You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Abutment A & BDocument1 pageAbutment A & Bmr. oneNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Incident Report Starbucks Wall NewDocument4 pagesIncident Report Starbucks Wall Newmr. oneNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- AsdfdsfgfDocument1 pageAsdfdsfgfmr. oneNo ratings yet

- Base Plate / Anchorage Design: ASDIP Steel 5.0.5Document3 pagesBase Plate / Anchorage Design: ASDIP Steel 5.0.5mr. oneNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Chef Monica's ContractDocument12 pagesChef Monica's Contractmr. oneNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Circular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012Document1 pageCircular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012mr. oneNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- SdadfdsfaDocument1 pageSdadfdsfamr. oneNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Top of Deck SlabDocument1 pageTop of Deck Slabmr. oneNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Circular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012Document1 pageCircular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012mr. oneNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Combined Footing Design: ASDIP Foundation 4.4.2Document4 pagesCombined Footing Design: ASDIP Foundation 4.4.2mr. oneNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Circular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012Document1 pageCircular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012mr. oneNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Rep Strike Revilla - Roll-Over Internet Bill - With EsigDocument5 pagesRep Strike Revilla - Roll-Over Internet Bill - With Esigmr. oneNo ratings yet

- Circular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012Document1 pageCircular Column Axial Load Enhancement: Code: NCHRP/ Aashto LRFD 2012mr. oneNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- SdasaDocument1 pageSdasamr. oneNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- FGHFDocument1 pageFGHFmr. oneNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- SdasfdfaDocument1 pageSdasfdfamr. oneNo ratings yet

- PS No. 18Document1 pagePS No. 18mr. oneNo ratings yet

- Office of Congressman Strike B. RevillaDocument1 pageOffice of Congressman Strike B. Revillamr. oneNo ratings yet

- Trust 1 Ramos vs. RamosDocument3 pagesTrust 1 Ramos vs. Ramosmr. oneNo ratings yet

- Spread Footing Design: ASDIP Foundation 4.4.2Document4 pagesSpread Footing Design: ASDIP Foundation 4.4.2heherson juanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Committee On Local Government: Prepared by LUJDocument6 pagesCommittee On Local Government: Prepared by LUJmr. oneNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Rep Strike Revilla - Roll-Over Internet Bill - With EsigDocument5 pagesRep Strike Revilla - Roll-Over Internet Bill - With Esigmr. oneNo ratings yet

- 2nd Quarter ScienceDocument1 page2nd Quarter Sciencemr. oneNo ratings yet

- SdasdasdDocument1 pageSdasdasdmr. oneNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Rep Strike Revilla - E-Sports Bill - FinalDocument5 pagesRep Strike Revilla - E-Sports Bill - Finalmr. oneNo ratings yet

- Briefer - 17 March 2021 - HealthDocument5 pagesBriefer - 17 March 2021 - Healthmr. oneNo ratings yet

- Briefer - 15 Sept 2020 - CHTEDocument6 pagesBriefer - 15 Sept 2020 - CHTEmr. oneNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Briefer - 15 March 2021 - Subcommittee On Police AdminDocument7 pagesBriefer - 15 March 2021 - Subcommittee On Police Adminmr. oneNo ratings yet

- Rep Strike Revilla - E-Sports BillDocument4 pagesRep Strike Revilla - E-Sports Billmr. oneNo ratings yet

- Fixed Asset Depreciation CalculationDocument2 pagesFixed Asset Depreciation CalculationMirna Kassar0% (1)

- Tax Invoice: FromDocument1 pageTax Invoice: FromMohit Ruhani MehraNo ratings yet

- BUKIDNON STATE UNIVERSITY EVALUATION TEST COVERS PRINCIPLES OF TAXATIONDocument17 pagesBUKIDNON STATE UNIVERSITY EVALUATION TEST COVERS PRINCIPLES OF TAXATIONJames Bryle GalagnaraNo ratings yet

- LESCO - Web Bill-February 2023Document2 pagesLESCO - Web Bill-February 2023MudassirNo ratings yet

- Tax Breaks To EliminateDocument4 pagesTax Breaks To Eliminatedacoda204No ratings yet

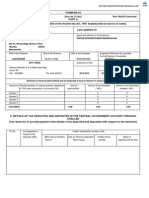

- Form 16 by Tcs PDFDocument5 pagesForm 16 by Tcs PDFAnonymous utPqL6jA3i25% (4)

- Would Flat Tax Work Again in Albania?Document4 pagesWould Flat Tax Work Again in Albania?Eduart GjokutajNo ratings yet

- PCL Chap 4 en CaDocument70 pagesPCL Chap 4 en CaRenso Ramirez100% (1)

- Chapter04.Personal ClaimsDocument181 pagesChapter04.Personal Claimsmpradip1975No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fort Bonifacio Development Corp. vs. Commissioner of Internal Revenue, 679 SCRA 566, September 04, 2012Document3 pagesFort Bonifacio Development Corp. vs. Commissioner of Internal Revenue, 679 SCRA 566, September 04, 2012anajuanitoNo ratings yet

- IRS TaxCodeDocument5 pagesIRS TaxCodeMt EmptyNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToShankara NarayananNo ratings yet

- Cir Vs CitytrustDocument2 pagesCir Vs CitytrustNelle Bulos-VenusNo ratings yet

- Connecticut W-4 Form Explains Codes For Withholding RatesDocument4 pagesConnecticut W-4 Form Explains Codes For Withholding RatesestannardNo ratings yet

- Stamp Duty Ready RecknorDocument14 pagesStamp Duty Ready RecknorLamar MillerNo ratings yet

- Understanding Economic Survey and Union BudgetDocument2 pagesUnderstanding Economic Survey and Union BudgetVarsha GuptaNo ratings yet

- Vista Print TaxInvoiceDocument2 pagesVista Print TaxInvoicebhageshlNo ratings yet

- Pay Slip March 2018Document1 pagePay Slip March 2018Anil PuvadaNo ratings yet

- PWC Vietnam Pocket Tax Book 2013Document43 pagesPWC Vietnam Pocket Tax Book 2013Angie NguyenNo ratings yet

- Scan COI for employment insurance detailsDocument2 pagesScan COI for employment insurance detailsAvijit DebnathNo ratings yet

- Midterm Exam - Ac-2Document7 pagesMidterm Exam - Ac-2Lyca ArcenaNo ratings yet

- TAX INVOICE DETAILSDocument1 pageTAX INVOICE DETAILSJNPNo ratings yet

- 2014 - CE (N.T.), Dated 12-08-2014Document1 page2014 - CE (N.T.), Dated 12-08-2014శ్రీనివాసకిరణ్కుమార్చతుర్వేదులNo ratings yet

- KPMG Flash News Valuation of Unquoted Shares 2Document3 pagesKPMG Flash News Valuation of Unquoted Shares 2Sridhar KrishnaNo ratings yet

- INSULAR LUMBER COMPANY vs. COURT OF TAX APPEALSDocument2 pagesINSULAR LUMBER COMPANY vs. COURT OF TAX APPEALSSwitzel SambriaNo ratings yet

- 4.2 Assignment - Principles To Accounting Period and MethodsDocument7 pages4.2 Assignment - Principles To Accounting Period and MethodsRoselyn LumbaoNo ratings yet

- ErrorDocument6 pagesErroranggandakonoh0% (1)

- Sales Invoice SummaryDocument1 pageSales Invoice SummaryRaghavendra S DNo ratings yet

- Philippines Supreme Court rules on tax deduction for US citizensDocument92 pagesPhilippines Supreme Court rules on tax deduction for US citizens001nooneNo ratings yet

- UntitledDocument15 pagesUntitledDharel GannabanNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)