You might also like

- Tutorial Report Enterprise Design and Analysis Financial ModuleDocument15 pagesTutorial Report Enterprise Design and Analysis Financial Modulealma millaniaNo ratings yet

- Financial Tables CONAIDDocument11 pagesFinancial Tables CONAIDCarl Ammiel P. LapureNo ratings yet

- Chapter 5 FSDocument17 pagesChapter 5 FSMarisa CaraganNo ratings yet

- RevisionDocument16 pagesRevisionKaycee C. San DiegoNo ratings yet

- Project Report2Document6 pagesProject Report2bhanuNo ratings yet

- Management Accounting Study NotesDocument39 pagesManagement Accounting Study NotesAlexander TrovatoNo ratings yet

- IV. Financial Study A. Project CostDocument13 pagesIV. Financial Study A. Project CostKeil Joshua VerdaderoNo ratings yet

- Final Proyectos EJEMPLODocument21 pagesFinal Proyectos EJEMPLOfransheska GallegosNo ratings yet

- E - Logistics: Profile No.: 151 NIC Code:82110Document9 pagesE - Logistics: Profile No.: 151 NIC Code:82110aefewNo ratings yet

- Online Catering Home Delivery ServiceDocument6 pagesOnline Catering Home Delivery ServiceMansi MistryNo ratings yet

- Cyber Café: Profile No.: 144 NIC Code: 63992Document10 pagesCyber Café: Profile No.: 144 NIC Code: 63992Krishnan NamboothiriNo ratings yet

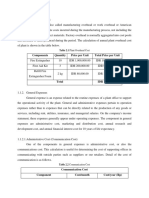

- Components Quantity Price Per Unit Total Price Per Unit: Table 2.1 Plant Overhead CostDocument4 pagesComponents Quantity Price Per Unit Total Price Per Unit: Table 2.1 Plant Overhead CostFaldy FariskiNo ratings yet

- Cyber Café and Xerox Lamination: 4. Industry Look Out and TrendsDocument11 pagesCyber Café and Xerox Lamination: 4. Industry Look Out and Trendspuja sharmaNo ratings yet

- Cyber Cafe and Back Office ServicesDocument11 pagesCyber Cafe and Back Office Services124swadeshi0% (1)

- Computer Training Institute: Project Report ofDocument9 pagesComputer Training Institute: Project Report ofEMMANUEL TV INDIANo ratings yet

- Cyber Café and Xerox Lamination: Profile No.: 143 NIC Code: 63992Document11 pagesCyber Café and Xerox Lamination: Profile No.: 143 NIC Code: 63992Shivam SyalNo ratings yet

- Feasibility StudyDocument19 pagesFeasibility StudyBayu IndraaNo ratings yet

- Computer Training Institute: Profile No.: 2 NIC Code: 62099Document6 pagesComputer Training Institute: Profile No.: 2 NIC Code: 62099nagendra80200No ratings yet

- Maintenance and Other Operating ExpensesDocument6 pagesMaintenance and Other Operating ExpensesRenalyn Mae BaysaNo ratings yet

- ACFrOgBR3zmYIfST M04WW9MOxJsCDOY8ij K10c8jFzoDesUe4hmgtwitQThRfZx9zgdfBbbfAPg9fYbdGwDnuwcmqyJhSe8wLpgC1wkMIV6jGps45E YC2ro8e WakacYQ6ARdjCeTf76iCHtdDocument6 pagesACFrOgBR3zmYIfST M04WW9MOxJsCDOY8ij K10c8jFzoDesUe4hmgtwitQThRfZx9zgdfBbbfAPg9fYbdGwDnuwcmqyJhSe8wLpgC1wkMIV6jGps45E YC2ro8e WakacYQ6ARdjCeTf76iCHtdMario FiskaNo ratings yet

- June2023 - Dec 2020 FinanceDocument105 pagesJune2023 - Dec 2020 FinancebinuNo ratings yet

- Suggested CAP II Group II June 2023Document61 pagesSuggested CAP II Group II June 2023pratyushmudbhari340No ratings yet

- Fs FinalDocument14 pagesFs FinalKringlelyn Fikan GandamNo ratings yet

- SK AB FormatDocument39 pagesSK AB FormatAnn YanaNo ratings yet

- E-Retail Outlet For Ready Made GarmentsDocument11 pagesE-Retail Outlet For Ready Made Garmentsrubi laariNo ratings yet

- Online Shopping Cart ApplicationDocument10 pagesOnline Shopping Cart ApplicationYESHUDAS JIVTODENo ratings yet

- Haldar Grocery Project-fINALDocument9 pagesHaldar Grocery Project-fINALCA Devangaraj GogoiNo ratings yet

- Computer Training InstituteDocument10 pagesComputer Training InstituteaefewNo ratings yet

- Resource Booklet Jun 2021Document8 pagesResource Booklet Jun 2021ElenaNo ratings yet

- Cyber CafeDocument6 pagesCyber CafeAjeet Aman SinghNo ratings yet

- Cyber Café and Xerox Lamination: Profile No.: 6 NIC Code: 63992Document6 pagesCyber Café and Xerox Lamination: Profile No.: 6 NIC Code: 63992EdigitalNo ratings yet

- E Retail Outlet For GarmentsDocument11 pagesE Retail Outlet For GarmentsAEBEE SIMONNo ratings yet

- Uts 2021 2Document7 pagesUts 2021 2Wahyudi SyaputraNo ratings yet

- Sample SEP Project ProposalDocument110 pagesSample SEP Project ProposalTonish LangthasaNo ratings yet

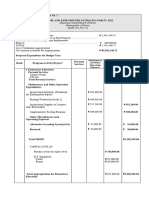

- The Required Initial Disbursement That The Business Needs To Facilitate The Proposed Project Will Be P 11,830,562.58. The Itemization Is As Shown in Table 22Document16 pagesThe Required Initial Disbursement That The Business Needs To Facilitate The Proposed Project Will Be P 11,830,562.58. The Itemization Is As Shown in Table 22Lhara Mae ReyesNo ratings yet

- Model Project Profile On Plastic Bottle (Pcbi)Document2 pagesModel Project Profile On Plastic Bottle (Pcbi)sivanagendrarao beharabhargavaNo ratings yet

- Ap A2.1 - FinalDocument7 pagesAp A2.1 - FinalLuna LeeNo ratings yet

- Web Design Service CentreDocument6 pagesWeb Design Service CentreRahulNo ratings yet

- FS CHAP 5 TABLE Finaaaaal NaDocument6 pagesFS CHAP 5 TABLE Finaaaaal NaIvan SalvadorNo ratings yet

- Bindi Manufacturing UnitDocument2 pagesBindi Manufacturing Unitsunsp52No ratings yet

- Zaman Nissa Kudumbasree NorkaDocument4 pagesZaman Nissa Kudumbasree NorkaJESSIS BUSINESS SOLUTIONSNo ratings yet

- IAR - FIT Peshawar 2019Document5 pagesIAR - FIT Peshawar 2019Fouzia NazarNo ratings yet

- CA-Midterm-N IE-2019-2-20201Document2 pagesCA-Midterm-N IE-2019-2-20201Grace BornengNo ratings yet

- CA-Midterm-N IE-2019-2-20201Document2 pagesCA-Midterm-N IE-2019-2-20201Grace BornengNo ratings yet

- KotureshwaraDocument9 pagesKotureshwaraVeerabhadreshwar Online CenterNo ratings yet

- Introduction To Accounting and Finance Unit Code Aaf005-1 Main Exam Semester 3 2020/21Document7 pagesIntroduction To Accounting and Finance Unit Code Aaf005-1 Main Exam Semester 3 2020/21Chulbul PandeyNo ratings yet

- Budget InformationDocument10 pagesBudget InformationIsabella BattiataNo ratings yet

- ROYAL SCANS AND DIAGNOSTICS - CompressedDocument23 pagesROYAL SCANS AND DIAGNOSTICS - CompressedAegan VetrinarayananNo ratings yet

- Bakery ProjectsDocument2 pagesBakery ProjectsfasmekbakerNo ratings yet

- Jawaban Tugas 2 AIK - EKSI4204 - Edward Jose 041010572Document4 pagesJawaban Tugas 2 AIK - EKSI4204 - Edward Jose 041010572EdwardJoseNo ratings yet

- Bakery Products 13 LakhDocument5 pagesBakery Products 13 LakhRitesh SinghNo ratings yet

- DroneTech Engineering CostsDocument16 pagesDroneTech Engineering CostsMarceloNo ratings yet

- Project Profile On Decorative GlasswareDocument2 pagesProject Profile On Decorative Glasswarepuja sharmaNo ratings yet

- E Directory Project ReportDocument11 pagesE Directory Project ReportVidhimanya Chamber of Commerce and IndustryNo ratings yet

- Beauty Parlour ShopDocument4 pagesBeauty Parlour Shopgdmurugan2k7No ratings yet

- Cyber Cafe Xerox LaminationDocument7 pagesCyber Cafe Xerox LaminationRatna KarNo ratings yet

- Intermediate Accounting ExamDocument6 pagesIntermediate Accounting ExamPISONANTA KRISETIANo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- 2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportFrom Everand2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportNo ratings yet

- Estimating the Job Creation Impact of Development AssistanceFrom EverandEstimating the Job Creation Impact of Development AssistanceNo ratings yet

- Business Performance Management (BPM) : The Architecture of Business IntelligenceDocument23 pagesBusiness Performance Management (BPM) : The Architecture of Business Intelligencealma millaniaNo ratings yet

- Understanding Business IntelligenceDocument18 pagesUnderstanding Business Intelligencealma millaniaNo ratings yet

- Business Intelligence: A Quick Peek: Winda Nur CahyoDocument34 pagesBusiness Intelligence: A Quick Peek: Winda Nur Cahyoalma millaniaNo ratings yet

- Alma Fitria Milania (18522215) - Assignment - Financial Analysis Using Power BIDocument5 pagesAlma Fitria Milania (18522215) - Assignment - Financial Analysis Using Power BIalma millaniaNo ratings yet

- Meet 03 - 04Document34 pagesMeet 03 - 04alma millaniaNo ratings yet

- Turning Data Into Art: Overview of Data VisualizationDocument17 pagesTurning Data Into Art: Overview of Data Visualizationalma millaniaNo ratings yet

- Tutorial Report Enterprise Design and Analysis Introduction and Marketing ModuleDocument19 pagesTutorial Report Enterprise Design and Analysis Introduction and Marketing Modulealma millaniaNo ratings yet

- Report Modul 3 IpDocument15 pagesReport Modul 3 Ipalma millaniaNo ratings yet

- Supplier Development at SWPDocument82 pagesSupplier Development at SWPalma millaniaNo ratings yet

- Evaluation of Procurement Processes and Its Operational Performance in The Public Sector of Ghana: A Case Study of Komfo Anokye Teaching Hospital and Kumasi PolytechnicDocument12 pagesEvaluation of Procurement Processes and Its Operational Performance in The Public Sector of Ghana: A Case Study of Komfo Anokye Teaching Hospital and Kumasi Polytechnicalma millaniaNo ratings yet

- Procurement Practices in Project Based Manufacturing EnvironmentsDocument7 pagesProcurement Practices in Project Based Manufacturing Environmentsalma millaniaNo ratings yet

- Procurement Process Analysis Using Process Mining in Cement Manufacturing Company (Case Study PT. Semen Indonesia Persero, TBK)Document6 pagesProcurement Process Analysis Using Process Mining in Cement Manufacturing Company (Case Study PT. Semen Indonesia Persero, TBK)alma millaniaNo ratings yet

- Procurement Practices in Project Based Manufacturing EnvironmentsDocument7 pagesProcurement Practices in Project Based Manufacturing Environmentsalma millaniaNo ratings yet

- Koh Et Al 2012 ReportDocument64 pagesKoh Et Al 2012 Reportalma millaniaNo ratings yet

- Procurement Process Analysis Using Process Mining in Cement Manufacturing Company (Case Study PT. Semen Indonesia Persero, TBK)Document6 pagesProcurement Process Analysis Using Process Mining in Cement Manufacturing Company (Case Study PT. Semen Indonesia Persero, TBK)alma millaniaNo ratings yet

- Tutorial Report Physiology and Work Measurement StopwatchDocument29 pagesTutorial Report Physiology and Work Measurement Stopwatchalma millaniaNo ratings yet

- Tutorial Report Physiology and Work Measurement Work PostureDocument29 pagesTutorial Report Physiology and Work Measurement Work Posturealma millaniaNo ratings yet

- Tutorial Report Physiology and Work Measurement Work PhysiologyDocument16 pagesTutorial Report Physiology and Work Measurement Work Physiologyalma millaniaNo ratings yet

- Supplier Development at SWPDocument82 pagesSupplier Development at SWPalma millaniaNo ratings yet

- Evaluation of Procurement Processes and Its Operational Performance in The Public Sector of Ghana: A Case Study of Komfo Anokye Teaching Hospital and Kumasi PolytechnicDocument12 pagesEvaluation of Procurement Processes and Its Operational Performance in The Public Sector of Ghana: A Case Study of Komfo Anokye Teaching Hospital and Kumasi Polytechnicalma millaniaNo ratings yet

- Tutorial Report Physiology and Work Measurement BiomechanicsDocument17 pagesTutorial Report Physiology and Work Measurement Biomechanicsalma millaniaNo ratings yet

- Tutorial Report Physiology and Work Measurement Mental WorkloadDocument18 pagesTutorial Report Physiology and Work Measurement Mental Workloadalma millaniaNo ratings yet

- ch01 en IbmDocument57 pagesch01 en IbmDewi Chan曾琦珍No ratings yet

- Saln 2016 FormDocument3 pagesSaln 2016 FormJOHN100% (3)

- Derivative Market in India by ICICI, SBI & Yes Bank & Its BehaviorDocument90 pagesDerivative Market in India by ICICI, SBI & Yes Bank & Its BehaviorChandan SrivastavaNo ratings yet

- Appendix 32 DVDocument1 pageAppendix 32 DVJohn-Rey ManzanoNo ratings yet

- 6 Disposal of Fixed AssetsDocument6 pages6 Disposal of Fixed Assetsశ్రీనివాసకిరణ్కుమార్చతుర్వేదులNo ratings yet

- Chapter One: The Principles of Lending and Lending BasicsDocument23 pagesChapter One: The Principles of Lending and Lending BasicsSamuel サム VargheseNo ratings yet

- Ethics CaseDocument38 pagesEthics Casemeochip21No ratings yet

- Sti ImfDocument88 pagesSti ImfPema DorjiNo ratings yet

- Sources of Capital, Informal Risk Capital & Venture CapitalDocument29 pagesSources of Capital, Informal Risk Capital & Venture CapitalDivyesh Gandhi0% (1)

- Monthly Statement: This Month's SummaryDocument4 pagesMonthly Statement: This Month's SummaryTushar AnandNo ratings yet

- Reading 24 - Equity Valuation - Applications and ProcessesDocument5 pagesReading 24 - Equity Valuation - Applications and ProcessesJuan MatiasNo ratings yet

- Effect of Service Transactions On Accounting ElementsDocument11 pagesEffect of Service Transactions On Accounting ElementsREACTION COPNo ratings yet

- 24 02 2018 - ElectricityBillDocument1 page24 02 2018 - ElectricityBillAditya TiwariNo ratings yet

- IBPS Clerk Interview QuestionsDocument4 pagesIBPS Clerk Interview QuestionsSai KaneNo ratings yet

- A187844 Aiman Zakwan Tutorial 4Document1 pageA187844 Aiman Zakwan Tutorial 4aiman ZakwanNo ratings yet

- Schedule Fees 2021 2022Document2 pagesSchedule Fees 2021 2022Marneil Daevid ArevaloNo ratings yet

- Buying and Selling Securities Buying and Selling Securities: Fundamentals InvestmentsDocument39 pagesBuying and Selling Securities Buying and Selling Securities: Fundamentals InvestmentsadillawaNo ratings yet

- Income Statement FormatDocument2 pagesIncome Statement FormatShruti MohanNo ratings yet

- Pubali July - 2019 - FinalDocument66 pagesPubali July - 2019 - Finalzannatul zoyaNo ratings yet

- CACell Intermediate Account Full Book-201-250Document50 pagesCACell Intermediate Account Full Book-201-250kalyanikamineniNo ratings yet

- Chapter 11 - Sources of CapitalDocument21 pagesChapter 11 - Sources of CapitalArman100% (1)

- Jun2023Document15 pagesJun2023Piyush NagarNo ratings yet

- Distressed Debt Investing: Wisdom From Seth KlarmanDocument4 pagesDistressed Debt Investing: Wisdom From Seth Klarmanjt322No ratings yet

- Correcting EntriesDocument2 pagesCorrecting EntriesCriziel Ann LealNo ratings yet

- 2018 - Mock AnswerDocument3 pages2018 - Mock AnswerNghiem Nguyen VinhNo ratings yet

- InsuranceDocument188 pagesInsurancetura kedirNo ratings yet

- What Is Portfolio ManagementDocument4 pagesWhat Is Portfolio Managementsakpal_smitaNo ratings yet

- Q2 Week 8 - ADM ModuleDocument4 pagesQ2 Week 8 - ADM ModuleCathleenbeth MorialNo ratings yet

- Fabm 1-PTDocument10 pagesFabm 1-PTClay MaaliwNo ratings yet