You might also like

- Residential Status and its Impact on Tax LiabilityDocument25 pagesResidential Status and its Impact on Tax LiabilityPJ 123No ratings yet

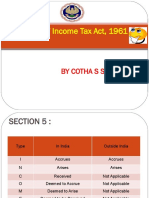

- Income Tax Act, 1961: Section - 5: Scope of Total IncomeDocument15 pagesIncome Tax Act, 1961: Section - 5: Scope of Total IncomeNisseem KrishnaNo ratings yet

- 1518759148pdfjoiner PDFDocument40 pages1518759148pdfjoiner PDFAlkaNo ratings yet

- Taxation Residential Status and Appeal ProvisionsDocument47 pagesTaxation Residential Status and Appeal ProvisionsSamata BohraNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Residential Status Cma IndaDocument10 pagesResidential Status Cma IndaKiran ChristyNo ratings yet

- 9Document4 pages9SPARSH KAPOORNo ratings yet

- Income Deemed To Accrue or Arise in India-Sec 9Document16 pagesIncome Deemed To Accrue or Arise in India-Sec 9drive8124No ratings yet

- Law of Taxation Law of Taxation Class Notes CompressDocument48 pagesLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshNo ratings yet

- Model Answers Law of TaxationDocument46 pagesModel Answers Law of Taxationlavkush1234No ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Taxation of Foreign Companies in Direct Taxes Code Bill PDFDocument6 pagesTaxation of Foreign Companies in Direct Taxes Code Bill PDFrajdeeppawarNo ratings yet

- Section 9Document7 pagesSection 9Achulendra Ji PushkarNo ratings yet

- Benefits Available To Non ResidentsDocument16 pagesBenefits Available To Non ResidentsArchita TiwariNo ratings yet

- Direct Tax Code SummaryDocument6 pagesDirect Tax Code SummaryShalini MahawarNo ratings yet

- Income Tax Guide for IndividualsDocument91 pagesIncome Tax Guide for IndividualsGiri SukumarNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Tax NotesDocument11 pagesTax NotesVishal DeshwalNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Weeks 4,5,6 - PDFDocument191 pagesWeeks 4,5,6 - PDFMehul Kumar MukulNo ratings yet

- Amndmnt I-M'21Document25 pagesAmndmnt I-M'21kri satNo ratings yet

- Q1) (A) Person - Section 2Document5 pagesQ1) (A) Person - Section 2Minal GandhiNo ratings yet

- Income Tax Brief NotesDocument184 pagesIncome Tax Brief NotesCreanativeNo ratings yet

- Sec 9Document39 pagesSec 9Akanksha BohraNo ratings yet

- Residential Status & Tax Incidence: DR Amit Kumar SinhaDocument14 pagesResidential Status & Tax Incidence: DR Amit Kumar SinhaasifanisNo ratings yet

- Residential Status and Tax IncidenceDocument14 pagesResidential Status and Tax IncidenceSugandha AgarwalNo ratings yet

- 01 Section 9Document54 pages01 Section 9ABHIJEETNo ratings yet

- 16 Taxtreatment Offoreign Income of Resident CRC 1Document68 pages16 Taxtreatment Offoreign Income of Resident CRC 1Vaibhavi NarNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- Principle of TaxationDocument7 pagesPrinciple of TaxationAnas YawarNo ratings yet

- Foreign Exchange Management Act (FEMA) overviewDocument13 pagesForeign Exchange Management Act (FEMA) overviewMr. funNo ratings yet

- Budget2017 18sudha 170215110415Document89 pagesBudget2017 18sudha 170215110415Taxpert mukeshNo ratings yet

- Income Tax Amendment - 2021 by CA Rajat MoghaDocument46 pagesIncome Tax Amendment - 2021 by CA Rajat MoghaOm Sai Enterprises100% (1)

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Definitions Residence and Tax LiabilityDocument23 pagesDefinitions Residence and Tax LiabilityVicky DNo ratings yet

- Income Tax Brief DemoDocument20 pagesIncome Tax Brief DemoZam HiaNo ratings yet

- Basis of Charge and Scope of TotalDocument24 pagesBasis of Charge and Scope of TotalSujithNo ratings yet

- 1806 Aditi Chandra Taxation Law IDocument26 pages1806 Aditi Chandra Taxation Law IAditi ChandraNo ratings yet

- FinTax Session 2: Residential Status and Key ConceptsDocument320 pagesFinTax Session 2: Residential Status and Key Conceptsayman abdul salamNo ratings yet

- 1328866787Chp 2 - Residence and Scope of Total IncomeDocument5 pages1328866787Chp 2 - Residence and Scope of Total IncomeMohiNo ratings yet

- Taxation Final ProjectDocument12 pagesTaxation Final ProjectShreya KalyaniNo ratings yet

- TDS on OTADocument4 pagesTDS on OTAabcxyznoneNo ratings yet

- Adctx02 - 21 Paper 1Document7 pagesAdctx02 - 21 Paper 1Soumya swarup MohantyNo ratings yet

- TAX Planning AssigmentDocument11 pagesTAX Planning AssigmentKaba TidianeNo ratings yet

- Residential status determination for individualsDocument14 pagesResidential status determination for individualsdhananjay7No ratings yet

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeDocument12 pagesCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliNo ratings yet

- B71fedca 95fa 4b5b B32e A2fa493fbdeaDocument22 pagesB71fedca 95fa 4b5b B32e A2fa493fbdeaRaj DasNo ratings yet

- Scope of Income Tax ActDocument16 pagesScope of Income Tax Actsyed junaid sultanNo ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Non Resident TaxationDocument123 pagesNon Resident Taxationguru1barkiNo ratings yet

- Marketing GRP 3Document75 pagesMarketing GRP 3Shivlal YadavNo ratings yet

- PWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsDocument5 pagesPWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsStikcon PmcNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Reading Material. Tax 1 (G)Document14 pagesReading Material. Tax 1 (G)Rahul RajNo ratings yet

- Financial, Assessment and Previous Years ExplainedDocument6 pagesFinancial, Assessment and Previous Years ExplainedVijayant DalalNo ratings yet

- Case BriefDocument6 pagesCase BriefVijayant DalalNo ratings yet

- Week - 2Document5 pagesWeek - 2Vijayant DalalNo ratings yet

- EssayDocument3 pagesEssayVijayant DalalNo ratings yet

- Neighbors Dispute Over Noise Leads to Tort ClaimsDocument6 pagesNeighbors Dispute Over Noise Leads to Tort ClaimsVijayant DalalNo ratings yet

- Legislative AnalysisDocument3 pagesLegislative AnalysisVijayant DalalNo ratings yet

- Week - 15Document3 pagesWeek - 15Vijayant DalalNo ratings yet

- Royalty CasesDocument1 pageRoyalty CasesVijayant DalalNo ratings yet

- Digital Taxation EvolutionDocument3 pagesDigital Taxation EvolutionVijayant DalalNo ratings yet

- Introduction To Tax LawDocument2 pagesIntroduction To Tax LawVijayant DalalNo ratings yet

- Tax Avoidance and EvasionDocument8 pagesTax Avoidance and EvasionVijayant DalalNo ratings yet

- Postpaid Bill AugDocument2 pagesPostpaid Bill Augsiva vNo ratings yet

- Diesel Pump of The Desmi GroupDocument10 pagesDiesel Pump of The Desmi Groupngocdhxd92No ratings yet

- Terms of Engagement - TMCS - GoldDocument14 pagesTerms of Engagement - TMCS - GoldPriyank KulshreshthaNo ratings yet

- Si Eft Mandate FormDocument1 pageSi Eft Mandate FormdSolarianNo ratings yet

- Surveying 2 Practical 3Document15 pagesSurveying 2 Practical 3Huzefa AliNo ratings yet

- FS1-Episode 10Document4 pagesFS1-Episode 10Mark Gerald Lagran82% (11)

- The Definition and Unit of Ionic StrengthDocument2 pagesThe Definition and Unit of Ionic StrengthDiego ZapataNo ratings yet

- Organization Structure in SAP Plant Maintenance: CommentsDocument3 pagesOrganization Structure in SAP Plant Maintenance: CommentsMarco Antônio Claret TeixeiraNo ratings yet

- STS Lesson 1-2Document23 pagesSTS Lesson 1-2zarnaih SmithNo ratings yet

- Prompt 2022Document12 pagesPrompt 2022cecilferrosNo ratings yet

- Module IV StaffingDocument3 pagesModule IV Staffingyang_19250% (1)

- CV HannahDocument3 pagesCV HannahRoxan DosdosNo ratings yet

- Landman Training ManualDocument34 pagesLandman Training Manualflashanon100% (2)

- MarketNexus Editor: Teri Buhl Character LetterDocument2 pagesMarketNexus Editor: Teri Buhl Character LetterTeri BuhlNo ratings yet

- Pathways Rw1 2e U7 TestDocument9 pagesPathways Rw1 2e U7 TestGrace Ann AbanteNo ratings yet

- Ky203817 PSRPT 2022-05-17 14.39.33Document8 pagesKy203817 PSRPT 2022-05-17 14.39.33Thuy AnhNo ratings yet

- Duttaphrynus Melanostictus,: Errata VersionDocument11 pagesDuttaphrynus Melanostictus,: Errata Versionutama 3002No ratings yet

- Microsoft Word BasicsDocument25 pagesMicrosoft Word Basicsitsudatte18No ratings yet

- Integrate Payments Direct Post APIDocument31 pagesIntegrate Payments Direct Post APIAnjali SharmaNo ratings yet

- Research Proposal HaDocument3 pagesResearch Proposal Haapi-446904695No ratings yet

- What Is ReligionDocument15 pagesWhat Is ReligionMary Glou Melo PadilloNo ratings yet

- NASA: 181330main Jun29colorDocument8 pagesNASA: 181330main Jun29colorNASAdocumentsNo ratings yet

- Return Snowball Device SafelyDocument1 pageReturn Snowball Device SafelyNoneNo ratings yet

- Processing, Handling and Storage of Agricultural Product 2Document6 pagesProcessing, Handling and Storage of Agricultural Product 2LittleagleNo ratings yet

- Warren BuffetDocument11 pagesWarren BuffetSopakirite Kuruye-AleleNo ratings yet

- Make Money OnlineDocument9 pagesMake Money OnlineTimiNo ratings yet

- 1868 Sop Work at HeightDocument10 pages1868 Sop Work at HeightAbid AzizNo ratings yet

- Sesame Seed: T. Y. Tunde-Akintunde, M. O. Oke and B. O. AkintundeDocument20 pagesSesame Seed: T. Y. Tunde-Akintunde, M. O. Oke and B. O. Akintundemarvellous ogbonnaNo ratings yet

- Sivas Doon LecturesDocument284 pagesSivas Doon LectureskartikscribdNo ratings yet

- Dasakam 31-40Document16 pagesDasakam 31-40Puducode Rama Iyer RamachanderNo ratings yet