You might also like

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Work Permit: Types of Work Permits & Work Permit ExemptionsFrom EverandWork Permit: Types of Work Permits & Work Permit ExemptionsNo ratings yet

- Personal Tax Planning 201718Document79 pagesPersonal Tax Planning 201718Deepak JainNo ratings yet

- Incidence of TaxDocument53 pagesIncidence of TaxAnurag SindhalNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- ch-11 Taxation of NRIsDocument25 pagesch-11 Taxation of NRIsdean.socNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential StatusDocument11 pagesResidential StatusSaurav MedhiNo ratings yet

- Sia - Itax-2018-19Document17 pagesSia - Itax-2018-19Abhay Pethani.No ratings yet

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- Income Tax Guide for IndividualsDocument91 pagesIncome Tax Guide for IndividualsGiri SukumarNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Residential StatusDocument17 pagesResidential Statussaif aliNo ratings yet

- Short Question AnswerDocument9 pagesShort Question AnswerJoshua LoyalNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- INTRODUCTION TO RESIDENCE & SCOPE OF TOTAL INCOMEDocument4 pagesINTRODUCTION TO RESIDENCE & SCOPE OF TOTAL INCOMENiya Maria NixonNo ratings yet

- Residential Status and Taxability in IndiaDocument2 pagesResidential Status and Taxability in IndiaSubhamNo ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- Residential StatusDocument24 pagesResidential StatusGaurav BeniwalNo ratings yet

- Income From SalaryDocument103 pagesIncome From SalaryNAVEEN ROYNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- 3.2 Incidence of TaxDocument5 pages3.2 Incidence of Taxswathi jaiganeshNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- Taxation: Unit 1: Income Tax Basic Concepts Residential Status and Incidence of TaxDocument32 pagesTaxation: Unit 1: Income Tax Basic Concepts Residential Status and Incidence of TaxnikkiNo ratings yet

- Scope of Total Income U/S. 5: Presented To:-Prof. SeemaDocument17 pagesScope of Total Income U/S. 5: Presented To:-Prof. SeemaRaksha ShettyNo ratings yet

- E Text Week 1 Module 1.5Document5 pagesE Text Week 1 Module 1.5bsc slpNo ratings yet

- Direct Taxation Compiled NotesDocument164 pagesDirect Taxation Compiled NotesSIDDHARTH ahlawatNo ratings yet

- Document .36Document15 pagesDocument .36jyotisingh6908501No ratings yet

- Analysis of Income Tax in IndiaDocument31 pagesAnalysis of Income Tax in IndiaAshwin NarayananNo ratings yet

- Income Tax FaqDocument11 pagesIncome Tax FaqNasir AhmedNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- DownloadDocument3 pagesDownloadSaranyaNo ratings yet

- Notes LLB Tax Nav 2Document12 pagesNotes LLB Tax Nav 2amit HCSNo ratings yet

- IncomeTax MaterialDocument91 pagesIncomeTax MaterialSandeep JaiswalNo ratings yet

- Checklist For 15CBDocument4 pagesChecklist For 15CBKrishna S MohanNo ratings yet

- Residential Status and TaxabilityDocument31 pagesResidential Status and TaxabilityViraja GuruNo ratings yet

- Fundamental of Taxation inDocument11 pagesFundamental of Taxation inprashmishah23No ratings yet

- Taxation of Foreign Nationals - Money ControlDocument1 pageTaxation of Foreign Nationals - Money ControlSankaram KasturiNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Tax Planning For An NRI: Pratul JainDocument3 pagesTax Planning For An NRI: Pratul Jainjanardhan lalwaniNo ratings yet

- Residential Status - May 2024 & Nov 2024Document2 pagesResidential Status - May 2024 & Nov 2024Rahul NegiNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Faq ITDocument9 pagesFaq ITManu GuptaNo ratings yet

- Residential Status & Scope of Income TaxDocument7 pagesResidential Status & Scope of Income TaxankushdeshmukhNo ratings yet

- Form 15Cb: U. Mohanan & Co Chartered AccountantDocument4 pagesForm 15Cb: U. Mohanan & Co Chartered AccountantKrishna S MohanNo ratings yet

- Direct Tax Indirect TaxDocument19 pagesDirect Tax Indirect TaxKrystle DseuzaNo ratings yet

- Fema Provisions: Hassle Free Compliance WithDocument16 pagesFema Provisions: Hassle Free Compliance WithjitmNo ratings yet

- Income Tax 1Document26 pagesIncome Tax 1Vismaya CholakkalNo ratings yet

- Income Tax: Basic Concepts and TermsDocument17 pagesIncome Tax: Basic Concepts and TermsSahitya Kumar SheeNo ratings yet

- Subject: Taxation Law-I: Chanakya National Law University, PatnaDocument20 pagesSubject: Taxation Law-I: Chanakya National Law University, PatnaKritika SinghNo ratings yet

- Income Tax Guide 2011-12: Residential Status, Rates, Salary, DeductionsDocument156 pagesIncome Tax Guide 2011-12: Residential Status, Rates, Salary, DeductionsSalman Ansari100% (1)

- Definitions: ST STDocument99 pagesDefinitions: ST STTapan PhadkeNo ratings yet

- Basis of Charge and Scope of TotalDocument24 pagesBasis of Charge and Scope of TotalSujithNo ratings yet

- 1 - Income Tax IntroductionDocument7 pages1 - Income Tax IntroductiondjNo ratings yet

- Income Tax Amendment - 2021 by CA Rajat MoghaDocument46 pagesIncome Tax Amendment - 2021 by CA Rajat MoghaOm Sai Enterprises100% (1)

- Income Tax Law PracticeDocument16 pagesIncome Tax Law PracticeTholai Nokku [ தொலை நோக்கு ]No ratings yet

- Historical Development of The Customs Act and Customs DutyDocument47 pagesHistorical Development of The Customs Act and Customs Dutysuyash dugarNo ratings yet

- Registration Under GSTDocument13 pagesRegistration Under GSTsuyash dugarNo ratings yet

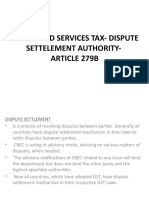

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Basic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, IrsDocument75 pagesBasic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, Irssuyash dugarNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- Transaction Value, Which Is The Price Actually Paid or PayableDocument10 pagesTransaction Value, Which Is The Price Actually Paid or Payablesuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- CUSTOMS DUTY AND TARIFF ACTSDocument26 pagesCUSTOMS DUTY AND TARIFF ACTSsuyash dugarNo ratings yet

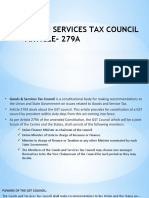

- Goods and Services Tax Council Article-279ADocument5 pagesGoods and Services Tax Council Article-279Asuyash dugarNo ratings yet

- Customs Valuation GuideDocument6 pagesCustoms Valuation Guidesuyash dugarNo ratings yet

- International TaxationDocument10 pagesInternational Taxationsuyash dugarNo ratings yet

- Than Money and Securities But Includes Actionable Claim, Growing CropsDocument8 pagesThan Money and Securities But Includes Actionable Claim, Growing Cropssuyash dugarNo ratings yet

- Indian income tax slabs for AY 2018-2019Document7 pagesIndian income tax slabs for AY 2018-2019suyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- UntitledDocument17 pagesUntitledsuyash dugarNo ratings yet

- International Tax SystemsDocument6 pagesInternational Tax Systemssuyash dugarNo ratings yet

- Taxable Event Explained in 40 CharactersDocument2 pagesTaxable Event Explained in 40 Characterssuyash dugarNo ratings yet

- UntitledDocument7 pagesUntitledsuyash dugarNo ratings yet

- Constitutional Amendments and Provisions of GST in IndiaDocument20 pagesConstitutional Amendments and Provisions of GST in Indiasuyash dugarNo ratings yet

- PrintDocument6 pagesPrintsuyash dugarNo ratings yet

- Adv & Dis Adv.Document6 pagesAdv & Dis Adv.suyash dugarNo ratings yet

- UntitledDocument12 pagesUntitledsuyash dugarNo ratings yet

- A Partnership Firm With A, B and C Partners.: IllustrationsDocument4 pagesA Partnership Firm With A, B and C Partners.: Illustrationssuyash dugarNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Tax FeeDocument1 pageTax Feesuyash dugarNo ratings yet

- Certificate of Creditable Tax Withheld at Source: Sta. Rosa Estate, Brgy. Macabling, Sta. Rosa City, LagunaDocument4 pagesCertificate of Creditable Tax Withheld at Source: Sta. Rosa Estate, Brgy. Macabling, Sta. Rosa City, Lagunaandrea mancaoNo ratings yet

- 349 SEC Investigating Melvin Capital Management - WSJDocument2 pages349 SEC Investigating Melvin Capital Management - WSJrahulNo ratings yet

- Hocmai TOEIC 450 Word Formation PracticeDocument5 pagesHocmai TOEIC 450 Word Formation PracticeDụ ThụNo ratings yet

- CorporationDocument1 pageCorporationHanaNo ratings yet

- Dwnload Full Essentials of Economics 10th Edition Schiller Solutions Manual PDFDocument20 pagesDwnload Full Essentials of Economics 10th Edition Schiller Solutions Manual PDFcryer.westing.44mwoe100% (10)

- Week 6-7 joint costs allocationDocument5 pagesWeek 6-7 joint costs allocationFebemay LindaNo ratings yet

- 2 1 4 PDFDocument4 pages2 1 4 PDFankusha SharmaNo ratings yet

- Apex Corporation Manufactures Eighteenth Century Classical StylDocument1 pageApex Corporation Manufactures Eighteenth Century Classical StylAmit Pandey0% (1)

- Credit Card Enrollment Cabaluna 2022Document3 pagesCredit Card Enrollment Cabaluna 2022Tracy AdraNo ratings yet

- Sem II Transportation Economics N EvaluationDocument2 pagesSem II Transportation Economics N EvaluationDwijendra ChanumoluNo ratings yet

- 10.1108@ijpdlm 05 2013 0112Document22 pages10.1108@ijpdlm 05 2013 0112Tú Vũ QuangNo ratings yet

- Presentation 1Document14 pagesPresentation 1Tanvi SidhayeNo ratings yet

- Print VAT Registration - GOV - UkDocument11 pagesPrint VAT Registration - GOV - Uksiva kumarNo ratings yet

- ReviewerDocument7 pagesReviewerKaye Mariz TolentinoNo ratings yet

- Sales Agency Accounting SystemDocument1 pageSales Agency Accounting Systemalmira garciaNo ratings yet

- 11 Risk and ReturnDocument11 pages11 Risk and ReturnHarinder SinghNo ratings yet

- Toyota Announces 2023 Car Sales Along With 2024 Domestic Sales Projection at 800,000 Units and Toyota Sales Target at 277,000 UnitsDocument6 pagesToyota Announces 2023 Car Sales Along With 2024 Domestic Sales Projection at 800,000 Units and Toyota Sales Target at 277,000 Unitslethuhoai3003No ratings yet

- Multifactor Models QuestionsDocument5 pagesMultifactor Models QuestionsJosh Brodsky0% (1)

- World Steel in FiguresDocument17 pagesWorld Steel in FiguresNashita espinoza maldonadoNo ratings yet

- 4 Comparative Accounting America and AsiaDocument17 pages4 Comparative Accounting America and AsiaNIARAMLINo ratings yet

- Lecture03 SlidesDocument50 pagesLecture03 Slidesaditya jainNo ratings yet

- Lesson 2: Learning ObjectiveDocument4 pagesLesson 2: Learning ObjectiveDante SausaNo ratings yet

- Soleto Vs SC (Sumitha S)Document2 pagesSoleto Vs SC (Sumitha S)MaChAnZzz OFFICIALNo ratings yet

- Graded Assignment 2 JCDocument12 pagesGraded Assignment 2 JCJustineNo ratings yet

- Financial Statement Analyses of Tata Motors LimitedDocument12 pagesFinancial Statement Analyses of Tata Motors LimitedJADUNATH HEMBRAMNo ratings yet

- Economics PYQ SSCDocument48 pagesEconomics PYQ SSCNitin Vishwakarma100% (1)

- CFASDocument5 pagesCFASBunny Kookie100% (1)

- Where Dreams Come: ANNUAL REPORT 2016-17Document212 pagesWhere Dreams Come: ANNUAL REPORT 2016-17Udayraj PatilNo ratings yet

- Siti Fatimah Azzahrah Binti Mohd Yazan: ObjectivesDocument1 pageSiti Fatimah Azzahrah Binti Mohd Yazan: ObjectivesZaraNo ratings yet

- Human Resources Performance Measurement Approaches Compared To Measures Used in Master's Theses in ASUDocument7 pagesHuman Resources Performance Measurement Approaches Compared To Measures Used in Master's Theses in ASUHugo Enrique Oblitas SalinasNo ratings yet