You might also like

- Nolo's Essential Retirement Tax GuideDocument436 pagesNolo's Essential Retirement Tax GuideabuaasiyahNo ratings yet

- Salary Structure CalculatorDocument7 pagesSalary Structure CalculatorMakesh Gopalakrishnan0% (1)

- Cir V. Central Luzon Drug Corporation, GR No. 148512, 2006-06-26Document2 pagesCir V. Central Luzon Drug Corporation, GR No. 148512, 2006-06-26Crisbon ApalisNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Residential Status AssignmentDocument4 pagesResidential Status AssignmentSimran Kaur Khurana100% (1)

- GST Entries For Every Month SalesDocument3 pagesGST Entries For Every Month SalesGiri SukumarNo ratings yet

- Payslip 2022 2023 1 Aso8807 SOAGBALICDocument1 pagePayslip 2022 2023 1 Aso8807 SOAGBALICRamesh Kumar PrasadNo ratings yet

- Report of Law1 - Other Percentage TaxDocument16 pagesReport of Law1 - Other Percentage TaxJonalyn Maraña-ManuelNo ratings yet

- My Project Report On Icici Bank FinalDocument97 pagesMy Project Report On Icici Bank Finalgauravshuklapgdm71% (28)

- Prelim Examination Business TaxDocument16 pagesPrelim Examination Business Taxmikheal beyberNo ratings yet

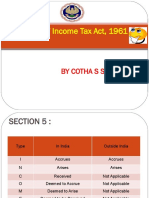

- Section 5 of Income Tax ActDocument4 pagesSection 5 of Income Tax ActParth PandeyNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Person (Section 2 (31) )Document1 pagePerson (Section 2 (31) )Tejas PandeyNo ratings yet

- Scope of Total IncomeDocument7 pagesScope of Total IncomeSatinderpal KaurNo ratings yet

- E Text Week 1 Module 1.5Document5 pagesE Text Week 1 Module 1.5bsc slpNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Scope of Total Income U/S. 5: Presented To:-Prof. SeemaDocument17 pagesScope of Total Income U/S. 5: Presented To:-Prof. SeemaRaksha ShettyNo ratings yet

- Introduction To ResidenceDocument4 pagesIntroduction To ResidenceNiya Maria NixonNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- CTPM ProblemsDocument31 pagesCTPM ProblemsViraja GuruNo ratings yet

- Income Tax Law & PracticeDocument32 pagesIncome Tax Law & PracticeGautam TamtaNo ratings yet

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeDocument12 pagesCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliNo ratings yet

- DTP 2nd ModuleDocument6 pagesDTP 2nd ModuleVeena GowdaNo ratings yet

- ch-11 Taxation of NRIsDocument25 pagesch-11 Taxation of NRIsdean.socNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- 3.2 Incidence of TaxDocument5 pages3.2 Incidence of Taxswathi jaiganeshNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Caa0eresidential StatusDocument13 pagesCaa0eresidential StatusShashwat MishraNo ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- The Direct Taxes CodeDocument3 pagesThe Direct Taxes Codeanuj91No ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Taxation Final ProjectDocument12 pagesTaxation Final ProjectShreya KalyaniNo ratings yet

- 2 Residential StatusDocument30 pages2 Residential StatusVEDANT SAININo ratings yet

- TaxationDocument15 pagesTaxationharshithaaba8No ratings yet

- Sia - Itax-2018-19Document17 pagesSia - Itax-2018-19Abhay Pethani.No ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Resdential Status Questionsby Garun Kumar GDCM SrikakulamDocument9 pagesResdential Status Questionsby Garun Kumar GDCM Srikakulamgeddadaarun100% (1)

- Income Tax Act, 1961: Section - 5: Scope of Total IncomeDocument15 pagesIncome Tax Act, 1961: Section - 5: Scope of Total IncomeNisseem KrishnaNo ratings yet

- Income Tax Planning-1Document32 pagesIncome Tax Planning-1Ashutosh ShuklaNo ratings yet

- Residential StatusDocument11 pagesResidential StatusSaurav MedhiNo ratings yet

- Residential StatusDocument17 pagesResidential Statussaif aliNo ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Incidence of TaxDocument53 pagesIncidence of TaxAnurag SindhalNo ratings yet

- Residential Status and Taxation For Individuals - Taxguru - inDocument2 pagesResidential Status and Taxation For Individuals - Taxguru - inSubhamNo ratings yet

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- Tax NotesDocument11 pagesTax NotesVishal DeshwalNo ratings yet

- 01 Section 9Document54 pages01 Section 9ABHIJEETNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- Residential Status Cma IndaDocument10 pagesResidential Status Cma IndaKiran ChristyNo ratings yet

- Principle of TaxationDocument7 pagesPrinciple of TaxationAnas YawarNo ratings yet

- Income TaxDocument22 pagesIncome TaxUjjwal AnandNo ratings yet

- 1328866787Chp 2 - Residence and Scope of Total IncomeDocument5 pages1328866787Chp 2 - Residence and Scope of Total IncomeMohiNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Q1) (A) Person - Section 2Document5 pagesQ1) (A) Person - Section 2Minal GandhiNo ratings yet

- Tenses: Shivani M. (PDP Dept.)Document21 pagesTenses: Shivani M. (PDP Dept.)Sandeep SinghNo ratings yet

- New Doc 2020-09-14 14.58.08Document2 pagesNew Doc 2020-09-14 14.58.08Sandeep SinghNo ratings yet

- What Is Management AccountingDocument11 pagesWhat Is Management AccountingSandeep SinghNo ratings yet

- Questions On GDDocument8 pagesQuestions On GDSandeep SinghNo ratings yet

- Proverbs in English With Meanings and Example SentencesDocument9 pagesProverbs in English With Meanings and Example SentencesSandeep SinghNo ratings yet

- Active Passive VoiceDocument6 pagesActive Passive VoiceSandeep SinghNo ratings yet

- Personal Interviews: Prepared By: Ms. Shivani Arora Assistant Professor Graphic Era Hill UniversityDocument8 pagesPersonal Interviews: Prepared By: Ms. Shivani Arora Assistant Professor Graphic Era Hill UniversitySandeep SinghNo ratings yet

- Cover Letter Resume 101 FundamentalsDocument3 pagesCover Letter Resume 101 FundamentalsSandeep SinghNo ratings yet

- Resume Writing: Prepared By: Ms. Shivani Arora Assistant Professor Graphic Era Hill UniversityDocument6 pagesResume Writing: Prepared By: Ms. Shivani Arora Assistant Professor Graphic Era Hill UniversitySandeep SinghNo ratings yet

- Idiom / Phrase Meaning Example SentenceDocument4 pagesIdiom / Phrase Meaning Example SentenceSandeep SinghNo ratings yet

- Taxes - Types of TaxesDocument2 pagesTaxes - Types of TaxesZie BeaNo ratings yet

- Survey of Metro Manila RPT RatesDocument6 pagesSurvey of Metro Manila RPT RatesMarcus DoroteoNo ratings yet

- Laxmi Metal Press Ing Works Pvt. LTD.: Invoice Cum ChallanDocument5 pagesLaxmi Metal Press Ing Works Pvt. LTD.: Invoice Cum ChallanSujit Kumar SinghNo ratings yet

- EMAILDocument1 pageEMAILSmdryfruits IranianNo ratings yet

- 911 KCC Buildcon PVT LTD Packege - 5Document1 page911 KCC Buildcon PVT LTD Packege - 5Kcc AlwarNo ratings yet

- Description: Tags: 0708depverwkshtFINAL1218906Document2 pagesDescription: Tags: 0708depverwkshtFINAL1218906anon-562432No ratings yet

- Tax Invoice / Bill of SupplyDocument1 pageTax Invoice / Bill of SupplyabhimanyuNo ratings yet

- Pacific Airlines Operated Both An Airline and Several Rental CarDocument1 pagePacific Airlines Operated Both An Airline and Several Rental CarAmit PandeyNo ratings yet

- EP Trucking DocumentsDocument6 pagesEP Trucking DocumentsKatieNo ratings yet

- Quiz 7 - Transfer PricingDocument2 pagesQuiz 7 - Transfer PricingAlbert XuNo ratings yet

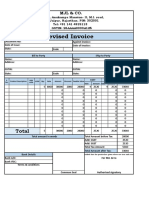

- Revised InvoiceDocument1 pageRevised InvoiceShaik NoorshaNo ratings yet

- Taxation, Types of Taxation, Main Objectives of TaxationDocument4 pagesTaxation, Types of Taxation, Main Objectives of TaxationKc Cassandra RosalNo ratings yet

- Form 16Document3 pagesForm 16Vikas PandyaNo ratings yet

- Hello SURESHA, Here's Your Tax Invoice: Original For RecipientDocument1 pageHello SURESHA, Here's Your Tax Invoice: Original For RecipientSuresh CANo ratings yet

- ICAEW - Tax - Mini Test 1 - STDDocument6 pagesICAEW - Tax - Mini Test 1 - STDlinhdinhphuong02No ratings yet

- FABM2121 Fundamentals of Accountancy Q2 Long Quiz 002Document6 pagesFABM2121 Fundamentals of Accountancy Q2 Long Quiz 002Christian Tero100% (2)

- There Is No Such Thing As 'SST'Document1 pageThere Is No Such Thing As 'SST'hfdghdhNo ratings yet

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- SPIT. Abella SamplexDocument5 pagesSPIT. Abella SamplexEins BalagtasNo ratings yet

- Tax Invoice - Ezcash: Transaction DetailsDocument1 pageTax Invoice - Ezcash: Transaction DetailsShoaib AbbasiNo ratings yet

- Ahmedabad Municipal Corporation Mahanagar Sewa SadanDocument1 pageAhmedabad Municipal Corporation Mahanagar Sewa SadanJohn FernendiceNo ratings yet

- Invoice Template 1Document2 pagesInvoice Template 1PramodhNo ratings yet