You might also like

- Unit VDocument18 pagesUnit VDr.P. Siva RamakrishnaNo ratings yet

- Profit: Types, Theories and Functions of ProfitDocument9 pagesProfit: Types, Theories and Functions of ProfitpreethilmaNo ratings yet

- Theories of ProfitDocument8 pagesTheories of ProfitNikita NimbalkarNo ratings yet

- Unit 5Document16 pagesUnit 5mussaiyibNo ratings yet

- Theories of ProfitDocument23 pagesTheories of ProfitswaroopramNo ratings yet

- Top 8 Theories of ProfitDocument7 pagesTop 8 Theories of Profitrhena villapasNo ratings yet

- Profits and Risk and Uncertainty Theory of Profit Learning Objective: Concepts of Profit and Theory of ProfitDocument3 pagesProfits and Risk and Uncertainty Theory of Profit Learning Objective: Concepts of Profit and Theory of ProfitRohitPatialNo ratings yet

- Unit 2 Theories of EntrepreneurshipDocument8 pagesUnit 2 Theories of EntrepreneurshipanishaNo ratings yet

- MBA-1 Risk Bearing Theory - F by AnjaliDocument4 pagesMBA-1 Risk Bearing Theory - F by AnjaliHritika SinghNo ratings yet

- Different Theories of ProfitDocument2 pagesDifferent Theories of Profitchandu_jjvrp0% (1)

- Economics ImpDocument9 pagesEconomics ImpTushti MalhotraNo ratings yet

- Profit ManagementDocument6 pagesProfit ManagementSonia LawsonNo ratings yet

- Theory of ProfitDocument10 pagesTheory of ProfitKajal Patil100% (1)

- Profit TheoriesDocument9 pagesProfit TheoriesRishwanth SNo ratings yet

- Objectives of Business Firm-FinalDocument43 pagesObjectives of Business Firm-FinalId Mohammad100% (3)

- DEFINITION of 'Business Risk'Document5 pagesDEFINITION of 'Business Risk'Rahul MaheshwariNo ratings yet

- Risk Dollarisation®: REDUCED DAMAGE CO$T$ = 1NCREA$ED PROF1T$From EverandRisk Dollarisation®: REDUCED DAMAGE CO$T$ = 1NCREA$ED PROF1T$No ratings yet

- Nature and Function of Profit: Dr. Gopalakrishna B.VDocument21 pagesNature and Function of Profit: Dr. Gopalakrishna B.VsamrulezzzNo ratings yet

- Theories of ProfitDocument5 pagesTheories of ProfitKavyanjali SinghNo ratings yet

- Chapter 2 Risk ManagementDocument20 pagesChapter 2 Risk ManagementbikilahussenNo ratings yet

- Theories of ProfitDocument39 pagesTheories of Profitradhaindia100% (1)

- Managerial Economics in Unit 5 Profit by - DR - Neha MathurDocument9 pagesManagerial Economics in Unit 5 Profit by - DR - Neha MathurGauravNo ratings yet

- Charlote Rep. FINANCIAL RISK MANAGEMENTDocument18 pagesCharlote Rep. FINANCIAL RISK MANAGEMENTJeanette FormenteraNo ratings yet

- Chapter Six: Risk Management in Business EnterprisesDocument22 pagesChapter Six: Risk Management in Business EnterprisesGech MNo ratings yet

- ENV Assignment InternalsDocument7 pagesENV Assignment Internalsakashsharma9011328268No ratings yet

- Theories of ProfitDocument6 pagesTheories of Profitvinati100% (1)

- Lesson Note EightDocument6 pagesLesson Note Eightanatomy grandgerNo ratings yet

- INTRODUCTION TO PROFIT MANAGEMENT M.E. NotesDocument25 pagesINTRODUCTION TO PROFIT MANAGEMENT M.E. NotesRita Alexa100% (3)

- Economics Notes Nec CH - 6 StuDocument7 pagesEconomics Notes Nec CH - 6 StuBirendra ShresthaNo ratings yet

- Basic Concepts of Managerial EconomicsDocument6 pagesBasic Concepts of Managerial EconomicsAnika VarkeyNo ratings yet

- ME - Objectives of Business Firms - 10Document29 pagesME - Objectives of Business Firms - 10semerederibe100% (1)

- Definition of BusinessDocument42 pagesDefinition of BusinessSujata BhosaleNo ratings yet

- Entrepreneurship DevDocument29 pagesEntrepreneurship DevtanyaNo ratings yet

- Profit Maximization and Wealth MaximizationDocument4 pagesProfit Maximization and Wealth MaximizationUvasre Sundar100% (3)

- Unit 2 Innovation & Entrepreneurship KMBN302Document28 pagesUnit 2 Innovation & Entrepreneurship KMBN302Prerna JhaNo ratings yet

- Material No. 5Document5 pagesMaterial No. 5rhbqztqbzyNo ratings yet

- Entrepreneurial Development Write UpDocument67 pagesEntrepreneurial Development Write UpJoyful DaysNo ratings yet

- MEFA UNIT-I Part-2Document9 pagesMEFA UNIT-I Part-2Anusha EnigallaNo ratings yet

- Entrepre N NotesDocument100 pagesEntrepre N NotesJOSIANENo ratings yet

- BEFA Mid-1 AnswersDocument36 pagesBEFA Mid-1 Answersravi tejaNo ratings yet

- MEFA UNIT-I Part-3Document9 pagesMEFA UNIT-I Part-3neha yarrapothuNo ratings yet

- Risk Management Lesson 1Document8 pagesRisk Management Lesson 1ABIODUN MicahNo ratings yet

- Introduction To EntrepreneurshipDocument20 pagesIntroduction To EntrepreneurshipNoah Ras LobitañaNo ratings yet

- FM Notes - Unit - 1Document17 pagesFM Notes - Unit - 1Shiva JohriNo ratings yet

- Unit - I: Managerial EconomicsDocument66 pagesUnit - I: Managerial EconomicsAkashNo ratings yet

- SESSION 3qDocument13 pagesSESSION 3qstumaini1200usdNo ratings yet

- Powerpoint in Entrep 1-3Document376 pagesPowerpoint in Entrep 1-3Joeferson Baguio Dancel100% (4)

- Unit 4 Operational Risk OverviewDocument29 pagesUnit 4 Operational Risk Overviewsaurabh thakurNo ratings yet

- SynopsisDocument3 pagesSynopsisRehaan DanishNo ratings yet

- (Q) - Discuss May Two Theories of Profit.Document3 pages(Q) - Discuss May Two Theories of Profit.Naved SahabNo ratings yet

- Objectives of Financial ManagementDocument3 pagesObjectives of Financial ManagementDaniel IssacNo ratings yet

- Theories of ProfitsDocument4 pagesTheories of ProfitsShaik Khwaja Nawaz SharifNo ratings yet

- EntrepreneurshipDocument94 pagesEntrepreneurshipSunny Dahiya100% (1)

- Module 1 QABDocument12 pagesModule 1 QABVaibhav LokegaonkarNo ratings yet

- 10 Principles of FinanceDocument6 pages10 Principles of FinanceMary Joy Caro CastañosNo ratings yet

- Nombrado, Sean Lester CBET - 01 - 303A Review Questions Concept Review Questions Test QuestionsDocument5 pagesNombrado, Sean Lester CBET - 01 - 303A Review Questions Concept Review Questions Test QuestionsSean Lester S. NombradoNo ratings yet

- 1711-316009 - Rehan AhmadDocument13 pages1711-316009 - Rehan AhmadMalik Muhammad NadirNo ratings yet

- Summary CH 1Document4 pagesSummary CH 1zulu4smawanNo ratings yet

- An Era of Pandemic - Business Survival During Pandemic and Its AftermathFrom EverandAn Era of Pandemic - Business Survival During Pandemic and Its AftermathNo ratings yet

- Motivation, Performance and Efficiency: November 2016Document4 pagesMotivation, Performance and Efficiency: November 2016Irina AtudoreiNo ratings yet

- Factors Affecting Employees MotivationDocument9 pagesFactors Affecting Employees Motivationm p100% (1)

- Factors Affecting Employees MotivationDocument9 pagesFactors Affecting Employees Motivationm p100% (1)

- Motivational Theories - A Critical Analysis: June 2014Document9 pagesMotivational Theories - A Critical Analysis: June 2014jimmycia82No ratings yet

- Modul MotivasiDocument23 pagesModul MotivasiElka Adreena ArsyNo ratings yet

- IJCRT2105297Document8 pagesIJCRT2105297m pNo ratings yet

- EJ1191767Document37 pagesEJ1191767m pNo ratings yet

- Board Paper The Functions and Impact of Fiscal CouncilsDocument63 pagesBoard Paper The Functions and Impact of Fiscal Councilsm pNo ratings yet

- The Role of Con Ict Management in Improving Relationships at Work: The Moderating Effect of CommunicationDocument11 pagesThe Role of Con Ict Management in Improving Relationships at Work: The Moderating Effect of CommunicationJamie HaravataNo ratings yet

- Learning Processes and Processing Learning From orDocument13 pagesLearning Processes and Processing Learning From orm pNo ratings yet

- Dimensiunea Interculturala in Rezolvarea ConflicteDocument15 pagesDimensiunea Interculturala in Rezolvarea ConflicteAlina Andreea DinuNo ratings yet

- Board Paper The Functions and Impact of Fiscal CouncilsDocument63 pagesBoard Paper The Functions and Impact of Fiscal Councilsm pNo ratings yet

- Gender Differences in The Context of Psychological Defense Mechanisms - Romanian Version of DSQ 60Document101 pagesGender Differences in The Context of Psychological Defense Mechanisms - Romanian Version of DSQ 60m pNo ratings yet

- Dimensiunea Interculturala in Rezolvarea ConflicteDocument15 pagesDimensiunea Interculturala in Rezolvarea ConflicteAlina Andreea DinuNo ratings yet

- Defining Con Ict and Making Choices About Its Management: Lighting The Dark Side of Organizational LifeDocument10 pagesDefining Con Ict and Making Choices About Its Management: Lighting The Dark Side of Organizational Lifetataru ninaNo ratings yet

- Sanyal, Rajibkumar. (2019) - Profit Theory 1.Document7 pagesSanyal, Rajibkumar. (2019) - Profit Theory 1.m pNo ratings yet

- Profit Maximisation As An Objective of A Firm-A Robust PerspectiveDocument4 pagesProfit Maximisation As An Objective of A Firm-A Robust PerspectivePhương Ngô LanNo ratings yet

- Profit & Loss Account and Balance Sheet ObjectivesDocument18 pagesProfit & Loss Account and Balance Sheet Objectivesm pNo ratings yet

- Masterthesis RavshanbekIsmailovDocument106 pagesMasterthesis RavshanbekIsmailovm pNo ratings yet

- Juridical Regime of Fiscal Inspection in Romania: January 2010Document10 pagesJuridical Regime of Fiscal Inspection in Romania: January 2010m pNo ratings yet

- Juridical Regime of Fiscal Inspection in Romania: January 2010Document10 pagesJuridical Regime of Fiscal Inspection in Romania: January 2010m pNo ratings yet

- Profit Maximisation As An Objective of A Firm-A Robust PerspectiveDocument4 pagesProfit Maximisation As An Objective of A Firm-A Robust PerspectivePhương Ngô LanNo ratings yet

- Relatii Publice ASEDocument4 pagesRelatii Publice ASEm pNo ratings yet

- Profit Maximization and Wealth MaximizationDocument16 pagesProfit Maximization and Wealth MaximizationOnindya MitraNo ratings yet

- Plagiarism Detector LogDocument130 pagesPlagiarism Detector Logm pNo ratings yet

- Din 21/05/2019 Pop DanielDocument2 pagesDin 21/05/2019 Pop Danielm pNo ratings yet

- Snowball LicenseDocument1 pageSnowball LicenseMaria Canubis PuertaNo ratings yet

- Plagiarism Detector LogDocument130 pagesPlagiarism Detector Logm pNo ratings yet

- Boost LicenseDocument1 pageBoost LicensedroikenNo ratings yet

- Consumer Behaviour Swiggy ZomatoDocument11 pagesConsumer Behaviour Swiggy ZomatowhoreNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- Pip Calculator - Forex Pip Calculator - Pip Value CalculatorDocument1 pagePip Calculator - Forex Pip Calculator - Pip Value Calculatorl100% (1)

- Listening Test Unit 6Document2 pagesListening Test Unit 6Xuân Bách0% (1)

- It Landscape: InsideDocument89 pagesIt Landscape: InsideBogdan StanciuNo ratings yet

- Predatory Pricing: Group: 2 Section: BDocument27 pagesPredatory Pricing: Group: 2 Section: BEsheeta GhoshNo ratings yet

- RACIDocument26 pagesRACImailtonoorul4114No ratings yet

- G11 1ST SemDocument2 pagesG11 1ST SemKrichel Mikhaela CorroNo ratings yet

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. byDocument56 pagesSecuritisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. bykannangksNo ratings yet

- Accenture FY19 Case WorkbookDocument24 pagesAccenture FY19 Case WorkbookMeera DeviNo ratings yet

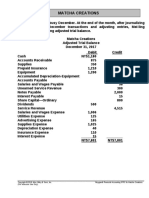

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Money Indian Currency Is Rupees and Paise. Let Us Look at Some Currency Notes and Coins That We UseDocument6 pagesMoney Indian Currency Is Rupees and Paise. Let Us Look at Some Currency Notes and Coins That We UseDhivya APNo ratings yet

- Economic Influences On Logistics - Business Case Study 2023Document3 pagesEconomic Influences On Logistics - Business Case Study 2023Bowie LeckieNo ratings yet

- Waste To WealthDocument13 pagesWaste To Wealthprashant singhNo ratings yet

- Business Interruption Insurance Notes-Final 2023Document12 pagesBusiness Interruption Insurance Notes-Final 2023tshililo mbengeniNo ratings yet

- CSE4003 - Cyber Security: Digital Assignment IDocument15 pagesCSE4003 - Cyber Security: Digital Assignment IjustadityabistNo ratings yet

- frdA190220A1421665 PDFDocument2 pagesfrdA190220A1421665 PDFVeritaserumNo ratings yet

- Characteristics of Habitual Entrepreneurs in Wales Awab Dali 09.09.2016 03.03.2020Document65 pagesCharacteristics of Habitual Entrepreneurs in Wales Awab Dali 09.09.2016 03.03.2020Awab DaliNo ratings yet

- Affiliated To University of Mumbai Program: COMMERCE Program Code: RJCUCOM (CBCS 2018-19)Document20 pagesAffiliated To University of Mumbai Program: COMMERCE Program Code: RJCUCOM (CBCS 2018-19)Endubai SuryawanshiNo ratings yet

- Press Release JFSL and Blackrock Agree To Form JVDocument3 pagesPress Release JFSL and Blackrock Agree To Form JVvikaskfeaindia15No ratings yet

- Personal Lease Adam LightfootDocument9 pagesPersonal Lease Adam Lightfootaaakinkumi115No ratings yet

- IHG® Frontline - GM Implementation Guide (Americas)Document20 pagesIHG® Frontline - GM Implementation Guide (Americas)Julie AnnaNo ratings yet

- Chapter 6 PRACTICING AS AN ETHICAL ADMINISTRATIONDocument8 pagesChapter 6 PRACTICING AS AN ETHICAL ADMINISTRATIONJR Rolf NeuqeletNo ratings yet

- LISTENING Countries in The WorldDocument6 pagesLISTENING Countries in The WorldVân KhánhNo ratings yet

- SM SX 52 SpecificatonDocument2 pagesSM SX 52 SpecificatonAli HussnainNo ratings yet

- Great To Have You On Board!Document36 pagesGreat To Have You On Board!jondraxdNo ratings yet

- Customer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedDocument25 pagesCustomer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedOmor FarukNo ratings yet

- GPOA (PR Consultant)Document7 pagesGPOA (PR Consultant)Jeydrew TVNo ratings yet

- Research Methods For Architecture Ebook - Lucas, Ray - Kindle StoreDocument1 pageResearch Methods For Architecture Ebook - Lucas, Ray - Kindle StoreMohammed ShriamNo ratings yet

- Introduction To Petroleum Engineering - Lecture 3 - 12-10-2012 - Final PDFDocument19 pagesIntroduction To Petroleum Engineering - Lecture 3 - 12-10-2012 - Final PDFshanecarlNo ratings yet