You might also like

- GST Unit 3Document61 pagesGST Unit 3SANSKRITI YADAV 22DM236No ratings yet

- Value of SupplyDocument23 pagesValue of SupplyBba ANo ratings yet

- Value of SupplyDocument35 pagesValue of Supplysaket kumarNo ratings yet

- Chapter 2-GST Part B - Value of SupplyDocument7 pagesChapter 2-GST Part B - Value of SupplyPooja D AcharyaNo ratings yet

- Value of Supply: Prem Kumar Nikel Adam. J Nikith .K .A Santosh KumarDocument8 pagesValue of Supply: Prem Kumar Nikel Adam. J Nikith .K .A Santosh KumarNikeladam JNo ratings yet

- GST Chalisa CH 6 - Value of Supply (R)Document5 pagesGST Chalisa CH 6 - Value of Supply (R)Bharatbhusan RoutNo ratings yet

- Goods and Service Tax: Programme Bachelor of CommerceDocument17 pagesGoods and Service Tax: Programme Bachelor of CommercemanjulaNo ratings yet

- Value of SupplyDocument10 pagesValue of SupplyAnshika PatwaNo ratings yet

- Value of SupplyDocument5 pagesValue of SupplyMohanNo ratings yet

- Value of Taxable Supply - Transaction ValueDocument36 pagesValue of Taxable Supply - Transaction ValueArun JyothiNo ratings yet

- Goods and Service Tax: Without Input CreditDocument44 pagesGoods and Service Tax: Without Input CreditpranjalNo ratings yet

- Valuation Rules Under GSTDocument16 pagesValuation Rules Under GSTHarshdeep SinghNo ratings yet

- Meaning and Scope of Supply Under GSTDocument5 pagesMeaning and Scope of Supply Under GSTRohit BajpaiNo ratings yet

- Value of SupplyDocument4 pagesValue of SupplyCupid FriendNo ratings yet

- Tax Mod 3Document7 pagesTax Mod 3Ayushi TiwariNo ratings yet

- Latest GST PPT DT 16 Apr 17Document29 pagesLatest GST PPT DT 16 Apr 17Venkatraman NatarajanNo ratings yet

- Value of SupplyDocument12 pagesValue of SupplyDrishti100% (1)

- Salient Features of GSTDocument9 pagesSalient Features of GSTKunal MalhotraNo ratings yet

- Goods and Service Tax (GST)Document29 pagesGoods and Service Tax (GST)Prince Digital ComputersNo ratings yet

- 2021 130 Taxmann Com 47 ArticleDocument3 pages2021 130 Taxmann Com 47 ArticleNaveenNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- 2015 VAT in Cambodia Sesion II 22aug 2015Document27 pages2015 VAT in Cambodia Sesion II 22aug 2015Sovanna HangNo ratings yet

- Basics of GSTDocument28 pagesBasics of GSTSandip JadavNo ratings yet

- GST Act 2017Document23 pagesGST Act 2017Deepak NimmojiNo ratings yet

- Treatment of Discounts Offers Free Samples in GSTDocument5 pagesTreatment of Discounts Offers Free Samples in GSTnaren.invincible244No ratings yet

- Tax, GST, Transfer PricingDocument11 pagesTax, GST, Transfer Pricingbiplav2uNo ratings yet

- 8 Value of Supply - TYBCOM FinalDocument13 pages8 Value of Supply - TYBCOM FinalNew AccountNo ratings yet

- 8 Value of Supply - TYBCOM FinalDocument13 pages8 Value of Supply - TYBCOM FinalNew AccountNo ratings yet

- Tax Credit For Inputs Under CENVAT and GST.Document28 pagesTax Credit For Inputs Under CENVAT and GST.Faisal AhmadNo ratings yet

- Value of SupplyDocument13 pagesValue of SupplyJasmin BidNo ratings yet

- Section 15 - Value of Taxable Supply - TIME AND VALUE OF SUPPLYDocument2 pagesSection 15 - Value of Taxable Supply - TIME AND VALUE OF SUPPLYalisagasaNo ratings yet

- GST Unit IiDocument20 pagesGST Unit IiMani Maran123No ratings yet

- GST DocumentationDocument32 pagesGST DocumentationTeju PawarNo ratings yet

- Pure Agent - Online Version - 20 June 2017Document3 pagesPure Agent - Online Version - 20 June 2017Rajendra SwarnakarNo ratings yet

- Imposition of Supplementary DutyDocument7 pagesImposition of Supplementary DutyHarippa23No ratings yet

- Unit 3eDocument11 pagesUnit 3ebasavaraj nayakNo ratings yet

- Chapter 6 ValueofTaxableSupplyDocument21 pagesChapter 6 ValueofTaxableSupplyDR. PREETI JINDALNo ratings yet

- Value of Taxable Supply of Goods or Services or BothDocument10 pagesValue of Taxable Supply of Goods or Services or BothyashNo ratings yet

- Tax Planning and Financial Management Decisions: CA Aarti PatkiDocument50 pagesTax Planning and Financial Management Decisions: CA Aarti PatkiRahul SinghNo ratings yet

- VAT SlidesDocument137 pagesVAT SlidesLebogang MashigoNo ratings yet

- Input Tax credit-GSTDocument17 pagesInput Tax credit-GSTSandhya DangiNo ratings yet

- Background of Works Contract Under GST Works Contract" Means A Contract For BuildingDocument4 pagesBackground of Works Contract Under GST Works Contract" Means A Contract For BuildingSATYANARAYANA MOTAMARRINo ratings yet

- Chapter 7 - Value of Supply - NotesDocument16 pagesChapter 7 - Value of Supply - NotesPuran GuptaNo ratings yet

- 6-GST - Declaration Form For GSTDocument1 page6-GST - Declaration Form For GSTvishal.nithamNo ratings yet

- Value of SupplyDocument36 pagesValue of SupplyTreesa Mary RejiNo ratings yet

- Annexure FDocument1 pageAnnexure FAnanta Engineering SolutionNo ratings yet

- Module III Valuation in GSTDocument89 pagesModule III Valuation in GSTAyushi TiwariNo ratings yet

- 4-GST Special Commercial Terms and Conditions RevisedDocument7 pages4-GST Special Commercial Terms and Conditions Revisedvishal.nithamNo ratings yet

- GST Notes For Vi SemesterDocument55 pagesGST Notes For Vi SemesterNagashree RANo ratings yet

- Taxable Event Under GSTDocument4 pagesTaxable Event Under GSTSuman SharmaNo ratings yet

- 51 GST Flyer Chapter29Document12 pages51 GST Flyer Chapter29GB Pranav LalNo ratings yet

- Value Added Tax (Cap 476)Document15 pagesValue Added Tax (Cap 476)Triila manillaNo ratings yet

- Direct and Indirect TaxDocument12 pagesDirect and Indirect TaxSresth VermaNo ratings yet

- Hindustan Shipyard Ltd - ि◌ह̢दु ◌ािनशपया ड´ ि◌ल: Commercial Division (An ISO 9001:2015 Company)Document16 pagesHindustan Shipyard Ltd - ि◌ह̢दु ◌ािनशपया ड´ ि◌ल: Commercial Division (An ISO 9001:2015 Company)satyanand chNo ratings yet

- Itc GSTDocument27 pagesItc GSTShivam GoelNo ratings yet

- ST Determtn Value Rules 1Document4 pagesST Determtn Value Rules 1Poonam GuptaNo ratings yet

- Input Tax Credit Mechanism in GSTDocument9 pagesInput Tax Credit Mechanism in GSThanumanthaiahgowdaNo ratings yet

- Background: It Is Very Common Practice in The Construction or Infrastructure Related Industries That TheDocument10 pagesBackground: It Is Very Common Practice in The Construction or Infrastructure Related Industries That TheViral BakhadaNo ratings yet

- GST Annexure: Timely Provision of Invoices/debit Note/Credit Note/Other Applicable DocumentsDocument3 pagesGST Annexure: Timely Provision of Invoices/debit Note/Credit Note/Other Applicable Documentsshuklaankit704_24016No ratings yet

- Registration Under GSTDocument13 pagesRegistration Under GSTsuyash dugarNo ratings yet

- Basic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, IrsDocument75 pagesBasic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, Irssuyash dugarNo ratings yet

- Historical Development of The Customs Act and Customs DutyDocument47 pagesHistorical Development of The Customs Act and Customs Dutysuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

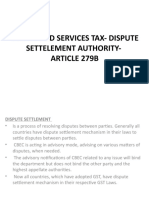

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

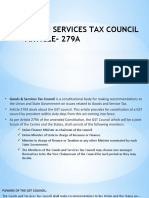

- Goods and Services Tax Council Article-279ADocument5 pagesGoods and Services Tax Council Article-279Asuyash dugarNo ratings yet

- Than Money and Securities But Includes Actionable Claim, Growing CropsDocument8 pagesThan Money and Securities But Includes Actionable Claim, Growing Cropssuyash dugarNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- Customs ValuationDocument6 pagesCustoms Valuationsuyash dugarNo ratings yet

- UntitledDocument26 pagesUntitledsuyash dugarNo ratings yet

- Income Tax Slabs Tax RateDocument7 pagesIncome Tax Slabs Tax Ratesuyash dugarNo ratings yet

- International TaxationDocument6 pagesInternational Taxationsuyash dugarNo ratings yet

- International TaxationDocument10 pagesInternational Taxationsuyash dugarNo ratings yet

- UntitledDocument17 pagesUntitledsuyash dugarNo ratings yet

- UntitledDocument7 pagesUntitledsuyash dugarNo ratings yet

- Constitutional Amendments and Provisions of GST in IndiaDocument20 pagesConstitutional Amendments and Provisions of GST in Indiasuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- Connotation of Receipt of Income and Accrual of IncomeDocument8 pagesConnotation of Receipt of Income and Accrual of Incomesuyash dugarNo ratings yet

- PrintDocument6 pagesPrintsuyash dugarNo ratings yet

- Taxable EventDocument2 pagesTaxable Eventsuyash dugarNo ratings yet

- UntitledDocument12 pagesUntitledsuyash dugarNo ratings yet

- A Partnership Firm With A, B and C Partners.: IllustrationsDocument4 pagesA Partnership Firm With A, B and C Partners.: Illustrationssuyash dugarNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- Adv & Dis Adv.Document6 pagesAdv & Dis Adv.suyash dugarNo ratings yet

- Tax FeeDocument1 pageTax Feesuyash dugarNo ratings yet

- Lesson 73 Creating Problems Involving The Volume of A Rectangular PrismDocument17 pagesLesson 73 Creating Problems Involving The Volume of A Rectangular PrismJessy James CardinalNo ratings yet

- Account Intel Sample 3Document28 pagesAccount Intel Sample 3CI SamplesNo ratings yet

- Curriculum Vitae Mukhammad Fitrah Malik FINAL 2Document1 pageCurriculum Vitae Mukhammad Fitrah Malik FINAL 2Bill Divend SihombingNo ratings yet

- Medicidefamilie 2011Document6 pagesMedicidefamilie 2011Mesaros AlexandruNo ratings yet

- Aero - 2013q2 Apu On DemandDocument32 pagesAero - 2013q2 Apu On DemandIvan MilosevicNo ratings yet

- Mathematics Into TypeDocument114 pagesMathematics Into TypeSimosBeikosNo ratings yet

- Sayyid DynastyDocument19 pagesSayyid DynastyAdnanNo ratings yet

- Monastery in Buddhist ArchitectureDocument8 pagesMonastery in Buddhist ArchitectureabdulNo ratings yet

- Government by Algorithm - Artificial Intelligence in Federal Administrative AgenciesDocument122 pagesGovernment by Algorithm - Artificial Intelligence in Federal Administrative AgenciesRone Eleandro dos SantosNo ratings yet

- Launchy 1.25 Readme FileDocument10 pagesLaunchy 1.25 Readme Fileagatzebluz100% (1)

- Chain of CommandDocument6 pagesChain of CommandDale NaughtonNo ratings yet

- All Zone Road ListDocument46 pagesAll Zone Road ListMegha ZalaNo ratings yet

- Wetlands Denote Perennial Water Bodies That Originate From Underground Sources of Water or RainsDocument3 pagesWetlands Denote Perennial Water Bodies That Originate From Underground Sources of Water or RainsManish thapaNo ratings yet

- B. Inggris Narrative TeksDocument11 pagesB. Inggris Narrative TeksDew FitriNo ratings yet

- Claim &: Change ProposalDocument45 pagesClaim &: Change ProposalInaam Ullah MughalNo ratings yet

- 37 Sample Resolutions Very Useful, Indian Companies Act, 1956Document38 pages37 Sample Resolutions Very Useful, Indian Companies Act, 1956CA Vaibhav Maheshwari70% (23)

- Conductivity MeterDocument59 pagesConductivity MeterMuhammad AzeemNo ratings yet

- My Parenting DnaDocument4 pagesMy Parenting Dnaapi-468161460No ratings yet

- Feuerhahn Funeral Bullet 17 March 2015Document12 pagesFeuerhahn Funeral Bullet 17 March 2015brandy99No ratings yet

- Steven SheaDocument1 pageSteven Sheaapi-345674935No ratings yet

- TEsis Doctoral en SuecoDocument312 pagesTEsis Doctoral en SuecoPruebaNo ratings yet

- The BreakupDocument22 pagesThe BreakupAllison CreaghNo ratings yet

- La Fonction Compositionnelle Des Modulateurs en Anneau Dans: MantraDocument6 pagesLa Fonction Compositionnelle Des Modulateurs en Anneau Dans: MantracmescogenNo ratings yet

- Logo DesignDocument4 pagesLogo Designdarshan kabraNo ratings yet

- Account Statement From 1 Jan 2017 To 30 Jun 2017Document2 pagesAccount Statement From 1 Jan 2017 To 30 Jun 2017Ujjain mpNo ratings yet

- Employer'S Virtual Pag-Ibig Enrollment Form: Address and Contact DetailsDocument2 pagesEmployer'S Virtual Pag-Ibig Enrollment Form: Address and Contact DetailstheffNo ratings yet

- " Thou Hast Made Me, and Shall Thy Work Decay?Document2 pages" Thou Hast Made Me, and Shall Thy Work Decay?Sbgacc SojitraNo ratings yet

- Oral Communication in ContextDocument31 pagesOral Communication in ContextPrecious Anne Prudenciano100% (1)

- Chapter 15 (Partnerships Formation, Operation and Ownership Changes) PDFDocument58 pagesChapter 15 (Partnerships Formation, Operation and Ownership Changes) PDFAbdul Rahman SholehNo ratings yet

- MC Donald'sDocument30 pagesMC Donald'sAbdullahWaliNo ratings yet