You might also like

- Subject: Taxation Law-I: Chanakya National Law University, PatnaDocument20 pagesSubject: Taxation Law-I: Chanakya National Law University, PatnaKritika SinghNo ratings yet

- FAQ On FDIDocument14 pagesFAQ On FDIParas ShahNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Amazon Supply ChainDocument18 pagesAmazon Supply Chainyatendra13288100% (2)

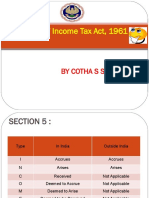

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- Incidence of TaxDocument53 pagesIncidence of TaxAnurag SindhalNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Tax NotesDocument11 pagesTax NotesVishal DeshwalNo ratings yet

- Tax Planning For An NRI: Pratul JainDocument3 pagesTax Planning For An NRI: Pratul Jainjanardhan lalwaniNo ratings yet

- Sia - Itax-2018-19Document17 pagesSia - Itax-2018-19Abhay Pethani.No ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Connotation of Receipt of Income and Accrual of IncomeDocument8 pagesConnotation of Receipt of Income and Accrual of Incomesuyash dugarNo ratings yet

- INTRODUCTION TO RESIDENCE & SCOPE OF TOTAL INCOMEDocument4 pagesINTRODUCTION TO RESIDENCE & SCOPE OF TOTAL INCOMENiya Maria NixonNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Basis of Charge and Scope of TotalDocument24 pagesBasis of Charge and Scope of TotalSujithNo ratings yet

- Personal Tax Planning 201718Document79 pagesPersonal Tax Planning 201718Deepak JainNo ratings yet

- Income Tax Guide for IndividualsDocument91 pagesIncome Tax Guide for IndividualsGiri SukumarNo ratings yet

- Taxation Residential Status and Income Deemed Received or AccruedDocument9 pagesTaxation Residential Status and Income Deemed Received or AccruedVineet RajNo ratings yet

- Permanent Esta researchDocument24 pagesPermanent Esta researchNeha PandeyNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Residential StatusDocument11 pagesResidential StatusSaurav MedhiNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- A Brief Study On International Taxation - Taxguru - inDocument7 pagesA Brief Study On International Taxation - Taxguru - inManas PatilNo ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Definitions: ST STDocument99 pagesDefinitions: ST STTapan PhadkeNo ratings yet

- Foreign Investment in IndiaDocument10 pagesForeign Investment in Indiaramashankar10No ratings yet

- 3.2 Incidence of TaxDocument5 pages3.2 Incidence of Taxswathi jaiganeshNo ratings yet

- 01 Section 9Document54 pages01 Section 9ABHIJEETNo ratings yet

- Residential StatusDocument17 pagesResidential Statussaif aliNo ratings yet

- Scope of Income Tax ActDocument16 pagesScope of Income Tax Actsyed junaid sultanNo ratings yet

- Notes LLB Tax Nav 2Document12 pagesNotes LLB Tax Nav 2amit HCSNo ratings yet

- Income Deemed To Accrue or Arise in IndiaDocument2 pagesIncome Deemed To Accrue or Arise in IndiaDhirendra SinghNo ratings yet

- Scope of Total Income U/S. 5: Presented To:-Prof. SeemaDocument17 pagesScope of Total Income U/S. 5: Presented To:-Prof. SeemaRaksha ShettyNo ratings yet

- FDI in India GuideDocument3 pagesFDI in India Guideabc defNo ratings yet

- Direct Tax Code SummaryDocument6 pagesDirect Tax Code SummaryShalini MahawarNo ratings yet

- FEMA RemovedDocument6 pagesFEMA RemovedUnknownNo ratings yet

- Tax Structure in India1Document9 pagesTax Structure in India1Subholina SenNo ratings yet

- Scope of Total Income and Residential StatusDocument3 pagesScope of Total Income and Residential StatusSandeep SinghNo ratings yet

- PWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsDocument5 pagesPWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsStikcon PmcNo ratings yet

- Residential Status and Taxability in IndiaDocument2 pagesResidential Status and Taxability in IndiaSubhamNo ratings yet

- Residential Status - May 2024 & Nov 2024Document2 pagesResidential Status - May 2024 & Nov 2024Rahul NegiNo ratings yet

- Checklist For 15CBDocument4 pagesChecklist For 15CBKrishna S MohanNo ratings yet

- E Text Week 1 Module 1.5Document5 pagesE Text Week 1 Module 1.5bsc slpNo ratings yet

- Bep 6Document14 pagesBep 6KAJAL KUMARINo ratings yet

- FDI - Important PointsDocument17 pagesFDI - Important PointsSavoir PenNo ratings yet

- Section 9 of Income Tax Act 1961Document55 pagesSection 9 of Income Tax Act 1961Bharath SimhaReddyNaiduNo ratings yet

- BFM CH 21 PDFDocument27 pagesBFM CH 21 PDFKiran KotlapatiNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- K.K. Jindal, Managing Director, Global Management Services New DelhiDocument61 pagesK.K. Jindal, Managing Director, Global Management Services New DelhiShashank GuptaNo ratings yet

- Definitions: ST STDocument121 pagesDefinitions: ST STKetan ThakkarNo ratings yet

- 40 - Section 9 of The Indian Income Tax ActDocument18 pages40 - Section 9 of The Indian Income Tax ActDhirendra SinghNo ratings yet

- Income deemed to accrue or arise in India under section 9Document13 pagesIncome deemed to accrue or arise in India under section 9Vicky DNo ratings yet

- Fema Provisions: Hassle Free Compliance WithDocument16 pagesFema Provisions: Hassle Free Compliance WithjitmNo ratings yet

- International Banking & Financing for NRIs and PIOsDocument15 pagesInternational Banking & Financing for NRIs and PIOsFaizaanKhanNo ratings yet

- Week 4-7Document9 pagesWeek 4-7Vijayant DalalNo ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- Non-Resident Investing in Indian Company Using NRO AccountDocument4 pagesNon-Resident Investing in Indian Company Using NRO AccountshubhamNo ratings yet

- Exploring Strateg1Document7 pagesExploring Strateg1soomsoomislamNo ratings yet

- COMPARISON OF PHILIPPINE TAX RATESDocument3 pagesCOMPARISON OF PHILIPPINE TAX RATESKevin JugaoNo ratings yet

- 3Q 2022 INDF Indofood+Sukses+Makmur+TbkDocument164 pages3Q 2022 INDF Indofood+Sukses+Makmur+TbkAdi Gesang PrayogaNo ratings yet

- Jurnal Ekonomika Vol 5 No 2 Des 2012inddDocument62 pagesJurnal Ekonomika Vol 5 No 2 Des 2012inddFaisalRahmatNo ratings yet

- Answers - Test - Strategic Management Class 0322Document5 pagesAnswers - Test - Strategic Management Class 0322Kuzi TolleNo ratings yet

- ILAC International College 2019 BrochureDocument32 pagesILAC International College 2019 BrochureLorz CatalinaNo ratings yet

- Zimbabwe Travel & Tourism GDP Falls Nearly 40% in 2020Document2 pagesZimbabwe Travel & Tourism GDP Falls Nearly 40% in 2020XXKEY2XXNo ratings yet

- PAL Exempt from Motor Vehicle Registration FeesDocument3 pagesPAL Exempt from Motor Vehicle Registration FeeskenNo ratings yet

- Process Interaction: Plutofab Engineers Private LimitedDocument1 pageProcess Interaction: Plutofab Engineers Private LimitedRahul MenchNo ratings yet

- SBA Loan Product MatrixDocument1 pageSBA Loan Product Matrixed_nycNo ratings yet

- Review of Literature on Solid Waste Management Methods and ImpactsDocument10 pagesReview of Literature on Solid Waste Management Methods and ImpactsIvy Joy UbinaNo ratings yet

- IBS301 International Business Work Plan 2023Document19 pagesIBS301 International Business Work Plan 2023sha ve3No ratings yet

- (Routledge Research in International Economic Law) Hao Wu - Trade Facilitation in The Multilateral Trading System - Genesis, Course and Accord-Routledge (2018)Document238 pages(Routledge Research in International Economic Law) Hao Wu - Trade Facilitation in The Multilateral Trading System - Genesis, Course and Accord-Routledge (2018)hasannbrNo ratings yet

- Chapter 6 - Organizational StudyDocument26 pagesChapter 6 - Organizational StudyRed SecretarioNo ratings yet

- Mobile Services Tax InvoiceDocument2 pagesMobile Services Tax InvoiceHemanth Kannan A SNo ratings yet

- Emerging Trends of InsiderDocument28 pagesEmerging Trends of InsiderShivamPandeyNo ratings yet

- Tu Delft Thesis Presentation TemplateDocument8 pagesTu Delft Thesis Presentation TemplateBuyEssaysOnlineForCollegeNewark100% (2)

- LEGAL DOSSIER AND LEGAL DOCUMENT IN ENGLISHDocument58 pagesLEGAL DOSSIER AND LEGAL DOCUMENT IN ENGLISHCristian Silva TapiaNo ratings yet

- Bill Wise DetailsDocument14 pagesBill Wise Detailsanandababu_cNo ratings yet

- Bolt May 201592181742354Document103 pagesBolt May 201592181742354Debasish RauloNo ratings yet

- Planning of Bank Branch AuditDocument9 pagesPlanning of Bank Branch AuditAshutosh PathakNo ratings yet

- GeM Bidding 3335448Document7 pagesGeM Bidding 3335448Bhumi ShahNo ratings yet

- HR Examiner's Guide to Free Speech at WorkDocument10 pagesHR Examiner's Guide to Free Speech at WorkShiba LodhiNo ratings yet

- Retention Strategies To Control Attrition Rate With Special Reference To BPO SectorDocument5 pagesRetention Strategies To Control Attrition Rate With Special Reference To BPO SectorInternational Journal in Management Research and Social ScienceNo ratings yet

- HISTORICAL ORIGINS AND FORMS OF UNDERDEVELOPMENT AND DEPENDENCE IN AFRICADocument21 pagesHISTORICAL ORIGINS AND FORMS OF UNDERDEVELOPMENT AND DEPENDENCE IN AFRICAJuma DutNo ratings yet

- Business Advantages and DisadvantagesDocument2 pagesBusiness Advantages and DisadvantagesTYA HERYANINo ratings yet

- Deloitte NL Risk Sdgs From A Business PerspectiveDocument51 pagesDeloitte NL Risk Sdgs From A Business PerspectiveAshraf ChowdhuryNo ratings yet

- Quality Assurance ProcedureDocument6 pagesQuality Assurance ProcedureTrivesh Sharma100% (1)

- Poa - Edu Loan1Document3 pagesPoa - Edu Loan1Anand JoshiNo ratings yet