You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Scientific Advertising - Book ReviewDocument6 pagesScientific Advertising - Book Reviewrainbowz2250% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Investment in Debt SecuritiesDocument31 pagesInvestment in Debt SecuritiesJohn Francis Idanan100% (1)

- 12 Top Five Regrets of The DyingDocument2 pages12 Top Five Regrets of The DyingOvini De SilvaNo ratings yet

- Valuation in The Airline Industry Excel FileDocument12 pagesValuation in The Airline Industry Excel FilevivekNo ratings yet

- History of RAF Squadron 145Document21 pagesHistory of RAF Squadron 145aalzayani100% (2)

- Accounting For InvestmentsDocument42 pagesAccounting For InvestmentsJohn Francis Idanan100% (4)

- TLM When To Sit & StandDocument1 pageTLM When To Sit & Standluthien tasadurNo ratings yet

- Fabric Study - (Textbook + Practical Manual) XIIDocument90 pagesFabric Study - (Textbook + Practical Manual) XIIAn Bn50% (2)

- Accounting For PpeDocument37 pagesAccounting For PpeJohn Francis Idanan40% (5)

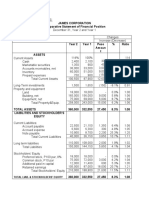

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDocument7 pagesHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananNo ratings yet

- Accounting For Service BusinessDocument2 pagesAccounting For Service BusinessJohn Francis IdananNo ratings yet

- 8-Capital BudgetingDocument89 pages8-Capital BudgetingJohn Francis IdananNo ratings yet

- DEPRECIATIONDocument10 pagesDEPRECIATIONJohn Francis IdananNo ratings yet

- Time Value of MoneyDocument5 pagesTime Value of MoneyJohn Francis IdananNo ratings yet

- Substantive Test of LiabilitiesDocument4 pagesSubstantive Test of LiabilitiesJohn Francis IdananNo ratings yet

- Springfield Building Department Inspectional Services Notice of ViolationsDocument6 pagesSpringfield Building Department Inspectional Services Notice of ViolationsThe Republican/MassLive.comNo ratings yet

- Gold Pre-First Exit Test: Name - ClassDocument7 pagesGold Pre-First Exit Test: Name - ClassMaría Marta OttavianoNo ratings yet

- Smelter and Refiner List in Samsungs Supply Chain 2022Document13 pagesSmelter and Refiner List in Samsungs Supply Chain 2022pepe romeroNo ratings yet

- Q1. Explain The Need For Corporate Governance. Discuss Its Role and Importance in Improving The Performance of Corporate SectorDocument3 pagesQ1. Explain The Need For Corporate Governance. Discuss Its Role and Importance in Improving The Performance of Corporate SectorAkash KumarNo ratings yet

- Ministry of Environment - VacanciesDocument1 pageMinistry of Environment - VacanciesRicardo DomingosNo ratings yet

- After BrexitDocument7 pagesAfter Brexityosmeilys.ramirezNo ratings yet

- ECHS ApplicationDocument77 pagesECHS ApplicationJAGDISH SAININo ratings yet

- Jaisalm Er: The Golden CityDocument29 pagesJaisalm Er: The Golden CityDeepak VermaNo ratings yet

- Memo Article FpcciDocument25 pagesMemo Article FpccimaliksaghirNo ratings yet

- UntitledDocument44 pagesUntitledAfnainNo ratings yet

- Reflection Essay 1Document3 pagesReflection Essay 1maria blascosNo ratings yet

- Addition KateDocument4 pagesAddition Kateaprrove ninjaNo ratings yet

- Armory v. DelamirieDocument1 pageArmory v. DelamiriePerez_Subgerente01No ratings yet

- Studentwise Final Placement DetailsLast 3 YearsDocument18 pagesStudentwise Final Placement DetailsLast 3 YearsAmitNo ratings yet

- Begining of A New Era Unit-IiDocument14 pagesBegining of A New Era Unit-IiANJU ASHOKANNo ratings yet

- Ana Pagano Health in Black and WhiteDocument24 pagesAna Pagano Health in Black and WhiteTarcisia EmanuelaNo ratings yet

- Synergy Synergy: Trading Method Trading MethodDocument22 pagesSynergy Synergy: Trading Method Trading MethodRabiu Ahmed OluwasegunNo ratings yet

- A.M. 1693 The Reformed GentlemanDocument93 pagesA.M. 1693 The Reformed GentlemanMitchell JohnsonNo ratings yet

- Creation of Israel, 1948 - Milestones - 1945-1952 - Milestones in The History ofDocument2 pagesCreation of Israel, 1948 - Milestones - 1945-1952 - Milestones in The History ofAhsanaliNo ratings yet

- Set Exam Question PaperDocument24 pagesSet Exam Question PaperMohammad Junaid KaziNo ratings yet

- Op Ed Genre WorksheetDocument2 pagesOp Ed Genre Worksheetapi-532133127No ratings yet

- A.C. No. 10537 - Ramirez vs. Atty. MargalloDocument6 pagesA.C. No. 10537 - Ramirez vs. Atty. MargalloDennis Jay A. ParasNo ratings yet

- Lower Swatara Township Code of OrdinancesDocument37 pagesLower Swatara Township Code of OrdinancesPress And JournalNo ratings yet

- Arjuna Prime FinalDocument27 pagesArjuna Prime FinalTejaswi SaxenaNo ratings yet