You might also like

- Formula Options Trading StrategiesDocument2 pagesFormula Options Trading StrategiesSameer88% (8)

- Five Low Risk Setups For Trading FuturesDocument76 pagesFive Low Risk Setups For Trading FuturesKenneth Culbert50% (2)

- Option Trading Strategies SummaryDocument6 pagesOption Trading Strategies SummaryRavi Khushalani100% (1)

- LIC Study Objectives and MethodologyDocument60 pagesLIC Study Objectives and MethodologypiudiNo ratings yet

- Risk Management Insurance - NotesDocument187 pagesRisk Management Insurance - NotesTejas100% (1)

- Elements of Good Life Insurance PolicyDocument4 pagesElements of Good Life Insurance PolicySaumya JaiswalNo ratings yet

- What is General Insurance in 40 CharactersDocument249 pagesWhat is General Insurance in 40 CharactersSandhya TambeNo ratings yet

- Insurance HandbookDocument28 pagesInsurance HandbookGreat VivekanandaNo ratings yet

- IC-85 Reinsurance PDFDocument342 pagesIC-85 Reinsurance PDFYesu Babu100% (1)

- Recruitment of Life Advisors in Indian Life Insurance IndustryDocument92 pagesRecruitment of Life Advisors in Indian Life Insurance IndustryDeepak Sharma100% (1)

- Data Pricing Edmund Lee PDFDocument41 pagesData Pricing Edmund Lee PDFAmit Bisai100% (1)

- Insurance management: Life, Motor, HealthDocument11 pagesInsurance management: Life, Motor, HealthHimanshu Conscript100% (1)

- SYBBI FP ProDocument9 pagesSYBBI FP ProSudarshan TakNo ratings yet

- IRM AssignmentDocument13 pagesIRM AssignmentHarshit Wardhan PrasadNo ratings yet

- Types of Insurance ExplainedDocument14 pagesTypes of Insurance ExplainedHS AspuipluNo ratings yet

- Insurance – Definition and Meaning 2Document4 pagesInsurance – Definition and Meaning 2ЕкатеринаNo ratings yet

- Life Insurance Kotak Mahindra Group Old MutualDocument16 pagesLife Insurance Kotak Mahindra Group Old MutualKanchan khedaskerNo ratings yet

- Classification of InsuranceDocument10 pagesClassification of InsuranceKhalid MehmoodNo ratings yet

- Research 1Document3 pagesResearch 1Rhythm MukatiNo ratings yet

- Insurance Promotion - IIDocument12 pagesInsurance Promotion - IIAditi JainNo ratings yet

- Subject: Risk & Insurance Management: Submitted By: Nitin Mahindroo Roll-No-617 Submitted To: Mr. Naresh SharmaDocument18 pagesSubject: Risk & Insurance Management: Submitted By: Nitin Mahindroo Roll-No-617 Submitted To: Mr. Naresh SharmaNitin MahindrooNo ratings yet

- New Microsoft Word DocumentDocument3 pagesNew Microsoft Word DocumentShantam GulatiNo ratings yet

- Everything You Need to Know About Life InsuranceDocument11 pagesEverything You Need to Know About Life InsurancePooja TripathiNo ratings yet

- Ibis Unit 03Document28 pagesIbis Unit 03bhagyashripande321No ratings yet

- Insurance PlansDocument2 pagesInsurance PlansDeeksha AgrawalNo ratings yet

- Importance of life and general insurance policiesDocument22 pagesImportance of life and general insurance policiesBhavik JainNo ratings yet

- 3-Financial Services - Non Banking Products-Part 2Document47 pages3-Financial Services - Non Banking Products-Part 2Kirti GiyamalaniNo ratings yet

- How Life Insurance Differ From OtherDocument2 pagesHow Life Insurance Differ From OtherishwarNo ratings yet

- Insurance ....Document8 pagesInsurance ....SanyaNo ratings yet

- Daniel AyoolaDocument10 pagesDaniel AyoolaSalim SulaimanNo ratings yet

- Group Insurance ExplainedDocument4 pagesGroup Insurance ExplainedBushra HaqueNo ratings yet

- Insurance basics explained in 40 charactersDocument5 pagesInsurance basics explained in 40 charactersDebasis NayakNo ratings yet

- What Is Insurance - Meaning, Types, Importance & BenefitsDocument7 pagesWhat Is Insurance - Meaning, Types, Importance & BenefitsAyush VermaNo ratings yet

- B&I Unit 5Document19 pagesB&I Unit 5saisri nagamallaNo ratings yet

- Basic Information About LIC PoliciesDocument6 pagesBasic Information About LIC PoliciesskumarshopperNo ratings yet

- Chap Iii - FinaldraftDocument12 pagesChap Iii - FinaldraftOjo Meow GovindhNo ratings yet

- Insurance PDFDocument16 pagesInsurance PDFNANDHINI MNo ratings yet

- InsuranceDocument7 pagesInsuranceVairag JainNo ratings yet

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- Q. What Is General Insurance and Explain Various Types of General Insurance?Document5 pagesQ. What Is General Insurance and Explain Various Types of General Insurance?Anil Bhard WajNo ratings yet

- Types of Insurance/Life Insurance/General InsuranceDocument3 pagesTypes of Insurance/Life Insurance/General Insuranceamarx2920000% (1)

- Insurance Company ProfileDocument12 pagesInsurance Company ProfileKai MK4No ratings yet

- Hum ADocument119 pagesHum Ajyoti8mishra100% (2)

- InsuranceDocument2 pagesInsurancesobhencNo ratings yet

- Group members and life insurance definitionsDocument20 pagesGroup members and life insurance definitionsMilton Rosario MoraesNo ratings yet

- Table & ContentDocument43 pagesTable & Contentsweety coolNo ratings yet

- Why Life Insurance Provides Financial SecurityDocument3 pagesWhy Life Insurance Provides Financial Securityshailen2uNo ratings yet

- Analysis of Indian Insurance IndustryDocument32 pagesAnalysis of Indian Insurance Industrymayur_rughaniNo ratings yet

- Need For Life InsuranceDocument9 pagesNeed For Life InsuranceDeepak NayakNo ratings yet

- Banking and InsuranceDocument17 pagesBanking and InsuranceDeepak GhimireNo ratings yet

- Presentation On InsuranceDocument40 pagesPresentation On InsurancedevvratNo ratings yet

- Unit - IiDocument9 pagesUnit - Iihitesh gargNo ratings yet

- NOTES (3)Document3 pagesNOTES (3)rgaherwal098No ratings yet

- Contractual Savng 1Document10 pagesContractual Savng 1Farid Kae KhamisNo ratings yet

- Unit Iii BoirmDocument58 pagesUnit Iii Boirmmtechvlsitd labNo ratings yet

- Principles & Types of InsuranceDocument6 pagesPrinciples & Types of InsuranceSudhansu Shekhar pandaNo ratings yet

- Life InsuranceDocument11 pagesLife InsuranceTuttu RajenDranNo ratings yet

- Finance PPT 2Document11 pagesFinance PPT 2sanhithNo ratings yet

- 6.FIM-Module VI - Insurance Companies and Pension FundDocument16 pages6.FIM-Module VI - Insurance Companies and Pension FundAmarendra PattnaikNo ratings yet

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- What Is Life Insurance in 40 CharactersDocument7 pagesWhat Is Life Insurance in 40 CharactersAustin MathiasNo ratings yet

- NotesDocument6 pagesNotesGoodataka ZackamanNo ratings yet

- Company Profile BirlaDocument31 pagesCompany Profile BirlaShivayu VaidNo ratings yet

- INSURANCE GUIDE COVERS LIFE GENERAL PLANSDocument16 pagesINSURANCE GUIDE COVERS LIFE GENERAL PLANSselvi abrahamNo ratings yet

- Motor Vehicle InsuranceDocument12 pagesMotor Vehicle InsuranceDhruv SiddarthNo ratings yet

- Insurance and Pension FundDocument44 pagesInsurance and Pension FundFiaz Ul HassanNo ratings yet

- Sps Antonio Tibay Vs CA GR 119655Document11 pagesSps Antonio Tibay Vs CA GR 119655VieNo ratings yet

- MalobaDocument1 pageMalobaenyonyoziNo ratings yet

- Risk Management: Credit, Weather, Energy, and Insurance Derivatives & Derivative MishapsDocument20 pagesRisk Management: Credit, Weather, Energy, and Insurance Derivatives & Derivative MishapsNishita SodagarNo ratings yet

- Q2021002 - ICAT - TC Insurance 40L - 3 PlatesDocument3 pagesQ2021002 - ICAT - TC Insurance 40L - 3 PlatesRatnadeep GhoshNo ratings yet

- Advanced: Derivatives Trading StrategiesDocument1 pageAdvanced: Derivatives Trading StrategiesSwapan ChakrabortyNo ratings yet

- Ejercicios de Bonos Con OpcionalidadDocument4 pagesEjercicios de Bonos Con OpcionalidadJosue Daniel Vilca ReynaldoNo ratings yet

- Assignment 2 - Weather DerivativeDocument8 pagesAssignment 2 - Weather DerivativeBrow SimonNo ratings yet

- Forward Bond Price Using Repo and FuturesDocument19 pagesForward Bond Price Using Repo and Futuressumit_uk1No ratings yet

- Balanced Scorecard - Auguis, Andrew SDocument1 pageBalanced Scorecard - Auguis, Andrew SICT DA13No ratings yet

- Tata AIA Life Insurance Sampoorna Raksha Supreme: Policy DetailsDocument4 pagesTata AIA Life Insurance Sampoorna Raksha Supreme: Policy DetailsRavi PrakashNo ratings yet

- Answers To Chapter 10 QuestionsDocument10 pagesAnswers To Chapter 10 QuestionsMoNo ratings yet

- Variable Universal Life - ExplanationDocument5 pagesVariable Universal Life - ExplanationGerald MesinaNo ratings yet

- Swaps: Derivatives & Risk ManagementDocument17 pagesSwaps: Derivatives & Risk ManagementMayankSharmaNo ratings yet

- Options I UploadDocument3 pagesOptions I UploadManav DhimanNo ratings yet

- PPC 1K485571204 2020-21 31122020Document1 pagePPC 1K485571204 2020-21 31122020communication indirapuramNo ratings yet

- Summary and Introduction To Real Options AnalysisDocument7 pagesSummary and Introduction To Real Options Analysisadminprojects1No ratings yet

- FINN 326 - Financial Risk Management-Bushra NaqviDocument5 pagesFINN 326 - Financial Risk Management-Bushra NaqviMuhammad Idrees0% (1)

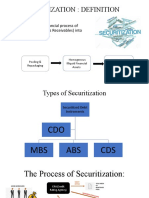

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- New Term: Hull and MachineryDocument8 pagesNew Term: Hull and MachineryJhoo AngelNo ratings yet

- Welcome To Aditya Birla Insurance Brokers Limited, A Subsidiary of Aditya Birla Capital Limited!Document4 pagesWelcome To Aditya Birla Insurance Brokers Limited, A Subsidiary of Aditya Birla Capital Limited!Loan LoanNo ratings yet

- The Pricing of Insurance PREMIUM CALCULATION INS 200Document12 pagesThe Pricing of Insurance PREMIUM CALCULATION INS 200Nur Syafatin Natasya100% (1)

- IndiaFirst Life Smart Pay Plan Money Back Life Insurance SummaryDocument2 pagesIndiaFirst Life Smart Pay Plan Money Back Life Insurance SummaryN-1397-10 KANISHKA Y HARDASANINo ratings yet

- Research Paper For Credit CrisisDocument31 pagesResearch Paper For Credit CrisisShabana KhanNo ratings yet