You might also like

- The Entrepreneurial Mind SYLLABUSDocument5 pagesThe Entrepreneurial Mind SYLLABUSJemalyn De Guzman Turingan89% (9)

- Fab Hotels Shubham Shinde PDFDocument26 pagesFab Hotels Shubham Shinde PDFRituraj SharmaNo ratings yet

- Rural Banking and Agricultural FinancingDocument17 pagesRural Banking and Agricultural FinancingNilanshi MukherjeeNo ratings yet

- RURAL Banking in India VabibhavDocument63 pagesRURAL Banking in India Vabibhavjyoti raghuvanshiNo ratings yet

- JAB Holding 2011-2021 - 10 Year Investment LetterDocument7 pagesJAB Holding 2011-2021 - 10 Year Investment LetterZerohedge100% (1)

- Economics 5 MCQ C14Document14 pagesEconomics 5 MCQ C14Lindelwe Nene100% (1)

- Coopart Bank Second Plag FinalDocument84 pagesCoopart Bank Second Plag FinalNamrathaNo ratings yet

- Small and Medium Enterprises LoansDocument12 pagesSmall and Medium Enterprises LoansSathishNo ratings yet

- FYP-Home Loan Comparison and Credit RatingDocument67 pagesFYP-Home Loan Comparison and Credit RatingGiridhar NaiduNo ratings yet

- Summer Internship Report On Current Account Facility of Central Bank of IndiaDocument87 pagesSummer Internship Report On Current Account Facility of Central Bank of IndiaGaurav SinghNo ratings yet

- Project On Rural Banking in India 15-01-2023Document74 pagesProject On Rural Banking in India 15-01-2023Praveen ChaudharyNo ratings yet

- A Project Report On "Role of Bajaj Finserv in Consumer Durable Lending "Document38 pagesA Project Report On "Role of Bajaj Finserv in Consumer Durable Lending "Aniket KarnNo ratings yet

- Rashid Solanki Roll No. 294 Bandhan Bank Final Year ProjectDocument60 pagesRashid Solanki Roll No. 294 Bandhan Bank Final Year Projectsarah IsharatNo ratings yet

- To The Study On Basic NabardDocument23 pagesTo The Study On Basic NabardKunal DeoreNo ratings yet

- Idbi BankDocument57 pagesIdbi BankRajVishwakarmaNo ratings yet

- NABARDDocument46 pagesNABARDMahesh Gaddamedi100% (1)

- XX Credit Appraisal Project FinalDocument40 pagesXX Credit Appraisal Project FinalDhaval ShahNo ratings yet

- Cooperative SocietyDocument5 pagesCooperative SocietyKavita SinghNo ratings yet

- A Study On Home Loans - SbiDocument69 pagesA Study On Home Loans - Sbirajesh bathula100% (1)

- Cooperative SocietyDocument4 pagesCooperative SocietyPanav MohindraNo ratings yet

- Micro-Finance Management & Critical Analysis in IndiaDocument72 pagesMicro-Finance Management & Critical Analysis in IndiaAtul MangaleNo ratings yet

- Vehicle Loan Financing by IIIFLDocument69 pagesVehicle Loan Financing by IIIFLKunal GoldmedalistNo ratings yet

- Role of Cooperative Bank in Agricultural PDFDocument12 pagesRole of Cooperative Bank in Agricultural PDFYashodhara BhattNo ratings yet

- Regional Rural BankDocument26 pagesRegional Rural BankVijayeta Nerurkar100% (1)

- A Study On The Mananthavady Urban Co-Operative Society Ltd. No: W 221 A Study On The Mananthavady Urban Co-Operative Society Ltd. No: W 221Document41 pagesA Study On The Mananthavady Urban Co-Operative Society Ltd. No: W 221 A Study On The Mananthavady Urban Co-Operative Society Ltd. No: W 221Wendy BattleNo ratings yet

- Axis BankDocument83 pagesAxis BankSami ZamaNo ratings yet

- Capital Market in India ProjectDocument50 pagesCapital Market in India ProjectNamrataShahaniNo ratings yet

- Shraddha ProjectDocument70 pagesShraddha ProjectAkshay Harekar50% (2)

- Axis Bank ReportDocument99 pagesAxis Bank Reportmudit varshneyNo ratings yet

- Project Report On Credit AppraisalDocument53 pagesProject Report On Credit AppraisalAMYNo ratings yet

- SKDRDP DairyDocument18 pagesSKDRDP DairyrajyalakshmiNo ratings yet

- Rana Internship Report-1Document44 pagesRana Internship Report-1Muhammed Althaf VKNo ratings yet

- 5th Sem ProjectDocument74 pages5th Sem Projectstellastar24No ratings yet

- Origin and Performance of Regional Rural Bank of IndiaDocument13 pagesOrigin and Performance of Regional Rural Bank of IndiaHetvi TankNo ratings yet

- Vaibhav JewellersDocument82 pagesVaibhav JewellersEmpty Minded0% (1)

- Gramin Bank Rular BankingDocument66 pagesGramin Bank Rular BankingSuman KumariNo ratings yet

- All Metabolic Reactions That Use Proteins, Fats, and CarbohydratesDocument32 pagesAll Metabolic Reactions That Use Proteins, Fats, and Carbohydratesshannon c. lewisNo ratings yet

- Summer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaDocument142 pagesSummer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaVismay GharatNo ratings yet

- Vikas Maheshwari 05106Document92 pagesVikas Maheshwari 05106Raju Cool100% (1)

- NBFC FinalDocument100 pagesNBFC FinalDivyangi WaliaNo ratings yet

- The Ayali Kalan Co-Operative Agricultural Multipurpose Society LimitedDocument51 pagesThe Ayali Kalan Co-Operative Agricultural Multipurpose Society LimitedRamandeep Grewal100% (1)

- Finance ProjectDocument14 pagesFinance ProjectASUTOSH MUDULINo ratings yet

- (Markenting) CRM SBICAP SECURITIESDocument73 pages(Markenting) CRM SBICAP SECURITIESsantoshnagane72No ratings yet

- A Study On Credit Risk Management at Karvadi Agricultural Co-Operative Society LimitedDocument76 pagesA Study On Credit Risk Management at Karvadi Agricultural Co-Operative Society LimitedPooja Sirsat100% (1)

- Cosmos Co-Operative Bank: Introducation & HistoryDocument28 pagesCosmos Co-Operative Bank: Introducation & HistoryMahesh DoijodeNo ratings yet

- Human Resoruce Management in The Hotel and Catering Industry.Document65 pagesHuman Resoruce Management in The Hotel and Catering Industry.Onatunji AdigunNo ratings yet

- Farmers' Service SocietyDocument7 pagesFarmers' Service SocietyTapesh Awasthi100% (1)

- JK Bank ShriyaDocument69 pagesJK Bank ShriyaRohit GanjooNo ratings yet

- VC Comparative Analysis of Sbi Icici BankDocument74 pagesVC Comparative Analysis of Sbi Icici BankVishal ChauhanNo ratings yet

- Economics Board ProjectDocument24 pagesEconomics Board ProjecttashaNo ratings yet

- Rawe ReportDocument67 pagesRawe ReportSuruchi KumariNo ratings yet

- Financing To Msme Units - Andhra BankDocument111 pagesFinancing To Msme Units - Andhra BankRavi Kumar100% (1)

- Role of Trade Associations and Self-Help Groups For Promotion of Entreprenuership - DIPIKA JAISWAL (BCH2021078)Document13 pagesRole of Trade Associations and Self-Help Groups For Promotion of Entreprenuership - DIPIKA JAISWAL (BCH2021078)Dipika JaiswalNo ratings yet

- Saraswat BankDocument72 pagesSaraswat Bankaadil shaikhNo ratings yet

- UntitledDocument45 pagesUntitledHYPER X GamingNo ratings yet

- Agricultural LoanDocument62 pagesAgricultural Loanprasad pawleNo ratings yet

- Final Project 0108Document56 pagesFinal Project 0108Shubham DanielNo ratings yet

- Credit Appraisal For Working Capital and Term LoanDocument114 pagesCredit Appraisal For Working Capital and Term LoanAkanksha Kapoor100% (2)

- A Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)Document56 pagesA Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)geetha_kannan32No ratings yet

- Docc Project Report Saath YuvraajDocument22 pagesDocc Project Report Saath YuvraajNikii BaluniNo ratings yet

- The Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalDocument6 pagesThe Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalRATHLOGICNo ratings yet

- Coop e PN 2018 19Document86 pagesCoop e PN 2018 19Ancy RajNo ratings yet

- Seed Tech AssignmentDocument42 pagesSeed Tech AssignmentPratik MogheNo ratings yet

- Seed Tech Pratical ManualDocument31 pagesSeed Tech Pratical ManualPratik MogheNo ratings yet

- Farmer Perception On E-Nam (National Agricultural Market)Document18 pagesFarmer Perception On E-Nam (National Agricultural Market)Pratik MogheNo ratings yet

- Project Report On Apmc-HinganghatDocument33 pagesProject Report On Apmc-HinganghatPratik MogheNo ratings yet

- Cooperative AssignmentDocument21 pagesCooperative AssignmentPratik MogheNo ratings yet

- On Customer SatisfcationDocument41 pagesOn Customer SatisfcationAnkit SoniNo ratings yet

- NCC-TPL-SIL C4 Pre Bid Queries - 1st Set 120419 R1Document12 pagesNCC-TPL-SIL C4 Pre Bid Queries - 1st Set 120419 R1chtrpNo ratings yet

- PCC 2008 NPO QuestionDocument10 pagesPCC 2008 NPO QuestionVaibhav MaheshwariNo ratings yet

- RHB Report Ind - Consumer - Sector Update - 20230306 - RHB Regional ConsumerDocument4 pagesRHB Report Ind - Consumer - Sector Update - 20230306 - RHB Regional ConsumerjovalNo ratings yet

- Undergraduate Project Report TECNO LINK FinalDocument60 pagesUndergraduate Project Report TECNO LINK FinalBontu GirmaNo ratings yet

- 13 CIR VS MARUBENI (2001) G.R. No. 137377Document12 pages13 CIR VS MARUBENI (2001) G.R. No. 137377JanMarkMontedeRamosWongNo ratings yet

- Insurance Fin InclusionDocument17 pagesInsurance Fin InclusionbhavyaNo ratings yet

- Reply-Wesco - FICO AMDocument165 pagesReply-Wesco - FICO AMJit GhoshNo ratings yet

- Accounting Treatment For MudarabahDocument8 pagesAccounting Treatment For MudarabahhamoussaibNo ratings yet

- Basel Credit Risk Correlation 0.12Document30 pagesBasel Credit Risk Correlation 0.12rahulNo ratings yet

- Introduction To Economy of PakistanDocument7 pagesIntroduction To Economy of PakistanAsim MinhasNo ratings yet

- Finance Viva Final SemesterDocument3 pagesFinance Viva Final SemesterSharfuddin ZishanNo ratings yet

- Summer Internship Report On Financial Analysis of Wipro LTDDocument77 pagesSummer Internship Report On Financial Analysis of Wipro LTDSatyam ShuklaNo ratings yet

- Fin321 Final Project Report BarcDocument21 pagesFin321 Final Project Report Barcapi-490659565No ratings yet

- Unit - 2 - Electronic Payment SystemDocument67 pagesUnit - 2 - Electronic Payment Systemvisdag100% (2)

- PNB Savings Bank Annual Report 2017 PDFDocument132 pagesPNB Savings Bank Annual Report 2017 PDFWil PerniaNo ratings yet

- B 1 Bank TransactionsDocument16 pagesB 1 Bank TransactionsMahima SherigarNo ratings yet

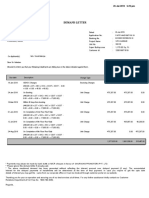

- Demand LetterDocument2 pagesDemand LetterHimanshu RantiyaNo ratings yet

- Terms and Conditions For HBL Conventional AccountsDocument2 pagesTerms and Conditions For HBL Conventional Accountsfaisal_ahsan7919No ratings yet

- FRM Practice Exam From EdupristineDocument52 pagesFRM Practice Exam From EdupristineAnish Jagdish LakhaniNo ratings yet

- Pbe EBANK001Document15 pagesPbe EBANK001UNIT EPID PKK KOTA KINABALUNo ratings yet

- IMO Publications Catalogue March 2018Document157 pagesIMO Publications Catalogue March 2018VARUN AGARWAL100% (1)

- FICHTNER 110KV Tender Enquiry Document SWYD PDFDocument364 pagesFICHTNER 110KV Tender Enquiry Document SWYD PDFS ManoharNo ratings yet

- Economic Survey Volume I Complete PDFDocument298 pagesEconomic Survey Volume I Complete PDFAbhishek KumarNo ratings yet

- Demonetization Impact Over Banking Loans & Advances-A Case StudyDocument16 pagesDemonetization Impact Over Banking Loans & Advances-A Case Studyom handeNo ratings yet

- 7 Market Risk - Mitigation and Regulatory RequirementsDocument20 pages7 Market Risk - Mitigation and Regulatory RequirementsThineshNo ratings yet

- Table 141: India'S Overall Balance of Payments - RupeesDocument2 pagesTable 141: India'S Overall Balance of Payments - Rupeesmahbobullah rahmaniNo ratings yet