You might also like

- Amalgamation of Companies (AS 14)Document22 pagesAmalgamation of Companies (AS 14)Sanaullah M SultanpurNo ratings yet

- (CBCS) (Repeaters) Commerce Paper - 3.5: Accounting For Specialised InstitutionsDocument4 pages(CBCS) (Repeaters) Commerce Paper - 3.5: Accounting For Specialised InstitutionsSanaullah M SultanpurNo ratings yet

- Commerce (Regular) (Cost Accounting Group) Production and Operations Management Paper - 3.3 (B)Document4 pagesCommerce (Regular) (Cost Accounting Group) Production and Operations Management Paper - 3.3 (B)Sanaullah M SultanpurNo ratings yet

- Com203 - Final Accounts of Insurance CompaniesDocument23 pagesCom203 - Final Accounts of Insurance CompaniesSanaullah M SultanpurNo ratings yet

- Commerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Document4 pagesCommerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Sanaullah M SultanpurNo ratings yet

- Image 1646906033506Document4 pagesImage 1646906033506Sanaullah M SultanpurNo ratings yet

- (CBCS) Commerce Paper: 4.5 A - Innovations in Accounting: Note: Answer As Per Internal ChoiceDocument4 pages(CBCS) Commerce Paper: 4.5 A - Innovations in Accounting: Note: Answer As Per Internal ChoiceSanaullah M SultanpurNo ratings yet

- 02 SynopsisDocument44 pages02 SynopsisSanaullah M SultanpurNo ratings yet

- Commerce Paper 4.4 (A) Security Analysis and Portfolio Management Accounting and FinanceDocument3 pagesCommerce Paper 4.4 (A) Security Analysis and Portfolio Management Accounting and FinanceSanaullah M SultanpurNo ratings yet

- (CBCS) Commerce Paper - 4.4 (A) : Security Analysis and Portfolio ManagementDocument3 pages(CBCS) Commerce Paper - 4.4 (A) : Security Analysis and Portfolio ManagementSanaullah M SultanpurNo ratings yet

- Investors' Services FundDocument2 pagesInvestors' Services FundSanaullah M SultanpurNo ratings yet

- Commerce Innovations in Accounting Paper 4.5 A: (Accounting and Finance)Document3 pagesCommerce Innovations in Accounting Paper 4.5 A: (Accounting and Finance)Sanaullah M SultanpurNo ratings yet

- Commerce Paper 4.6 A - Mutual Funds (Accounting and Finance)Document3 pagesCommerce Paper 4.6 A - Mutual Funds (Accounting and Finance)Sanaullah M SultanpurNo ratings yet

- (CBCS) (Regular) Commerce Paper - 4.5: Innovations in AccountingDocument4 pages(CBCS) (Regular) Commerce Paper - 4.5: Innovations in AccountingSanaullah M SultanpurNo ratings yet

- (CBCS) Commerce Paper - 4.6 (A) : Mutual FundsDocument2 pages(CBCS) Commerce Paper - 4.6 (A) : Mutual FundsSanaullah M SultanpurNo ratings yet

- Human Resource Accounting Practices in Indian Companies: Bottorof$ ( - Tlosiop P CommerceDocument305 pagesHuman Resource Accounting Practices in Indian Companies: Bottorof$ ( - Tlosiop P CommerceSanaullah M SultanpurNo ratings yet

- 2021 0 Time Table - PG Golden Chance ExaminationDocument87 pages2021 0 Time Table - PG Golden Chance ExaminationSanaullah M SultanpurNo ratings yet

- Online/Digital Learning Questionnaire: October 2020Document5 pagesOnline/Digital Learning Questionnaire: October 2020Sanaullah M SultanpurNo ratings yet

- Environment of International Business and Its Significance: Dr. Akram Abdulraqeb Sultan Al-KhaledDocument7 pagesEnvironment of International Business and Its Significance: Dr. Akram Abdulraqeb Sultan Al-KhaledSanaullah M SultanpurNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- (Nikolay TSD) LCBB4001 Accounting Fundamentals-A1Document24 pages(Nikolay TSD) LCBB4001 Accounting Fundamentals-A1munnaNo ratings yet

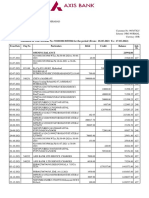

- Online StatementDocument3 pagesOnline StatementLong LeeNo ratings yet

- Chapter 1: Introduction To Accounting: Activity 1: A Chapter DiscussionDocument9 pagesChapter 1: Introduction To Accounting: Activity 1: A Chapter DiscussionFaith ClaireNo ratings yet

- Beauty Without Cruelty - India: Be Part of Our Movement and Donate NowDocument2 pagesBeauty Without Cruelty - India: Be Part of Our Movement and Donate NowdpfsopfopsfhopNo ratings yet

- Ifrs 17 Reinsurance Contract Held ExampleDocument24 pagesIfrs 17 Reinsurance Contract Held ExampleHesham AlabaniNo ratings yet

- Stripe Tax Invoice 3H6ZFA4U-2021-07Document1 pageStripe Tax Invoice 3H6ZFA4U-2021-07Rafa CNo ratings yet

- Answers BSBFIM501Document13 pagesAnswers BSBFIM501Gurpreet Kaur80% (5)

- Interest Rate Risk NotesDocument157 pagesInterest Rate Risk Notesdaksh.agarwal180No ratings yet

- Research Paper Group 3 1Document5 pagesResearch Paper Group 3 1Jp CombisNo ratings yet

- Factsheet ANTM 2023 01Document4 pagesFactsheet ANTM 2023 01arsyil1453No ratings yet

- FX Forecast Update 190623Document20 pagesFX Forecast Update 190623Ahmed AbedNo ratings yet

- The Balance Sheet Items For CIBDocument1 pageThe Balance Sheet Items For CIBKhalid Al SanabaniNo ratings yet

- MEcon - Presentation - MihailDocument13 pagesMEcon - Presentation - MihailMisho IlievNo ratings yet

- Worksheet 8 - Comparing QuantitiesDocument5 pagesWorksheet 8 - Comparing QuantitiesRosy RaiNo ratings yet

- John Maynard Keynes The General Theory of Employment Interest and Money A Critique by Brett DiDonatoDocument23 pagesJohn Maynard Keynes The General Theory of Employment Interest and Money A Critique by Brett DiDonatosoyouthinkyoucaninvest100% (1)

- The Currency Famine of 1893, John DeWitt WarnerDocument12 pagesThe Currency Famine of 1893, John DeWitt Warnervanveen1967No ratings yet

- Test Paper-2 Master Question PGBPDocument3 pagesTest Paper-2 Master Question PGBPyeidaindschemeNo ratings yet

- SWGI Growth Fund - 2009 Annual ReportDocument51 pagesSWGI Growth Fund - 2009 Annual ReportThe Russia MonitorNo ratings yet

- Risk Management Solution Chapters Seven-EightDocument9 pagesRisk Management Solution Chapters Seven-EightBombitaNo ratings yet

- Interest Rate DerivativesDocument58 pagesInterest Rate DerivativesIndia Forex100% (2)

- JP Morgan PresentationDocument22 pagesJP Morgan PresentationramleaderNo ratings yet

- Account STMTDocument4 pagesAccount STMTsreehas sreehasNo ratings yet

- Accounting Practice of Ethiopia - FinalDocument33 pagesAccounting Practice of Ethiopia - FinalDgl100% (8)

- LS Sar Page50Document1 pageLS Sar Page50Ljubisa MaticNo ratings yet

- Cash Flow Statement - Analyzing Cash Flow From Investing Activities - InvestopediaDocument3 pagesCash Flow Statement - Analyzing Cash Flow From Investing Activities - InvestopediaBob KaneNo ratings yet

- NSCC Fee Guide 2014Document26 pagesNSCC Fee Guide 2014theoriqueNo ratings yet

- PNB v. Natl City Bank of NYDocument19 pagesPNB v. Natl City Bank of NYAndrea RioNo ratings yet

- Tax Invoice: Madimack Pty LTD 19 Tarra Cres Dee Why NSW 2099Document1 pageTax Invoice: Madimack Pty LTD 19 Tarra Cres Dee Why NSW 2099Mildred PagsNo ratings yet

- Financial Supervisory System in Korea: RYU, Min Hae HWANG, Jae HakDocument43 pagesFinancial Supervisory System in Korea: RYU, Min Hae HWANG, Jae HakstaimoukNo ratings yet

- Financial Accounting Assignment 1 PDFDocument26 pagesFinancial Accounting Assignment 1 PDFUmair MughalNo ratings yet