You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- United States Post Office Creditor Bond 410760000/ 2025923Document14 pagesUnited States Post Office Creditor Bond 410760000/ 2025923akil kemnebi easley el100% (8)

- The Law of Trusts 3 - e - Gillese, Eileen E.Document225 pagesThe Law of Trusts 3 - e - Gillese, Eileen E.Valentine Gurfinkel100% (6)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 1099 OID CLASS - ExtraformsDocument218 pages1099 OID CLASS - Extraformspatiosmamu100% (3)

- Ill Wind in FriezfordDocument36 pagesIll Wind in FriezfordNick KNo ratings yet

- FMA Informative Issue184Document11 pagesFMA Informative Issue184Nick KNo ratings yet

- Agency, Trust & Partnership: E.G. SPA & Regular AuthorizationsDocument16 pagesAgency, Trust & Partnership: E.G. SPA & Regular AuthorizationsKingNo ratings yet

- Fiduciaries DutiesDocument95 pagesFiduciaries DutiesDrjKmrNo ratings yet

- Banking Memory AidDocument10 pagesBanking Memory AidEdz Votefornoymar Del RosarioNo ratings yet

- GR 163553, GR 160488Document8 pagesGR 163553, GR 160488ronhuman14100% (1)

- KYC Norms Full ProjectDocument72 pagesKYC Norms Full ProjectGaurav Golecha100% (1)

- Commercial BanksDocument37 pagesCommercial Banksshanpearl100% (2)

- K10. MIAA vs. Court of Appeals - DigestDocument2 pagesK10. MIAA vs. Court of Appeals - DigestCarla Mae MartinezNo ratings yet

- IncomeTaxation Banggawan2019 Ch13BDocument9 pagesIncomeTaxation Banggawan2019 Ch13BNoreen Ledda0% (2)

- Quarantine Final Exam 2020 (SET A)Document3 pagesQuarantine Final Exam 2020 (SET A)The ApprenticeNo ratings yet

- Australiansuper: Product Disclosure StatementDocument32 pagesAustraliansuper: Product Disclosure StatementNick KNo ratings yet

- PDS SuperOptionsDocument32 pagesPDS SuperOptionsNick KNo ratings yet

- GHD Superannuation Plan: Product Disclosure StatementDocument32 pagesGHD Superannuation Plan: Product Disclosure StatementNick KNo ratings yet

- Personal Plan: Product Disclosure StatementDocument28 pagesPersonal Plan: Product Disclosure StatementNick KNo ratings yet

- Australiansuper Select: Product Disclosure StatementDocument16 pagesAustraliansuper Select: Product Disclosure StatementNick KNo ratings yet

- Life Insurance PdsDocument43 pagesLife Insurance PdsNick KNo ratings yet

- PDS PublicSectorDocument16 pagesPDS PublicSectorNick KNo ratings yet

- AU-Vanguard Managed Funds-Reference GuideDocument19 pagesAU-Vanguard Managed Funds-Reference GuideNick KNo ratings yet

- Generations Personal Super and Pension Additional InformationDocument22 pagesGenerations Personal Super and Pension Additional InformationNick KNo ratings yet

- TTR Income: Product Disclosure StatementDocument52 pagesTTR Income: Product Disclosure StatementNick KNo ratings yet

- Generations Super and Pension Product Disclosure StatementDocument39 pagesGenerations Super and Pension Product Disclosure StatementNick KNo ratings yet

- AU-Unitholder-notice-Vanguard AMMA Tax Statement GlossaryDocument4 pagesAU-Unitholder-notice-Vanguard AMMA Tax Statement GlossaryNick KNo ratings yet

- Woolworths Supermarkets Agreement 2018 Final 02.10.2018Document68 pagesWoolworths Supermarkets Agreement 2018 Final 02.10.2018Nick KNo ratings yet

- Medtronic MM780G New Insulin Pump Order FormDocument4 pagesMedtronic MM780G New Insulin Pump Order FormNick KNo ratings yet

- AU-Vanguard Personal Investor Guide Part ADocument28 pagesAU-Vanguard Personal Investor Guide Part ANick KNo ratings yet

- AU-Vanguard Personal Investor Investment MenuDocument12 pagesAU-Vanguard Personal Investor Investment MenuNick KNo ratings yet

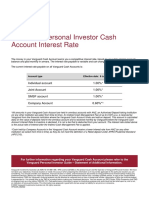

- AU-Vanguard Personal Investor-Cash Account Interest RateDocument1 pageAU-Vanguard Personal Investor-Cash Account Interest RateNick KNo ratings yet

- Epic Rogue of Seven Sneak Attacks A Round A Creature (3Document4 pagesEpic Rogue of Seven Sneak Attacks A Round A Creature (3Nick KNo ratings yet

- Info Card 2016-17Document12 pagesInfo Card 2016-17Nick KNo ratings yet

- Common Riverbank Weeds Lower Hawk Nepean BookletDocument68 pagesCommon Riverbank Weeds Lower Hawk Nepean BookletNick KNo ratings yet

- Richmond Bridge Duplication and Traffic Improvements: Frequently Asked QuestionsDocument5 pagesRichmond Bridge Duplication and Traffic Improvements: Frequently Asked QuestionsNick KNo ratings yet

- Richmond Bridge Duplication and Traffic Improvements: Community Update - Route Investigation November 2019Document5 pagesRichmond Bridge Duplication and Traffic Improvements: Community Update - Route Investigation November 2019Nick KNo ratings yet

- Trinidad vs. ImsonDocument5 pagesTrinidad vs. ImsonVince Llamazares LupangoNo ratings yet

- CasesDocument32 pagesCasesdollyccruzNo ratings yet

- Juan VS YapDocument4 pagesJuan VS YapTAU MU OFFICIALNo ratings yet

- 2019MCNo07 Guidelines On The Establishment of A One Person CorporationDocument19 pages2019MCNo07 Guidelines On The Establishment of A One Person Corporationdominador faurilloNo ratings yet

- Stopper v. Kestel, 4th Cir. (2001)Document5 pagesStopper v. Kestel, 4th Cir. (2001)Scribd Government DocsNo ratings yet

- NBKC Memo Supporting Motion To DismissDocument35 pagesNBKC Memo Supporting Motion To DismissChris HerzecaNo ratings yet

- Taxation On Estates and TrustsDocument31 pagesTaxation On Estates and TrustsAndrea Renice S. FerriolNo ratings yet

- The Maharashtra Metropolitan Region Development Authority Act, 2016Document21 pagesThe Maharashtra Metropolitan Region Development Authority Act, 2016Srishty PandeyNo ratings yet

- MOJ0217.1E OCT21 Maori Land TrustsDocument3 pagesMOJ0217.1E OCT21 Maori Land TrustsmcrobertspatsyNo ratings yet

- CA Request For Beneficiary StatementDocument2 pagesCA Request For Beneficiary StatementbombdocNo ratings yet

- Exercise 2 Estate Tax pt1.5Document4 pagesExercise 2 Estate Tax pt1.5Maristella GatonNo ratings yet

- W302 Tma03Document6 pagesW302 Tma03Freddie CookNo ratings yet

- Chapter 03 - Non-Bank Financial InstitutionsDocument18 pagesChapter 03 - Non-Bank Financial InstitutionsKhang Tran DuyNo ratings yet

- 2nd ARC Social Capital @cse - UpdatesDocument122 pages2nd ARC Social Capital @cse - UpdatesIslavath BalajiNo ratings yet

- Pok (PL PDocument5 pagesPok (PL PCristopher ReyesNo ratings yet

- EDMDocument10 pagesEDMDhruvil ShahNo ratings yet

- Form No. 34A: Application For A Certificate Under Section 230A (1) of The Income - Tax Act, 1961Document4 pagesForm No. 34A: Application For A Certificate Under Section 230A (1) of The Income - Tax Act, 1961Movie DhamakaNo ratings yet

- CIR v. CA, 207 SCRA 487 (1992) PDFDocument5 pagesCIR v. CA, 207 SCRA 487 (1992) PDFsbce14No ratings yet