submitted byDocument20 pagesOnline Banking in India: Submitted byAastha PrakashNo ratings yet

- Online Clothes Rent Application Using Mern-01!06!2022Document21 pagesOnline Clothes Rent Application Using Mern-01!06!2022paudelayush999No ratings yet

- Full Current 2Document172 pagesFull Current 2Haizum Binti Hasbi StudentNo ratings yet

- CompleteresearchpaperDocument42 pagesCompleteresearchpaperGirish SahooNo ratings yet

- Complete Research PaperDocument43 pagesComplete Research PaperBrian JabaliNo ratings yet

- The Suits Concerning Patent Infringement: (Hons.) During The Academic Year 2021-2022Document28 pagesThe Suits Concerning Patent Infringement: (Hons.) During The Academic Year 2021-2022sakshi tiwariNo ratings yet

- E Website Repot ItDocument39 pagesE Website Repot ItAniket pandeyNo ratings yet

- Anita Pieterson PDFDocument78 pagesAnita Pieterson PDFSachie BeeNo ratings yet

- Mohit Final Sip 112Document45 pagesMohit Final Sip 112palak dNo ratings yet

- Skripsi Luky Fitri AngrainiDocument110 pagesSkripsi Luky Fitri AngrainiMebratu BirhanuNo ratings yet

- Musau Final ProposalDocument54 pagesMusau Final Proposaldanilomusau04No ratings yet

- Mini Dissertaion-Research Methods-Group 3Document58 pagesMini Dissertaion-Research Methods-Group 3Najaah RujuballyNo ratings yet

- Project ReportDocument73 pagesProject ReportMitali RajNo ratings yet

- SIP Report Bajaj Finserv Updated - NiharikaDocument44 pagesSIP Report Bajaj Finserv Updated - NiharikaAniket AgrahariNo ratings yet

- Sang Cherono Project1Document54 pagesSang Cherono Project1shadrackkipkemoi647No ratings yet

- Oromo - The Relationship Between Mobile Money and Loans Issued by Commercial Banks in KenyaDocument56 pagesOromo - The Relationship Between Mobile Money and Loans Issued by Commercial Banks in KenyaNatinael AbebeNo ratings yet

- Doreen FinalDocument40 pagesDoreen Finalgeorgeodhiambo840No ratings yet

- Emily Final DocumentDocument64 pagesEmily Final DocumentmjNo ratings yet

- MMS 22 24 C64 BBDocument93 pagesMMS 22 24 C64 BBS H RE ENo ratings yet

- Aheza BerheDocument64 pagesAheza BerheOnnatan DinkaNo ratings yet

- Banking LawDocument37 pagesBanking LawavniNo ratings yet

- BBA Batch 11 Morning Prakash Regmi PW Report Puja SahDocument90 pagesBBA Batch 11 Morning Prakash Regmi PW Report Puja Sahrajeev85.1thapaNo ratings yet

- 9236 AmitkumarDocument71 pages9236 AmitkumarAmit Kumar BaraiNo ratings yet

- Annrose Karanja FinalDocument55 pagesAnnrose Karanja Finalshadrackkipkemoi647No ratings yet

- Aklilu Tekle PDFDocument71 pagesAklilu Tekle PDFTILAHUNNo ratings yet

- Cost Benefit Analysis of Digital BankingDocument47 pagesCost Benefit Analysis of Digital Bankingterefelign melesNo ratings yet

- MMS 22 24 C64 BBDocument88 pagesMMS 22 24 C64 BBS H RE ENo ratings yet

- Final Report Muhammad Fakhri I17012347Document69 pagesFinal Report Muhammad Fakhri I17012347Muhammad FakhriNo ratings yet

- IT19000886Document28 pagesIT19000886Harish KumarNo ratings yet

- SLR - Ram AurangabadkarDocument82 pagesSLR - Ram AurangabadkarOjas KamthikarNo ratings yet

- Full Text 01Document79 pagesFull Text 01Shlesha NarvekarNo ratings yet

- Yogita Suresh Daranea - Study On E-BankingDocument91 pagesYogita Suresh Daranea - Study On E-Bankingprahlad prajapatiNo ratings yet

- BrendanDocument49 pagesBrendanDOUGLAS NYONGESANo ratings yet

- Appraisal of Judicial Reforms Towards An EfficientDocument137 pagesAppraisal of Judicial Reforms Towards An EfficientRegina KateNo ratings yet

- Project - Online Banking SystemDocument25 pagesProject - Online Banking SystemEpsita PaulNo ratings yet

- Yvee System DocumentationDocument47 pagesYvee System DocumentationYvettee NdlovuNo ratings yet

- AT Sharekhan LTD Hyderabad: A Comparative Study On Online Trading of Share Prices of Banking SectorDocument86 pagesAT Sharekhan LTD Hyderabad: A Comparative Study On Online Trading of Share Prices of Banking Sectorsheikh129No ratings yet

- Ayelech EsheteDocument112 pagesAyelech Esheteawel centerNo ratings yet

- Factors Affecting Electronic Filing of Returns Among Medium EnterprisesDocument53 pagesFactors Affecting Electronic Filing of Returns Among Medium EnterprisesJoh TzNo ratings yet

- Tourism Management SystemDocument29 pagesTourism Management SystemKushal SharmaNo ratings yet

- Proposal Real BookDocument30 pagesProposal Real BookDa udNo ratings yet

- Niyonzima Louis PDFDocument61 pagesNiyonzima Louis PDFNadine ITUZENo ratings yet

- Final BankingDocument27 pagesFinal BankingshubhiNo ratings yet

- Prospective Operation of Statutes: A StudyDocument5 pagesProspective Operation of Statutes: A Studysakshi tiwariNo ratings yet

- Central University of South Bihar: School of Law & GovernanceDocument21 pagesCentral University of South Bihar: School of Law & GovernanceSHREY BHUSHANNo ratings yet

- Company Law Assignment MoaDocument1 pageCompany Law Assignment Moasakshi tiwariNo ratings yet

- Discharge JudgmentDocument3 pagesDischarge Judgmentsakshi tiwariNo ratings yet

- II Fdi IIDocument16 pagesII Fdi IIsakshi tiwariNo ratings yet

- Advocates and Contempt of Court - 682 - Ketana KrishnaDocument13 pagesAdvocates and Contempt of Court - 682 - Ketana KrishnaUtkarshJhinganNo ratings yet

- Rebate Under Section 80 of Income Tax ActDocument21 pagesRebate Under Section 80 of Income Tax Actsakshi tiwariNo ratings yet

- Sunil Bharti Mittal Vs N Naresh Kumar 2019Document5 pagesSunil Bharti Mittal Vs N Naresh Kumar 2019sakshi tiwariNo ratings yet

- PG 736 Ibid, Citation No. 64, PG 740 Look Citation 19 Supra 1 PG 743Document2 pagesPG 736 Ibid, Citation No. 64, PG 740 Look Citation 19 Supra 1 PG 743sakshi tiwariNo ratings yet

- Relief and 20Document18 pagesRelief and 20sakshi tiwariNo ratings yet

- The Locus Standi Conundrum: Samir Agarwal V. Cci: Sakshi Tiwari & Mayank KumarDocument2 pagesThe Locus Standi Conundrum: Samir Agarwal V. Cci: Sakshi Tiwari & Mayank Kumarsakshi tiwariNo ratings yet

- Labour LawDocument23 pagesLabour Lawsakshi tiwariNo ratings yet

- The Suits Concerning Patent Infringement: (Hons.) During The Academic Year 2021-2022Document28 pagesThe Suits Concerning Patent Infringement: (Hons.) During The Academic Year 2021-2022sakshi tiwariNo ratings yet

- Labour LawDocument23 pagesLabour Lawsakshi tiwariNo ratings yet

- Rajit Ram & Ors. V. Kateskar Nath & Ors. (1896) ILR 18 ALL 396Document21 pagesRajit Ram & Ors. V. Kateskar Nath & Ors. (1896) ILR 18 ALL 396sakshi tiwariNo ratings yet

- Administrative LAW I Final Draft - Sakshi Tiwari - 2035Document23 pagesAdministrative LAW I Final Draft - Sakshi Tiwari - 2035sakshi tiwariNo ratings yet

- Date EventDocument1 pageDate Eventsakshi tiwariNo ratings yet

- ARGUMENTS ADVANCED Special IntraDocument7 pagesARGUMENTS ADVANCED Special Intrasakshi tiwariNo ratings yet

- Environmental Law Final ProjectDocument30 pagesEnvironmental Law Final Projectpraharshitha100% (1)

- Sakshi Tiwari - 2035 - Administrative Law I RDDocument4 pagesSakshi Tiwari - 2035 - Administrative Law I RDsakshi tiwariNo ratings yet

- Gi 2021Document1 pageGi 2021sakshi tiwariNo ratings yet

- ADR Final Draft - Sakshi Tiwari - 2035Document28 pagesADR Final Draft - Sakshi Tiwari - 2035sakshi tiwariNo ratings yet

- ARGUMENTS ADVANCED Special IntraDocument7 pagesARGUMENTS ADVANCED Special Intrasakshi tiwariNo ratings yet

- Geography ProjectDocument43 pagesGeography Projectsakshi tiwariNo ratings yet

- ADR Final Draft - Sakshi TiwariDocument28 pagesADR Final Draft - Sakshi Tiwarisakshi tiwariNo ratings yet

- CPC Final Draft - Sakshi Tiwari - 2035Document31 pagesCPC Final Draft - Sakshi Tiwari - 2035sakshi tiwariNo ratings yet

- Family Law 2 ProjectDocument31 pagesFamily Law 2 Projectsakshi tiwariNo ratings yet

- JURISPRUDENCE I - FINAL DRAFT - SakshiTiwari - 2035Document20 pagesJURISPRUDENCE I - FINAL DRAFT - SakshiTiwari - 2035sakshi tiwariNo ratings yet

- Family Law 2 ProjectDocument31 pagesFamily Law 2 Projectsakshi tiwariNo ratings yet

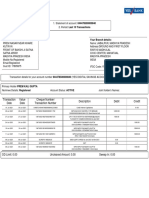

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument10 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceYeshwanth SunkaraNo ratings yet

- Dear Customer Welcome To JS Bank E-Statement !Document3 pagesDear Customer Welcome To JS Bank E-Statement !Honey JanNo ratings yet

- 11FS Rebuilding Financial Services From The InsideDocument58 pages11FS Rebuilding Financial Services From The InsideJose TC NetoNo ratings yet

- Tax Invoice: Billing Address Installation Address Invoice DetailsDocument1 pageTax Invoice: Billing Address Installation Address Invoice DetailsShetkar GouthamNo ratings yet

- SOADocument2 pagesSOAJonathan Peter Del RosarioNo ratings yet

- mt101 ManualDocument53 pagesmt101 ManualNestor Julio Arias MonáNo ratings yet

- Account Statement For The Account: 3127000108458731: Branch DetailsDocument8 pagesAccount Statement For The Account: 3127000108458731: Branch DetailsDEVENDRA KUMAR SHEETAL0% (1)

- Transactions 600 051949600 20220324 160153Document2 pagesTransactions 600 051949600 20220324 160153Hemanth Kumar NNo ratings yet

- Acct Statement XX0947 20102022Document62 pagesAcct Statement XX0947 2010202227 Vishal HadiyaNo ratings yet

- Latin America Payments Solution: November 2018Document19 pagesLatin America Payments Solution: November 2018Jairo MartinezNo ratings yet

- Mastercard Rules PDFDocument353 pagesMastercard Rules PDFSamir MadanNo ratings yet

- Main Acct Statemetn Jan To Dec 17Document11 pagesMain Acct Statemetn Jan To Dec 17Col RajNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument15 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceMaulik PatelNo ratings yet

- Your Branch Details:: Transaction Date Value Date Cheque Number/ Transaction Number Description Debit CreditDocument1 pageYour Branch Details:: Transaction Date Value Date Cheque Number/ Transaction Number Description Debit CreditSagar GuptaNo ratings yet

- Penyata BSNDocument12 pagesPenyata BSNQaf QayyumNo ratings yet

- On Line Audit 2Document2 pagesOn Line Audit 2Nicolas ErnestoNo ratings yet

- N 8 SZIB6 Otr UHQAZmDocument3 pagesN 8 SZIB6 Otr UHQAZmOmkar LolgeNo ratings yet

- Syahriah 12 PutraDocument3 pagesSyahriah 12 PutraAkhmad TajuddinNo ratings yet

- McClellan Volume OscillatorDocument24 pagesMcClellan Volume Oscillatorapi-26898051No ratings yet

- SepaDirectDebit FromExcelToPain v1Document15 pagesSepaDirectDebit FromExcelToPain v1Devesh RawatNo ratings yet

- Bank 1Document91 pagesBank 1trainticket5598No ratings yet

- Account Summary: AccountsDocument4 pagesAccount Summary: AccountsFahad ZaidNo ratings yet

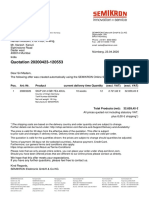

- Quotation 20200423-120553: Pos. Art.-Nr. Product Current Delivery Time Quantity Unit Price (Excl. VAT) Total (Excl. VAT)Document1 pageQuotation 20200423-120553: Pos. Art.-Nr. Product Current Delivery Time Quantity Unit Price (Excl. VAT) Total (Excl. VAT)kanrinareshNo ratings yet

- Revolut Payments Personal Terms and SupplementDocument40 pagesRevolut Payments Personal Terms and SupplementLarisa Mihaela SfătuțăNo ratings yet

- Fintech Regulations: Emerson S. Banez UP College of LawDocument37 pagesFintech Regulations: Emerson S. Banez UP College of LawMike E DmNo ratings yet

- 4444 17789 1 PBDocument20 pages4444 17789 1 PBHossain Moulude TejoNo ratings yet

- MTN Invoice - Oct 2021Document2 pagesMTN Invoice - Oct 2021Nana Kwame MensahNo ratings yet

- Fintech in Investment ManagementDocument3 pagesFintech in Investment ManagementFundamental researchersNo ratings yet

- Etickets PDFDocument3 pagesEtickets PDFblue fireNo ratings yet

- Ams InvoiceDocument2 pagesAms InvoiceChristine NgemaNo ratings yet