You might also like

- Background of The Goods and Services Tax CouncilDocument3 pagesBackground of The Goods and Services Tax CouncilPranay VermaNo ratings yet

- GST Council - StudyDocument3 pagesGST Council - Studyahil XO1BDNo ratings yet

- Mandate of GST CouncilDocument4 pagesMandate of GST CouncilDevil DemonNo ratings yet

- Prashant: Bba Z3 Subject: GST (Goods & Services Tax) Presentation Topic: GST COUNCILDocument9 pagesPrashant: Bba Z3 Subject: GST (Goods & Services Tax) Presentation Topic: GST COUNCILPrashant JiNo ratings yet

- Presentation 1Document8 pagesPresentation 1AR Ananth Rohith BhatNo ratings yet

- GST CouncilDocument2 pagesGST CouncilMilind SwaroopNo ratings yet

- GST Council: MR Aditya Vikram Advocate Visiting Faculty in Bharti College, DU & IITM College, IP UniversityDocument9 pagesGST Council: MR Aditya Vikram Advocate Visiting Faculty in Bharti College, DU & IITM College, IP UniversityNavendu ShuklaNo ratings yet

- Universityof Lucknow Faculty of Law: SESSION 2020-21 Assignment of Taxation Law Topic-Gst CouncilDocument6 pagesUniversityof Lucknow Faculty of Law: SESSION 2020-21 Assignment of Taxation Law Topic-Gst CouncilGoldi SinghNo ratings yet

- Sem. Subject: GST & Indirect Tax (Core - 14) : Unit - 4 Syllabus: GST Council and Regulatory FrameworkDocument7 pagesSem. Subject: GST & Indirect Tax (Core - 14) : Unit - 4 Syllabus: GST Council and Regulatory FrameworkAnwesha HotaNo ratings yet

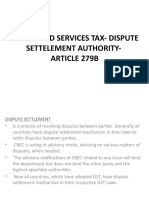

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- GST NotesDocument18 pagesGST NotesNasmaNo ratings yet

- LLB Taxation Law Unit-3 Part - 1-1 PDFDocument44 pagesLLB Taxation Law Unit-3 Part - 1-1 PDFravi kumarNo ratings yet

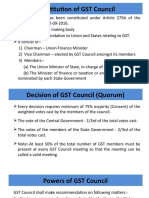

- Constitution of GSTDocument8 pagesConstitution of GSTGauharNo ratings yet

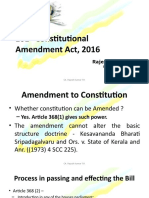

- 101 Constitutional Amendment Act - GSTDocument28 pages101 Constitutional Amendment Act - GSTRajesh KumarNo ratings yet

- GSTDocument5 pagesGSTSourav KaranthNo ratings yet

- GST - Uniting India: CA. Rajendra Kumar P, FCA, Chartered AccountantDocument3 pagesGST - Uniting India: CA. Rajendra Kumar P, FCA, Chartered AccountantMuhammed Aslam NVNo ratings yet

- GST Unit 1Document25 pagesGST Unit 1SHARATH JNo ratings yet

- GST - Brief - Exports and RefundsDocument18 pagesGST - Brief - Exports and RefundsSteve MclarenNo ratings yet

- 1-Overview of GST - Model GST LawDocument58 pages1-Overview of GST - Model GST Lawaditya_vyas_13No ratings yet

- Week - 15Document3 pagesWeek - 15Vijayant DalalNo ratings yet

- GST - UNIT 1 (Updated 2022)Document130 pagesGST - UNIT 1 (Updated 2022)Krish GoelNo ratings yet

- GST CouncilDocument3 pagesGST Councilaniket singhNo ratings yet

- Administration & ClassificationDocument3 pagesAdministration & Classification974-Abhijeet MotewarNo ratings yet

- Goods and Service Tax: Unit 2Document45 pagesGoods and Service Tax: Unit 2pradhyumn yadavNo ratings yet

- SM GSTDocument12 pagesSM GSTPranav TejaNo ratings yet

- 01032018-GST Concept and StatusDocument16 pages01032018-GST Concept and StatusGanesh AnantharamNo ratings yet

- Participant's NoteDocument11 pagesParticipant's NoteaskNo ratings yet

- GST CouncilDocument12 pagesGST CouncilPresidency UniversityNo ratings yet

- GST Concept and StatusDocument11 pagesGST Concept and Statusichchhit srivastavaNo ratings yet

- Chapter 3 - Charge of GST - NotesDocument17 pagesChapter 3 - Charge of GST - NotesHarsh SawantNo ratings yet

- Basics of GST PDFDocument23 pagesBasics of GST PDFmaxsoniiNo ratings yet

- GST Concept Status Ason 03062017 PDFDocument15 pagesGST Concept Status Ason 03062017 PDFAarti MoreNo ratings yet

- Introduction To Goods and Service Tax (GST) - PART 1Document5 pagesIntroduction To Goods and Service Tax (GST) - PART 1Sakthi MaheswariNo ratings yet

- PGD-GST 2020 Batch - Paper I 26-09-2020Document31 pagesPGD-GST 2020 Batch - Paper I 26-09-2020hampaiahNo ratings yet

- GST IntroductionDocument13 pagesGST IntroductionAnjali Krishna SNo ratings yet

- Law of Taxation - GST CouncilDocument22 pagesLaw of Taxation - GST CouncilSRILAKSHMI GHATENo ratings yet

- Tax Law IIDocument20 pagesTax Law IIaffan QureshiNo ratings yet

- GST - Concept & Status - May, 2016: For Departmental Officers OnlyDocument6 pagesGST - Concept & Status - May, 2016: For Departmental Officers Onlydroy21No ratings yet

- Intro To GST 09.11Document18 pagesIntro To GST 09.11aashrit sukhijaNo ratings yet

- Model Answer ScriptDocument9 pagesModel Answer ScriptPresidency UniversityNo ratings yet

- Chapter I: Implementation of GSTDocument23 pagesChapter I: Implementation of GSTTax NatureNo ratings yet

- K Vaitheeswaran CTC GST Jaipur 9 1 2020Document37 pagesK Vaitheeswaran CTC GST Jaipur 9 1 2020Shayan ZafarNo ratings yet

- GST 25dec14Document23 pagesGST 25dec14Mangesh BarhateNo ratings yet

- Assignment On GST CouncilDocument4 pagesAssignment On GST CouncilSimran Kaur KhuranaNo ratings yet

- The GST Council and Five Next Steps For The GST V BhaskarDocument4 pagesThe GST Council and Five Next Steps For The GST V Bhaskarpartha_pbhNo ratings yet

- Goods & Servics Tax (GST)Document7 pagesGoods & Servics Tax (GST)venkateshNo ratings yet

- TAX LAW II NotesDocument10 pagesTAX LAW II Notesaffan QureshiNo ratings yet

- Goods and Services Tax (G-2Document69 pagesGoods and Services Tax (G-2Sahil GogiaNo ratings yet

- Tax 5Document3 pagesTax 5JK Lights TradingNo ratings yet

- Gstconference NoticeDocument4 pagesGstconference NoticegauravNo ratings yet

- GST Notes For Sem 4Document7 pagesGST Notes For Sem 4prakhar100% (1)

- GST Definition, Objective, Framework, Action Plan, GST ScopeDocument8 pagesGST Definition, Objective, Framework, Action Plan, GST ScopeKATNo ratings yet

- Goods and Service Tax-AnDocument12 pagesGoods and Service Tax-AnAtreya GanchaudhuriNo ratings yet

- 18 Simple Steps To Know About GSTDocument81 pages18 Simple Steps To Know About GSTSrinivas PadakantiNo ratings yet

- DraftDocument36 pagesDraftAbhinand SadhanandanNo ratings yet

- Unit-1 GST (Continuation)Document70 pagesUnit-1 GST (Continuation)Anurag KandariNo ratings yet

- Detailed Presentation On GST by CBECDocument43 pagesDetailed Presentation On GST by CBECRajat GoyalNo ratings yet

- GST ProjectDocument53 pagesGST Projectafaque khan0% (1)

- Taxation LawDocument19 pagesTaxation LawMayank SarafNo ratings yet

- Registration Under GSTDocument13 pagesRegistration Under GSTsuyash dugarNo ratings yet

- Basic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, IrsDocument75 pagesBasic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, Irssuyash dugarNo ratings yet

- Historical Development of The Customs Act and Customs DutyDocument47 pagesHistorical Development of The Customs Act and Customs Dutysuyash dugarNo ratings yet

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Transaction Value, Which Is The Price Actually Paid or PayableDocument10 pagesTransaction Value, Which Is The Price Actually Paid or Payablesuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- Than Money and Securities But Includes Actionable Claim, Growing CropsDocument8 pagesThan Money and Securities But Includes Actionable Claim, Growing Cropssuyash dugarNo ratings yet

- Customs ValuationDocument6 pagesCustoms Valuationsuyash dugarNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- Constitutional Amendments and Provisions of GST in IndiaDocument20 pagesConstitutional Amendments and Provisions of GST in Indiasuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- Income Tax Slabs Tax RateDocument7 pagesIncome Tax Slabs Tax Ratesuyash dugarNo ratings yet

- UntitledDocument26 pagesUntitledsuyash dugarNo ratings yet

- Taxable EventDocument2 pagesTaxable Eventsuyash dugarNo ratings yet

- UntitledDocument7 pagesUntitledsuyash dugarNo ratings yet

- International TaxationDocument10 pagesInternational Taxationsuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- International TaxationDocument6 pagesInternational Taxationsuyash dugarNo ratings yet

- Connotation of Receipt of Income and Accrual of IncomeDocument8 pagesConnotation of Receipt of Income and Accrual of Incomesuyash dugarNo ratings yet

- UntitledDocument17 pagesUntitledsuyash dugarNo ratings yet

- Tax FeeDocument1 pageTax Feesuyash dugarNo ratings yet

- UntitledDocument12 pagesUntitledsuyash dugarNo ratings yet

- PrintDocument6 pagesPrintsuyash dugarNo ratings yet

- Adv & Dis Adv.Document6 pagesAdv & Dis Adv.suyash dugarNo ratings yet

- Agricultural IncomeDocument16 pagesAgricultural Incomesuyash dugarNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- A Partnership Firm With A, B and C Partners.: IllustrationsDocument4 pagesA Partnership Firm With A, B and C Partners.: Illustrationssuyash dugarNo ratings yet

- Excise DutyDocument14 pagesExcise Dutysuyash dugarNo ratings yet

- 12312/netaji Express Second Ac (2A)Document2 pages12312/netaji Express Second Ac (2A)SAYAN SARKARNo ratings yet

- Hotel BillDocument1 pageHotel BillTaher MaimoonNo ratings yet

- Value of SupplyDocument12 pagesValue of SupplyDrishti100% (1)

- Accounting Voucher PDFDocument2 pagesAccounting Voucher PDFVenky SamNo ratings yet

- Flipkart Labels 30 Sep 2022-10-44Document25 pagesFlipkart Labels 30 Sep 2022-10-44NANDA KUMARNo ratings yet

- Ewaybill - Master Steel - 01112019Document1 pageEwaybill - Master Steel - 01112019AshishNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Mayu PatNo ratings yet

- Internship Report: Department of CommerceDocument23 pagesInternship Report: Department of CommerceSriram SriramNo ratings yet

- Invoice - Dhanraj1992 APRIL-23 PDDocument1 pageInvoice - Dhanraj1992 APRIL-23 PDAinta GaurNo ratings yet

- Ola Bill From Citi To Home PDFDocument3 pagesOla Bill From Citi To Home PDFSiddhesh Jain0% (1)

- 12805/janmabhoomi Exp Second Sitting (2S)Document2 pages12805/janmabhoomi Exp Second Sitting (2S)satwika ChristieNo ratings yet

- Avenue E-Commerce Limited: 00009595951009285849 Crate IdDocument2 pagesAvenue E-Commerce Limited: 00009595951009285849 Crate IdPratik GadgeNo ratings yet

- Tax Reform & GST: A Systematic Literature Review: October 2017Document15 pagesTax Reform & GST: A Systematic Literature Review: October 2017Aaron NadarNo ratings yet

- 25-7-21 611 nf-8175 GST QueDocument4 pages25-7-21 611 nf-8175 GST QueJignesh NagarNo ratings yet

- 2018-NASSCOM-Startup Ecosystem-Product Opportunities Driving USD 10 Trillion EconomyDocument117 pages2018-NASSCOM-Startup Ecosystem-Product Opportunities Driving USD 10 Trillion Economyrishabh gargNo ratings yet

- Byod App. FormDocument8 pagesByod App. FormAbhishek KumawatNo ratings yet

- Sachin Internship ReportDocument58 pagesSachin Internship ReportAnshul VermaNo ratings yet

- 3 Sales Invoice RelaxoDocument3 pages3 Sales Invoice RelaxoSantosh OjhaNo ratings yet

- Delivery Summary: Order DateDocument4 pagesDelivery Summary: Order Datemohammad AmirNo ratings yet

- Cer Ficate Course in Community Health Examina On 2020-21: ReceiptDocument4 pagesCer Ficate Course in Community Health Examina On 2020-21: ReceiptSurender YadavNo ratings yet

- Signing Date: 26/02/2020 07:16:35 SGT Signed By: Ds CWT India PVT LTD 02Document2 pagesSigning Date: 26/02/2020 07:16:35 SGT Signed By: Ds CWT India PVT LTD 02Vrushank KanekarNo ratings yet

- Paper/ Subject Code: 44806 / Taxation - IV (Indirect TaxesDocument5 pagesPaper/ Subject Code: 44806 / Taxation - IV (Indirect TaxesVJ GroupNo ratings yet

- Irctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Document1 pageIrctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Anthony BoretoNo ratings yet

- Chandra Enterprises-059Document4 pagesChandra Enterprises-059Aarvee FoodNo ratings yet

- Sip Project On Hotel Industry PDFDocument34 pagesSip Project On Hotel Industry PDFDarshan BhanageNo ratings yet

- Goods and Service Tax: Without Input CreditDocument44 pagesGoods and Service Tax: Without Input CreditpranjalNo ratings yet

- Ride Details Bill Details: Thanks For Travelling With Us, Sumit Kumar MehraDocument3 pagesRide Details Bill Details: Thanks For Travelling With Us, Sumit Kumar Mehrasumit mehraNo ratings yet

- GST Ek Kahani - May 23Document139 pagesGST Ek Kahani - May 23Maliya BhaiNo ratings yet

- Medicine Agecies TMK (2 Files Merged)Document2 pagesMedicine Agecies TMK (2 Files Merged)Sushil AgarwalNo ratings yet

- 07446/LPI CCT SPL Sleeper Class (SL)Document2 pages07446/LPI CCT SPL Sleeper Class (SL)sandeepNo ratings yet