You might also like

- Management & Financial AccountingDocument390 pagesManagement & Financial AccountingParveen KumarNo ratings yet

- How To Value A Business - Presentation For Sustainable Business Network of Philadelphia - February 25, 2014Document36 pagesHow To Value A Business - Presentation For Sustainable Business Network of Philadelphia - February 25, 2014Michael CunninghamNo ratings yet

- 2019 Mock Exam A - Afternoon Session PDFDocument23 pages2019 Mock Exam A - Afternoon Session PDFDhruva Sareen Consultancy100% (1)

- Employee Resignation Process FlowchartDocument1 pageEmployee Resignation Process FlowchartJayvee BernalNo ratings yet

- Fa Class Notes UplodedDocument252 pagesFa Class Notes UplodedDurvas Karmarkar100% (1)

- Accounts Volume 1Document503 pagesAccounts Volume 1Utkarsh100% (1)

- ACC 203 module explores conceptual framework and financial reportingDocument127 pagesACC 203 module explores conceptual framework and financial reportingAsi Cas Jav67% (3)

- 7001 Assignment #2Document11 pages7001 Assignment #2南玖No ratings yet

- Case Financial Performance - PT TimahDocument14 pagesCase Financial Performance - PT TimahIto PuruhitoNo ratings yet

- Integ Acc FinalsDocument201 pagesInteg Acc FinalsBack upNo ratings yet

- Advances and Expenses GuideDocument22 pagesAdvances and Expenses GuideDebarati BoseNo ratings yet

- Ch04 SM Larson Fap15Document143 pagesCh04 SM Larson Fap15Paul Hrynew100% (1)

- Ohada Accounting Plan PDFDocument72 pagesOhada Accounting Plan PDFNchendeh Christian50% (2)

- Heritage Economics +A Conceptual Frameowrk - D ThrosbyDocument30 pagesHeritage Economics +A Conceptual Frameowrk - D ThrosbyshahimabduNo ratings yet

- Highland Malt Inc Calculation of Financial Ratios 2019 2018 1. Liquidity Ratios $ $Document12 pagesHighland Malt Inc Calculation of Financial Ratios 2019 2018 1. Liquidity Ratios $ $TylerNo ratings yet

- Business Plan of FOODHUBDocument12 pagesBusiness Plan of FOODHUBAmit SharmaNo ratings yet

- Oracle Fixed Assets - Implementation Tips and StrategiesDocument27 pagesOracle Fixed Assets - Implementation Tips and Strategiesiam_narayanan100% (2)

- Chapter 1 - Review of Accounting ProcessDocument13 pagesChapter 1 - Review of Accounting ProcessJam100% (1)

- BAFACR16 01 FS PresentationDocument15 pagesBAFACR16 01 FS PresentationThats BellaNo ratings yet

- CM3 PAS1R Presentation of Financial StatementsDocument15 pagesCM3 PAS1R Presentation of Financial StatementsMark GerwinNo ratings yet

- SLIDES UNIT 6 Part 2Document22 pagesSLIDES UNIT 6 Part 2joseguticast99No ratings yet

- Module 1Document23 pagesModule 1esparagozanichole01No ratings yet

- IC102 Accounting 1 (Week 7 M3-L3) - HandoutsDocument27 pagesIC102 Accounting 1 (Week 7 M3-L3) - HandoutsLj TvNo ratings yet

- Quiz-2 Financial Acctg & ReportingDocument3 pagesQuiz-2 Financial Acctg & ReportingDanica Saraus DomughoNo ratings yet

- Accounting Technicians Scheme (West Africa) : Basic Accounting Processes & Systems (BAPS)Document428 pagesAccounting Technicians Scheme (West Africa) : Basic Accounting Processes & Systems (BAPS)Ibrahim MuyeNo ratings yet

- B215 AC01 - Numbers and Words - 6th Presentation - 17apr2009Document23 pagesB215 AC01 - Numbers and Words - 6th Presentation - 17apr2009tohqinzhiNo ratings yet

- CM1 PAS1 Presentation of Financial StatementsDocument16 pagesCM1 PAS1 Presentation of Financial StatementsMark GerwinNo ratings yet

- University of Saint Louis Tuguegarao City School of Accountancy, Business and Hospitality First Semester A.Y. 2020-2021Document8 pagesUniversity of Saint Louis Tuguegarao City School of Accountancy, Business and Hospitality First Semester A.Y. 2020-2021Annie RapanutNo ratings yet

- Module 11 ICT 141Document3 pagesModule 11 ICT 141Janice SeterraNo ratings yet

- Week 6 Lecture Notes (1 Slide) PDFDocument48 pagesWeek 6 Lecture Notes (1 Slide) PDFSharon LiNo ratings yet

- Nature of Financial Accounting: Faculty of Economy and Business Mercubuana University 2018Document15 pagesNature of Financial Accounting: Faculty of Economy and Business Mercubuana University 2018AgusMaulanaEntrepreneurshipSuksesNo ratings yet

- Instant Download Ebook PDF Accounting Basic Reports 10th Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Accounting Basic Reports 10th Edition PDF Scribdphyllis.rodriguez580100% (43)

- Accounting Module OverviewDocument23 pagesAccounting Module OverviewMa Leah TañezaNo ratings yet

- Government AccountingDocument28 pagesGovernment AccountingRazel TercinoNo ratings yet

- FINANCIAL STATEMENT LECTUREDocument33 pagesFINANCIAL STATEMENT LECTUREkacaribuantonNo ratings yet

- Accounting+ Chapter 1Document21 pagesAccounting+ Chapter 1pronab kumarNo ratings yet

- Institute-University School of Business Department-MbaDocument12 pagesInstitute-University School of Business Department-MbaAbhishek kumarNo ratings yet

- Q .1 Explain Meaning of Accounting and Process of Accounting?Document4 pagesQ .1 Explain Meaning of Accounting and Process of Accounting?Sahil Kumar GuptaNo ratings yet

- Comparative FSs 6Document21 pagesComparative FSs 6Shierwin Ebcas JavierNo ratings yet

- Bookkeeping: CILO 1: Understand The Accounting ProcessDocument40 pagesBookkeeping: CILO 1: Understand The Accounting ProcessNeama1 RadhiNo ratings yet

- Module For ACC203 Conceptual Framework and Presentation of Financial StatementsDocument42 pagesModule For ACC203 Conceptual Framework and Presentation of Financial StatementsAron Rabino ManaloNo ratings yet

- CM1 Overview of AccountingDocument14 pagesCM1 Overview of AccountingMark GerwinNo ratings yet

- The Conceptual Framework of AccountingDocument34 pagesThe Conceptual Framework of AccountingSuzanne Paderna100% (1)

- Unit-1 Intoduction To AccountingDocument17 pagesUnit-1 Intoduction To AccountingManjula DeviNo ratings yet

- Introduction To Accounting & Accounting Concepts and Policies IDocument24 pagesIntroduction To Accounting & Accounting Concepts and Policies IDanishevNo ratings yet

- SAS#2-ACC104 With AnswerDocument5 pagesSAS#2-ACC104 With AnswerartificerrrrNo ratings yet

- Intro to Financial Accounting: Key ConceptsDocument22 pagesIntro to Financial Accounting: Key ConceptsBorhanNo ratings yet

- Topic Overview - Week 2Document23 pagesTopic Overview - Week 2Awike IiyambulaNo ratings yet

- Module 006 Week002-Finacct3 Review of The Accounting ProcessDocument4 pagesModule 006 Week002-Finacct3 Review of The Accounting Processman ibeNo ratings yet

- Ch04 SM Larson FAP16Document64 pagesCh04 SM Larson FAP16josjhNo ratings yet

- Unit 1Document32 pagesUnit 1Dibyansu KumarNo ratings yet

- CH2Document39 pagesCH2Saleh RaoufNo ratings yet

- PDF&Rendition 1Document25 pagesPDF&Rendition 1nitin jaulkarNo ratings yet

- FABM Q3 L2. SLeM - 2S - Q3 - W2 Accounting Concept & PrinciplesDocument16 pagesFABM Q3 L2. SLeM - 2S - Q3 - W2 Accounting Concept & PrinciplesSophia MagdaraogNo ratings yet

- ACC 101 - Module 4Document12 pagesACC 101 - Module 4Kyla Renz de LeonNo ratings yet

- Fin 1 Module Midterm CoverageDocument67 pagesFin 1 Module Midterm CoverageRomea NuevaNo ratings yet

- Principles of Accounting II: Activity Fund Accounting For Local School PersonnelDocument75 pagesPrinciples of Accounting II: Activity Fund Accounting For Local School PersonnelJiechlat Dak YangNo ratings yet

- Unit I Study GuideDocument5 pagesUnit I Study GuideVirginia TownzenNo ratings yet

- CHAPTER 1 Introduction To AccountingDocument12 pagesCHAPTER 1 Introduction To Accountingrosendophil7No ratings yet

- Course Material 1 Introduction To AccountingDocument15 pagesCourse Material 1 Introduction To AccountingEowyn DianaNo ratings yet

- Module 4 Packet: AE 111 - Financial Accounting & ReportingDocument28 pagesModule 4 Packet: AE 111 - Financial Accounting & ReportingHelloNo ratings yet

- Week 01 - 01 - Module 01 - Concepts and PrinciplesDocument11 pagesWeek 01 - 01 - Module 01 - Concepts and Principles지마리No ratings yet

- Financial Accounting IDocument193 pagesFinancial Accounting InikhilsarojazNo ratings yet

- 2 REVEIW OF FINANCIAL STATEMENTS PREPARATION (1)Document5 pages2 REVEIW OF FINANCIAL STATEMENTS PREPARATION (1)Hommer CorderoNo ratings yet

- Analyze Financial Statements with Ratios and StatementsDocument64 pagesAnalyze Financial Statements with Ratios and StatementsHimanshu NaugainNo ratings yet

- MODULE 2 - BUSINESS ACCOUNTING RevisedDocument16 pagesMODULE 2 - BUSINESS ACCOUNTING RevisedArchill YapparconNo ratings yet

- Unit 1 - Accounting Cycle For A Service FirmDocument5 pagesUnit 1 - Accounting Cycle For A Service FirmJosh LeBlancNo ratings yet

- BEACTG 03 REVISED MODULE 2 Business Transaction & Acctg EquationDocument25 pagesBEACTG 03 REVISED MODULE 2 Business Transaction & Acctg EquationChristiandale Delos ReyesNo ratings yet

- Course Title: Intermediate Accounting Course Code: Acc2401Document7 pagesCourse Title: Intermediate Accounting Course Code: Acc2401S. M. Khaled HossainNo ratings yet

- Review of Related LiteratureDocument2 pagesReview of Related LiteratureJayvee BernalNo ratings yet

- History: Definition and UsageDocument4 pagesHistory: Definition and UsageJayvee BernalNo ratings yet

- Hiring: Review Application Schedule InterviewDocument3 pagesHiring: Review Application Schedule InterviewJayvee BernalNo ratings yet

- 5 - Relevant Costing and Differential AnalysisDocument41 pages5 - Relevant Costing and Differential AnalysisJayvee BernalNo ratings yet

- Course Material 7 - Accounting For Local Government UnitsDocument24 pagesCourse Material 7 - Accounting For Local Government UnitsJayvee BernalNo ratings yet

- Non-Profit OrganizationsDocument44 pagesNon-Profit OrganizationsJayvee BernalNo ratings yet

- 1.2 - Introduction To Management Accounting & Recent DevelopmentsDocument42 pages1.2 - Introduction To Management Accounting & Recent DevelopmentsJayvee BernalNo ratings yet

- Course Material 2 - The Unified Accounts Codes StructureDocument34 pagesCourse Material 2 - The Unified Accounts Codes StructureJayvee BernalNo ratings yet

- Partnership Liquidation - Activity - BERNAL J.V.BDocument3 pagesPartnership Liquidation - Activity - BERNAL J.V.BJayvee BernalNo ratings yet

- Course Material 3 - Accounting For Budgetary AccountsDocument22 pagesCourse Material 3 - Accounting For Budgetary AccountsJayvee BernalNo ratings yet

- Course Material 5 - Account For Revenue and Other ReceiptsDocument17 pagesCourse Material 5 - Account For Revenue and Other ReceiptsJayvee BernalNo ratings yet

- Course Material 4 - Accounting For Disbursement and Related TransactionsDocument32 pagesCourse Material 4 - Accounting For Disbursement and Related TransactionsJayvee BernalNo ratings yet

- Inventory Management and Control SystemDocument88 pagesInventory Management and Control SystemJayvee BernalNo ratings yet

- Opman-Practice Set On Network Diagram - Bernal J.V.BDocument2 pagesOpman-Practice Set On Network Diagram - Bernal J.V.BJayvee BernalNo ratings yet

- Introduction To Transaction Processing - Exercise - BERNAL J.V.BDocument2 pagesIntroduction To Transaction Processing - Exercise - BERNAL J.V.BJayvee BernalNo ratings yet

- Ias 18 PDFDocument4 pagesIas 18 PDFUmar Shaheen ANo ratings yet

- Mother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Document3 pagesMother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Jayash Kaushal0% (2)

- Finance RatiosDocument2 pagesFinance Ratioscoolmaverick420100% (1)

- Cash and Cash Equivalents DefinitionDocument10 pagesCash and Cash Equivalents DefinitionRica Lei N. DomingoNo ratings yet

- Oberoi Realty Initiation ReportDocument16 pagesOberoi Realty Initiation ReportHardik GandhiNo ratings yet

- Definition of CommitmentDocument2 pagesDefinition of CommitmentcrissiekamNo ratings yet

- PT Sawit Sumbermas Sarana TBK.: (Million Rupia ### ### ### Total AssetsDocument2 pagesPT Sawit Sumbermas Sarana TBK.: (Million Rupia ### ### ### Total AssetsAgil MahendraNo ratings yet

- Business Plan TemplateDocument33 pagesBusiness Plan TemplateMohammad Akbar MubaroqNo ratings yet

- 2006 Annual ReportDocument16 pages2006 Annual ReportEva's InitiativesNo ratings yet

- BBS - 1st - Financial Accounting and AnalysisDocument46 pagesBBS - 1st - Financial Accounting and AnalysisJALDIMAINo ratings yet

- CH 20Document8 pagesCH 20Saleh RaoufNo ratings yet

- Balane SheetDocument33 pagesBalane SheetOswinda GomesNo ratings yet

- Supply of Goods and ServicesDocument10 pagesSupply of Goods and Serviceshariom bajpaiNo ratings yet

- Power User Training Sign-Off Sheet Financial Accounting: 15 June 2010 - 23 JUNE 2010Document5 pagesPower User Training Sign-Off Sheet Financial Accounting: 15 June 2010 - 23 JUNE 2010Omer Farooq KhanNo ratings yet

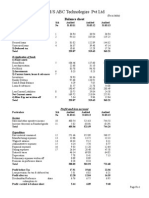

- ABC Technologies Balance Sheet AnalysisDocument3 pagesABC Technologies Balance Sheet AnalysisSmitha RajNo ratings yet

- Chapter 26 - Review QuestionsDocument7 pagesChapter 26 - Review QuestionsAli MohamedNo ratings yet

- CISDR 2007-08 Annual ReportDocument24 pagesCISDR 2007-08 Annual ReportCISDRNo ratings yet

- Acct 101 SyllabusDocument8 pagesAcct 101 Syllabusapi-267728422No ratings yet

- Notes Forming Part of Financial StatementsDocument36 pagesNotes Forming Part of Financial StatementsSwarup RanjanNo ratings yet

- Solution Accounting 2Document3 pagesSolution Accounting 2Hanzo vargasNo ratings yet