You might also like

- Í Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaDocument3 pagesÍ Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaJoshua M. GenoviaNo ratings yet

- Market Structure and Pricing PoliciesDocument32 pagesMarket Structure and Pricing PoliciesSharanya Ramesh100% (1)

- Unit 3 Study GuideDocument3 pagesUnit 3 Study Guide高瑞韩No ratings yet

- EFE MATRIX Khaadi.Document4 pagesEFE MATRIX Khaadi.Maryam MaqsoodNo ratings yet

- Meaning of Market StructureDocument18 pagesMeaning of Market StructureAbhishek Yadav100% (2)

- Learn Financial ReportsDocument6 pagesLearn Financial ReportsMai RuizNo ratings yet

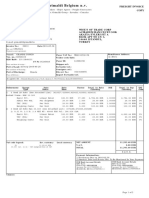

- Grimaldi Belgium N.V.: Freight InvoiceDocument2 pagesGrimaldi Belgium N.V.: Freight InvoiceAyseColakNo ratings yet

- The UltimaDocument18 pagesThe Ultimadoc purushottamNo ratings yet

- Korean Economy EvolutionDocument57 pagesKorean Economy EvolutionHanya LariosNo ratings yet

- Green Agrevolution PVT LTDDocument16 pagesGreen Agrevolution PVT LTDCharanmadhav KorrapatiNo ratings yet

- Direct Hydrothermal Treatment of Sugarcane Juice For 3D Oxygen Rich Carbon Aerogel NiCo2O4 Based SupercapacitorDocument12 pagesDirect Hydrothermal Treatment of Sugarcane Juice For 3D Oxygen Rich Carbon Aerogel NiCo2O4 Based SupercapacitorAnh DuyNo ratings yet

- Important Questions For CBSE Class 8 Social Science Our Past 3 Chapter 9 - The Making of The National Movement - 1870s - 1947Document8 pagesImportant Questions For CBSE Class 8 Social Science Our Past 3 Chapter 9 - The Making of The National Movement - 1870s - 1947Megha TalukdarNo ratings yet

- CA Chapter 16-02 Monopolistic CompetitionDocument11 pagesCA Chapter 16-02 Monopolistic CompetitionYasmine JazzNo ratings yet

- Sept 2022 Belmont Poll Release - FinalDocument3 pagesSept 2022 Belmont Poll Release - FinalJack SterneNo ratings yet

- Chapter 7Document37 pagesChapter 7Kenneth Wen Xuan TiongNo ratings yet

- Social Science (087) Set 32 C 123 Marking Scheme Comptt 2020Document18 pagesSocial Science (087) Set 32 C 123 Marking Scheme Comptt 2020hacker GodNo ratings yet

- MBA Exam Case Study: Should Nozer Mobikes Go PublicDocument3 pagesMBA Exam Case Study: Should Nozer Mobikes Go PublicAnkita PrasadNo ratings yet

- 16way NTG ManualDocument62 pages16way NTG ManualSavinda JanszNo ratings yet

- IS 7903 StandardsDocument14 pagesIS 7903 StandardsCHIRAG PATELNo ratings yet

- Project ReportDocument46 pagesProject ReportDigi SalesNo ratings yet

- Essential Reading 5Document16 pagesEssential Reading 5kevinballesterosNo ratings yet

- What is Spread Betting? The Basics, Risks and StrategiesDocument4 pagesWhat is Spread Betting? The Basics, Risks and StrategiesMyriam GrissaNo ratings yet

- Project Report: PSIT College of Higher Education, Bhauti, KanpurDocument52 pagesProject Report: PSIT College of Higher Education, Bhauti, KanpurAshutosh SinghNo ratings yet

- Lecture Notes International EconomicsDocument105 pagesLecture Notes International EconomicsWilliam HeffnerNo ratings yet

- Multiple Choice Questions 1 According To The Crowding Out EffeDocument2 pagesMultiple Choice Questions 1 According To The Crowding Out Effetrilocksp SinghNo ratings yet

- HBSE 11th Business Studies 2018 PaperDocument7 pagesHBSE 11th Business Studies 2018 PaperRajiv KharbandaNo ratings yet

- PGR 2022-00031 - Order Instituting PGR (Grecia D'702)Document16 pagesPGR 2022-00031 - Order Instituting PGR (Grecia D'702)Sarah BursteinNo ratings yet

- Determinants of Poverty in South AfricaDocument19 pagesDeterminants of Poverty in South AfricaibsaNo ratings yet

- Chapter 14 Firms in Competitive Markets PDFDocument38 pagesChapter 14 Firms in Competitive Markets PDFWasiq BhuiyanNo ratings yet

- International Finance: Ibf301 - FPT Universit YDocument43 pagesInternational Finance: Ibf301 - FPT Universit YĐặng Quỳnh TrangNo ratings yet

- Test Topic 1 and 2 ESSDocument12 pagesTest Topic 1 and 2 ESSBaichu Deepa DeviNo ratings yet

- Understanding Business EnvironmentDocument75 pagesUnderstanding Business EnvironmentRAVI PRASAD KUSHWAHANo ratings yet

- DPR - KING Chili CCPUR NEWDocument37 pagesDPR - KING Chili CCPUR NEWAIWVS ManipurNo ratings yet

- Tci 903SDocument8 pagesTci 903SomarhanandehNo ratings yet

- Parents Handbookof Professional Careersafter 10th/12thDocument29 pagesParents Handbookof Professional Careersafter 10th/12thaadal arasuNo ratings yet

- Study of Sinhgad FortDocument9 pagesStudy of Sinhgad FortTejas MahajanNo ratings yet

- Jaipur To IndoreDocument1 pageJaipur To IndoreVINAY BANSALNo ratings yet

- Academic Year 2022Document41 pagesAcademic Year 2022Skylar RingtonesNo ratings yet

- Adobe Scan Mar 22, 2023Document5 pagesAdobe Scan Mar 22, 2023Lay MahantNo ratings yet

- Yoga and Meditation PankDocument21 pagesYoga and Meditation PankSikha SharmaNo ratings yet

- Unethical Behavior of Tesco PLCDocument5 pagesUnethical Behavior of Tesco PLCNicole AgustinNo ratings yet

- Iic Pub G1 V1.80 2017-01-31Document58 pagesIic Pub G1 V1.80 2017-01-31Pema Chentsho100% (1)

- 2.mold Tek Packaging Initial (ICICI)Document14 pages2.mold Tek Packaging Initial (ICICI)beza manojNo ratings yet

- 10 Sneaky Marketing Ploys ExplainedDocument15 pages10 Sneaky Marketing Ploys ExplainedElica DiazNo ratings yet

- Orientation Programme 2022 23 New StudentsDocument22 pagesOrientation Programme 2022 23 New StudentsR majumdar100% (1)

- Tempo ReformsDocument3 pagesTempo ReformsBarnali RayNo ratings yet

- Chapter 10 Managerial Econ LessonDocument8 pagesChapter 10 Managerial Econ LessonAngelica Joy ManaoisNo ratings yet

- Market and Pricing StrategiesDocument27 pagesMarket and Pricing StrategiesIzzatullah JanNo ratings yet

- ECO XII - Topic X (FORMS OF MARKET)Document17 pagesECO XII - Topic X (FORMS OF MARKET)Tanisha PoddarNo ratings yet

- Market Structure and Pricing PracticesDocument14 pagesMarket Structure and Pricing Practicesdurgesh7998No ratings yet

- Market Structure ExplainedDocument5 pagesMarket Structure ExplainedPamela SantiagoNo ratings yet

- Market Structure Types Perfect Competition Monopolistic Competition Oligopoly MonopolyDocument21 pagesMarket Structure Types Perfect Competition Monopolistic Competition Oligopoly MonopolyLizza AlipioNo ratings yet

- Unit 5Document50 pagesUnit 5NEENA SARA THOMAS 2227432No ratings yet

- Market Structure & Pricing DecisionsDocument6 pagesMarket Structure & Pricing DecisionsDivyang BhattNo ratings yet

- Unit - 04 MBA 02Document5 pagesUnit - 04 MBA 02Himanshu AwasthiNo ratings yet

- Chapter-10 (Microeconomics) Forms of MarketDocument8 pagesChapter-10 (Microeconomics) Forms of MarketSourav KumarNo ratings yet

- Lecture 25Document7 pagesLecture 25RohitPatialNo ratings yet

- Me 4 (Part A)Document6 pagesMe 4 (Part A)Anuj YadavNo ratings yet

- FORMS OF MARKET STRUCTURESDocument4 pagesFORMS OF MARKET STRUCTURESSaurabhNo ratings yet

- Economics Monopoly NewDocument19 pagesEconomics Monopoly NewBhavin patelNo ratings yet

- Module 5 (Rev)Document7 pagesModule 5 (Rev)Meian De JesusNo ratings yet

- Bs. Economics 1Document17 pagesBs. Economics 1UmeshNo ratings yet

- Unit IV - (Managerial Economics) Market Structures & Pricing StrategiesDocument37 pagesUnit IV - (Managerial Economics) Market Structures & Pricing StrategiesAbhinav SachdevaNo ratings yet

- Main Market FormsDocument9 pagesMain Market FormsP Janaki Raman50% (2)

- Unit - Iii Markets and Economic EnvironmentDocument29 pagesUnit - Iii Markets and Economic Environmentpinnamaraju kavyaNo ratings yet

- Unit IV V and VIDocument57 pagesUnit IV V and VIrosieNo ratings yet

- Unit-2 Sadp: N.Mounika Asst - Professor Dept of Cse UrceDocument26 pagesUnit-2 Sadp: N.Mounika Asst - Professor Dept of Cse UrcerosieNo ratings yet

- Route OptimizationDocument11 pagesRoute OptimizationrosieNo ratings yet

- R-16 IV/I Unit-I: HTML, Css UNIT-II: Java Script Unit-Iii: XML, Ajax Unit-Iv: PHP Unit-V: Perl Unit-Vi: RubyDocument273 pagesR-16 IV/I Unit-I: HTML, Css UNIT-II: Java Script Unit-Iii: XML, Ajax Unit-Iv: PHP Unit-V: Perl Unit-Vi: RubyrosieNo ratings yet

- RubyDocument40 pagesRubyrosieNo ratings yet

- Packet Delivery and Handover ManagementDocument18 pagesPacket Delivery and Handover ManagementrosieNo ratings yet

- Mefa NotesDocument80 pagesMefa NotesrosieNo ratings yet

- Mefa Vi UnitDocument12 pagesMefa Vi UnitrosieNo ratings yet

- Mefa Unit-4Document8 pagesMefa Unit-4rosieNo ratings yet

- Unit - Iii Mobile Network Layer: IP and Mobile IPDocument15 pagesUnit - Iii Mobile Network Layer: IP and Mobile IProsieNo ratings yet

- Managerial Economics and Financial Analysis Unit-2 ProductionDocument14 pagesManagerial Economics and Financial Analysis Unit-2 ProductionrosieNo ratings yet

- Unit - 4 PHPDocument45 pagesUnit - 4 PHProsieNo ratings yet

- Cns r16 Unit 6 1Document17 pagesCns r16 Unit 6 1rosieNo ratings yet

- CNS (R16) B.Tech (CSE) IV Year I SemDocument34 pagesCNS (R16) B.Tech (CSE) IV Year I SemrosieNo ratings yet

- Dbms Interview QuestionsDocument20 pagesDbms Interview QuestionsrosieNo ratings yet

- Advantages of CSS StylingDocument19 pagesAdvantages of CSS StylingrosieNo ratings yet

- F 1040 SBDocument2 pagesF 1040 SBapi-252942620No ratings yet

- Differences between prime rate, discount rate and federal funds rateDocument4 pagesDifferences between prime rate, discount rate and federal funds rateTeffi Boyer MontoyaNo ratings yet

- Tax Invoice: INVOICE NO. B2320473 21.12.2022 Invoice / Issue DateDocument1 pageTax Invoice: INVOICE NO. B2320473 21.12.2022 Invoice / Issue DateRanjith PatelNo ratings yet

- Tarun Project FileDocument32 pagesTarun Project FileTushar SikarwarNo ratings yet

- Manufacturing Account Worked Example Question 12Document6 pagesManufacturing Account Worked Example Question 12Roshan RamkhalawonNo ratings yet

- Causes and Types of Poverty ExplainedDocument13 pagesCauses and Types of Poverty ExplainedShruti SinghNo ratings yet

- Exercise 1 Demand Theory and Elasticities01Document3 pagesExercise 1 Demand Theory and Elasticities01Muhammad FikryNo ratings yet

- Ceres Gardening Company Case StudyDocument3 pagesCeres Gardening Company Case StudyBadri Narayan MishraNo ratings yet

- Annual Financial Statements of The ChurchDocument9 pagesAnnual Financial Statements of The ChurchKath Nidoy RoderoNo ratings yet

- MAHINDRA AND MAHINDRA FINANCIAL SERVICES LTD. Financial Results July 2021Document20 pagesMAHINDRA AND MAHINDRA FINANCIAL SERVICES LTD. Financial Results July 2021mukesh bhattNo ratings yet

- FIN Chapter 6 - V1Document44 pagesFIN Chapter 6 - V1foysalNo ratings yet

- 2008tpu PDFDocument207 pages2008tpu PDFMicrosoft SumberdjantinNo ratings yet

- Private Capital MobilizationDocument486 pagesPrivate Capital MobilizationHallo SunshineNo ratings yet

- Investment Banker ResumeDocument1 pageInvestment Banker ResumeJerry PasaribuNo ratings yet

- Physical Delivery Guide: Page 1 of 79Document79 pagesPhysical Delivery Guide: Page 1 of 79maheshNo ratings yet

- RBI guidelines on transferring borrowal accounts between banksDocument8 pagesRBI guidelines on transferring borrowal accounts between banksSatish SolankiNo ratings yet

- Final Exam Study GuideDocument9 pagesFinal Exam Study GuideDognimin Aboudramane KonateNo ratings yet

- Schreiben BZBM - MR Le Maire de DoualaDocument2 pagesSchreiben BZBM - MR Le Maire de DoualaMohamed ElkatibNo ratings yet

- Public Econ BookDocument172 pagesPublic Econ BookSuhas KandeNo ratings yet

- Case StudyDocument28 pagesCase StudyNCP Shem ManaoisNo ratings yet

- 02 0 The Engulfing Lights, Using Engulfing Patterns As Traffic LightsDocument16 pages02 0 The Engulfing Lights, Using Engulfing Patterns As Traffic Lightsmikestar_tarNo ratings yet

- WRSX External Environment - Phase 1 Produced by Andy Carnelley, WRSX Business AnalystDocument4 pagesWRSX External Environment - Phase 1 Produced by Andy Carnelley, WRSX Business AnalystQuinn Tavious TaylorNo ratings yet

- DG - 0015 PDFDocument1 pageDG - 0015 PDFGasBuddyNo ratings yet

- The Factors Influencing Bank Credit Risk: The Case of TunisiaDocument9 pagesThe Factors Influencing Bank Credit Risk: The Case of TunisiaAhanafNo ratings yet

- Role Leader Achieve Employee PerformanceDocument5 pagesRole Leader Achieve Employee PerformanceMohammad ErwanNo ratings yet