You might also like

- Week 4-7Document9 pagesWeek 4-7Vijayant DalalNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Residential Status Cma IndaDocument10 pagesResidential Status Cma IndaKiran ChristyNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document47 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Samata BohraNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- Model Answers Law of TaxationDocument46 pagesModel Answers Law of Taxationlavkush1234No ratings yet

- Law of Taxation Law of Taxation Class Notes CompressDocument48 pagesLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- TAX Planning AssigmentDocument11 pagesTAX Planning AssigmentKaba TidianeNo ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Weeks 4,5,6 - PDFDocument191 pagesWeeks 4,5,6 - PDFMehul Kumar MukulNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav Banjandeepika gawasNo ratings yet

- 1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee IsDocument14 pages1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee Isdhananjay7No ratings yet

- Corporate Tax Planning: Unit IDocument35 pagesCorporate Tax Planning: Unit ILavanya KasettyNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- 1518759148pdfjoiner PDFDocument40 pages1518759148pdfjoiner PDFAlkaNo ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav BanjanAnmolNo ratings yet

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Residential Status of A CompanyDocument18 pagesResidential Status of A CompanyNaveenNo ratings yet

- B71fedca 95fa 4b5b B32e A2fa493fbdeaDocument22 pagesB71fedca 95fa 4b5b B32e A2fa493fbdeaRaj DasNo ratings yet

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- Income Tax Brief NotesDocument184 pagesIncome Tax Brief NotesCreanativeNo ratings yet

- Taxation Final ProjectDocument12 pagesTaxation Final ProjectShreya KalyaniNo ratings yet

- FinTax 1 MergedDocument320 pagesFinTax 1 Mergedayman abdul salamNo ratings yet

- Amndmnt I-M'21Document25 pagesAmndmnt I-M'21kri satNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- Q1) (A) Person - Section 2Document5 pagesQ1) (A) Person - Section 2Minal GandhiNo ratings yet

- Introduction To Income TaxDocument36 pagesIntroduction To Income TaxDeep ShahNo ratings yet

- Residential Status PDFDocument14 pagesResidential Status PDFPaiNo ratings yet

- Fema Provisions: Hassle Free Compliance WithDocument16 pagesFema Provisions: Hassle Free Compliance WithjitmNo ratings yet

- CTP - Residential Status & Scope of IncomeDocument7 pagesCTP - Residential Status & Scope of IncomeankushdeshmukhNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Income Tax Amendment - 2021 by CA Rajat MoghaDocument46 pagesIncome Tax Amendment - 2021 by CA Rajat MoghaOm Sai Enterprises100% (1)

- 2 Residential StatusDocument30 pages2 Residential StatusVEDANT SAININo ratings yet

- 2021 128 Taxmann Com 128 Article Recent Amendments Impacting Residential StatusDocument5 pages2021 128 Taxmann Com 128 Article Recent Amendments Impacting Residential StatusGunay ChandawatNo ratings yet

- Week 4 - Residence Based TaxationDocument31 pagesWeek 4 - Residence Based Taxationkabir kapoorNo ratings yet

- Residential Status and Scope of Total Income - AY 2023 - 24Document12 pagesResidential Status and Scope of Total Income - AY 2023 - 24Rajan SundararajanNo ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Lesson 2 Residential Status & Scope of Total IncomeDocument27 pagesLesson 2 Residential Status & Scope of Total Income1A 10 ASWIN RNo ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- DIRECT TAX I Bharathiar University B.com PADocument78 pagesDIRECT TAX I Bharathiar University B.com PAkalpanaNo ratings yet

- C. Law UNIT III - Foreign Exchange Management Act (FEMA Act)Document13 pagesC. Law UNIT III - Foreign Exchange Management Act (FEMA Act)Mr. funNo ratings yet

- Residential Status and Scope of Total IncomeDocument19 pagesResidential Status and Scope of Total IncomeSamyak JainNo ratings yet

- 4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-DayDocument9 pages4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-Dayvijay anandNo ratings yet

- International TaxationDocument22 pagesInternational TaxationGhamda Ram SiyagNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Adctx02 - 21 Paper 1Document7 pagesAdctx02 - 21 Paper 1Soumya swarup MohantyNo ratings yet

- Residential Status of An AssesseeDocument9 pagesResidential Status of An Assesseetanisha negiNo ratings yet

- PTS 2024 Preparatory Test 33 Solutions EngDocument28 pagesPTS 2024 Preparatory Test 33 Solutions EngPJ 123No ratings yet

- Income Deemed To Be Accrue or Arise inDocument41 pagesIncome Deemed To Be Accrue or Arise inPJ 123No ratings yet

- Abuse of Double Taxation Avoidance Agreement by Treaty PART-IDocument31 pagesAbuse of Double Taxation Avoidance Agreement by Treaty PART-IPJ 123No ratings yet

- Transfer Pricing PPT Case LawDocument17 pagesTransfer Pricing PPT Case LawPJ 123No ratings yet

- Taxation of Non-Residents With Special Reference To Chapter Xii and Xii ADocument16 pagesTaxation of Non-Residents With Special Reference To Chapter Xii and Xii APJ 123No ratings yet

- Mission LinksDocument42 pagesMission LinksPJ 123No ratings yet

- PMFIAS Geo HG 09 PortsDocument16 pagesPMFIAS Geo HG 09 PortsPJ 123No ratings yet

- Comparative PoliticsDocument7 pagesComparative PoliticsPJ 123No ratings yet

- Cases From Rattan LalDocument6 pagesCases From Rattan LalPJ 123No ratings yet

- R V MnaghtenDocument7 pagesR V MnaghtenRazor RockNo ratings yet

- Presentation 2Document10 pagesPresentation 2PJ 123No ratings yet

- Revocation or Termination of OfferDocument3 pagesRevocation or Termination of OfferPJ 123No ratings yet

- In Favour of An Investigation of The Relationship Between Vitamin B12 Deficiency and HIV InfectionDocument3 pagesIn Favour of An Investigation of The Relationship Between Vitamin B12 Deficiency and HIV InfectionPJ 123No ratings yet

- Cases On Strict LiabilityDocument9 pagesCases On Strict LiabilityPJ 123No ratings yet

- Supreme Court: Adultery Not A Crime, Women Not Property of Husbands, But Still Civil WrongDocument1 pageSupreme Court: Adultery Not A Crime, Women Not Property of Husbands, But Still Civil WrongPJ 123No ratings yet

- Types of ContractDocument6 pagesTypes of ContractPJ 123No ratings yet

- Scanned by CamscannerDocument2 pagesScanned by CamscannerPJ 123No ratings yet

- Gandhian Thoughts of Law & Justice: Dr. Nitesh D ChaudhariDocument5 pagesGandhian Thoughts of Law & Justice: Dr. Nitesh D ChaudhariPJ 123No ratings yet

- Prosecution of Civil ServantsDocument9 pagesProsecution of Civil ServantsPJ 123No ratings yet

- Doctrine of PrivityDocument6 pagesDoctrine of PrivityPJ 123No ratings yet

- Minor / Minority and Capacity To Contract: Case Mohoribibi vs. Dharmodas GhoseDocument6 pagesMinor / Minority and Capacity To Contract: Case Mohoribibi vs. Dharmodas GhosePJ 123No ratings yet

- Definition and Essentials of Offer and AcceptanceDocument7 pagesDefinition and Essentials of Offer and AcceptancePJ 123No ratings yet

- 08 - Chapter 3 PDFDocument39 pages08 - Chapter 3 PDFPJ 123No ratings yet

- ClsDocument1 pageClsPJ 123No ratings yet

- Class Notes Sebii PDFDocument232 pagesClass Notes Sebii PDFPJ 123No ratings yet

- Objectivity SubjectivityDocument12 pagesObjectivity SubjectivityPJ 123No ratings yet

- Supreme Court Monthly Digest-September 2019: Prakash Sahu V. SaulalDocument28 pagesSupreme Court Monthly Digest-September 2019: Prakash Sahu V. SaulalPJ 123No ratings yet

- Specific Relief Act 2018 AmendmentDocument6 pagesSpecific Relief Act 2018 AmendmentAbhilash AggarwalNo ratings yet

- Jurisdictional Challenges Parallel Proceedings Need For StayDocument12 pagesJurisdictional Challenges Parallel Proceedings Need For StayMeo U Luc LacNo ratings yet

- Secretary CertificateDocument2 pagesSecretary CertificateJanz CJNo ratings yet

- Go Vs MetropolitanDocument4 pagesGo Vs MetropolitanKayee KatNo ratings yet

- Ancient GreeceDocument26 pagesAncient GreeceGiuseppe De CorsoNo ratings yet

- Moneymax X Citibank GCash Exclusive Campaign T&CsDocument3 pagesMoneymax X Citibank GCash Exclusive Campaign T&CsProsserfina MinaoNo ratings yet

- SPPL 07 02 PDFDocument17 pagesSPPL 07 02 PDFFattia SyafiraNo ratings yet

- The Foreign Policy of Park Chung Hee (1968 - 1979)Document217 pagesThe Foreign Policy of Park Chung Hee (1968 - 1979)Viet NguyenNo ratings yet

- SHFC Applicant Data SheetDocument2 pagesSHFC Applicant Data SheetAlvy Faith Pel-eyNo ratings yet

- Bentham Anarchical Fallacies SummaryDocument3 pagesBentham Anarchical Fallacies SummaryYing Han100% (3)

- Elliot Dukke UsDocument7 pagesElliot Dukke UsNguyễn Phan Khánh LinhNo ratings yet

- 8200-0859-01-A0 Intlx InstallConfig EN PDFDocument94 pages8200-0859-01-A0 Intlx InstallConfig EN PDFFrancisco Rodriguez MartinezNo ratings yet

- FAQ299Document2 pagesFAQ299Eve GreenNo ratings yet

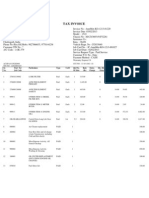

- Tax Invoice: Warranty Expired:NDocument3 pagesTax Invoice: Warranty Expired:NSanjay PatelNo ratings yet

- Revised Cef-1: Republic of The Philippines Commission On ElectionsDocument7 pagesRevised Cef-1: Republic of The Philippines Commission On ElectionsHeli CrossNo ratings yet

- Palma v. OmelioDocument12 pagesPalma v. OmelioMac SorianoNo ratings yet

- Correspondence Between My Friend, The Late Gordon T. "Gordy" Pratt, and Chicago Tribune Reporter Lisa Black and Editor Peter Hernon (Sept/Oct 2009)Document8 pagesCorrespondence Between My Friend, The Late Gordon T. "Gordy" Pratt, and Chicago Tribune Reporter Lisa Black and Editor Peter Hernon (Sept/Oct 2009)Peter M. HeimlichNo ratings yet

- Pass Amazon AWS Certified Solutions Architect - Associate Certification Exam in First Attempt Guaranteed!Document5 pagesPass Amazon AWS Certified Solutions Architect - Associate Certification Exam in First Attempt Guaranteed!Jan Rey AltivoNo ratings yet

- 8b. Title Disputes LLBP3007 22-23Document31 pages8b. Title Disputes LLBP3007 22-23Ismail PatelNo ratings yet

- Legal Ethics MCQDocument2 pagesLegal Ethics MCQronasolde50% (2)

- Corporate Finance SlidesDocument38 pagesCorporate Finance SlidesHaymaan Rashid DarNo ratings yet

- Kuda - External Analysis Delta FinalDocument10 pagesKuda - External Analysis Delta Finalkays chapanda100% (2)

- Section 194J: Fees For Professional or Technical ServicesDocument24 pagesSection 194J: Fees For Professional or Technical ServicesSAURABH TIBREWALNo ratings yet

- Saes K 110Document5 pagesSaes K 110mika cabelloNo ratings yet

- Ia 2Document2 pagesIa 2Nadine SofiaNo ratings yet

- Li Vs PeopleDocument1 pageLi Vs Peopledjango69No ratings yet

- Bar Exam Suggested Answers - 2017 Labor Law Bar Q&A AUGUST 31, 2018 2017 Labor Law Bar Questions and AnswersDocument17 pagesBar Exam Suggested Answers - 2017 Labor Law Bar Q&A AUGUST 31, 2018 2017 Labor Law Bar Questions and AnswersImma FoosaNo ratings yet

- Lecture 4 North Country Auto Case Performance MeasurementDocument5 pagesLecture 4 North Country Auto Case Performance MeasurementAprican ApriNo ratings yet

- Investment CodeDocument23 pagesInvestment CodeMaricrisNo ratings yet

- Southern National Bank of North Carolina v. Federal Resources Corporation Kenyon Home Furnishings, LTD., and James W. Pearce Elizabeth Contogiannis Steve Palinkas, 911 F.2d 724, 4th Cir. (1990)Document6 pagesSouthern National Bank of North Carolina v. Federal Resources Corporation Kenyon Home Furnishings, LTD., and James W. Pearce Elizabeth Contogiannis Steve Palinkas, 911 F.2d 724, 4th Cir. (1990)Scribd Government DocsNo ratings yet

- 5 Heirs - of - Sarili - v. - LagrosaDocument9 pages5 Heirs - of - Sarili - v. - LagrosaVincent john NacuaNo ratings yet

- Schedule - G 1Document6 pagesSchedule - G 1A RajaNo ratings yet