You might also like

- Insurance BasicsDocument25 pagesInsurance BasicsGautam SandeepNo ratings yet

- PCL Chap 2 en Ca PDFDocument45 pagesPCL Chap 2 en Ca PDFRenso Ramirez JimenezNo ratings yet

- Understanding Insurance BasicsDocument25 pagesUnderstanding Insurance BasicsTewodros TeshomeNo ratings yet

- A Beginner's Guide to Disability Insurance Claims in Canada: How to Apply for and Win Payment of Disability Insurance Benefits, Even After a Denial or Unsuccessful AppealFrom EverandA Beginner's Guide to Disability Insurance Claims in Canada: How to Apply for and Win Payment of Disability Insurance Benefits, Even After a Denial or Unsuccessful AppealNo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- Safe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesFrom EverandSafe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- FMA Informative Issue184Document11 pagesFMA Informative Issue184Nick KNo ratings yet

- Compensation Policy AuthorizationDocument20 pagesCompensation Policy Authorizationshruti tripathiNo ratings yet

- Canara HSBC Life Insurance Premium ReceiptDocument1 pageCanara HSBC Life Insurance Premium Receiptyogesh bafnaNo ratings yet

- Asteron Life CompleteDocument108 pagesAsteron Life CompleteLife Insurance AustraliaNo ratings yet

- Week 5 Individual Assignment Individual Income Taxation Exercise 1202 CLWTAXN K35 TAXATIONDocument15 pagesWeek 5 Individual Assignment Individual Income Taxation Exercise 1202 CLWTAXN K35 TAXATIONVan TisbeNo ratings yet

- Rest Super Insurance Guide PDFDocument60 pagesRest Super Insurance Guide PDFnimai.nitai1No ratings yet

- Macquarie FutureWiseDocument80 pagesMacquarie FutureWiseLife Insurance AustraliaNo ratings yet

- FWD Term Life Plus insurance policy contract overviewDocument49 pagesFWD Term Life Plus insurance policy contract overviewfelixkerNo ratings yet

- TAL Accelerated Protection PDSDocument44 pagesTAL Accelerated Protection PDSLife Insurance AustraliaNo ratings yet

- InsuranceGuide IndustryDocument36 pagesInsuranceGuide IndustryAntoine Nabil ZakiNo ratings yet

- 07937assure - Ci - BrochureDocument6 pages07937assure - Ci - Brochurebasantjain12345No ratings yet

- Select Membership Handbook Oct 2020Document68 pagesSelect Membership Handbook Oct 2020Ola ANo ratings yet

- QM838-0421 Motorcycle Insurance PDS (Web)Document52 pagesQM838-0421 Motorcycle Insurance PDS (Web)JasonNo ratings yet

- InsuranceGuide IndustryDocument36 pagesInsuranceGuide Industryjim STAMNo ratings yet

- TandCs - ZurichDocument32 pagesTandCs - ZurichskylerboodieNo ratings yet

- Personal Watercraft Insurance Product Disclosure StatementDocument40 pagesPersonal Watercraft Insurance Product Disclosure Statementmark georgeNo ratings yet

- 0cksmlfsdd01v02 Beagle01 s5 Aprd 130522lfsdv002Document9 pages0cksmlfsdd01v02 Beagle01 s5 Aprd 130522lfsdv002JeniferNo ratings yet

- Product Summary FOR Group Livingcare Insurance (Acceleration Benefit)Document3 pagesProduct Summary FOR Group Livingcare Insurance (Acceleration Benefit)Axel KruseNo ratings yet

- Key Features DocumentDocument25 pagesKey Features DocumentPectro BiotechNo ratings yet

- CitibankOneTrip DLDocument42 pagesCitibankOneTrip DLsamlanny97No ratings yet

- SBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness TooDocument2 pagesSBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness ToobpshuNo ratings yet

- Assignment Cover Page: Course Code Course TitleDocument5 pagesAssignment Cover Page: Course Code Course TitleMD FySLNo ratings yet

- Flexible Protection BrochureDocument24 pagesFlexible Protection Brochureslimm.No ratings yet

- Scti International Student PD 01jul19Document38 pagesScti International Student PD 01jul19Rianovel MareNo ratings yet

- OnePath OneCare Life CoverDocument108 pagesOnePath OneCare Life CoverGosselink12No ratings yet

- INSURANCE FOR LIFE'S UNEXPECTED MOMENTSDocument40 pagesINSURANCE FOR LIFE'S UNEXPECTED MOMENTShaiz haizNo ratings yet

- Whole of Life Insurance+: Policy SummaryDocument16 pagesWhole of Life Insurance+: Policy SummaryChristos YerolemouNo ratings yet

- Specified Illness Definitions GuideDocument46 pagesSpecified Illness Definitions GuideRaja Nur Atiqah Hanim R Mohamad FaudziNo ratings yet

- Life Insurance PDSDocument2 pagesLife Insurance PDSAkmal HelmiNo ratings yet

- IPru Sarv Jana Suraksha BrochureDocument6 pagesIPru Sarv Jana Suraksha BrochureyesindiacanngoNo ratings yet

- Coles Motor PDS 300813Document33 pagesColes Motor PDS 300813Turab MominNo ratings yet

- Accidental Death & Serious Injury Cover ExplainedDocument20 pagesAccidental Death & Serious Injury Cover ExplainedTomato GreenNo ratings yet

- Unit 2 Health Insurance ProductsDocument25 pagesUnit 2 Health Insurance ProductsShivam YadavNo ratings yet

- Protection Planning 2013Document28 pagesProtection Planning 2013JessNo ratings yet

- Scti Visiting New Zealand PD 01aug19Document34 pagesScti Visiting New Zealand PD 01aug19chinmay.qsrNo ratings yet

- Health Insurance 12 Points Check ListDocument3 pagesHealth Insurance 12 Points Check ListmcsrNo ratings yet

- INSURANCE POLICIES AND STRATEGIES GUIDEDocument40 pagesINSURANCE POLICIES AND STRATEGIES GUIDEIshaNo ratings yet

- Corporate Chanakya Successful Management The Chanakya WaysDocument60 pagesCorporate Chanakya Successful Management The Chanakya WaysRaza OshimNo ratings yet

- ICICI Pru Iprotect Smart Illustrated Brochure PDFDocument60 pagesICICI Pru Iprotect Smart Illustrated Brochure PDFDhrubajyoti DattaNo ratings yet

- الوثائق المطلوبة للمعاملاتDocument26 pagesالوثائق المطلوبة للمعاملاتPeterbb HelmanNo ratings yet

- HealthDocument68 pagesHealthKvvPrasadNo ratings yet

- Life InsuranceDocument26 pagesLife Insurancevivek kant100% (1)

- QM3098-0513 Combined Annual Cargo Policy - 22 08 13 - WebDocument33 pagesQM3098-0513 Combined Annual Cargo Policy - 22 08 13 - WebPeter MuchoraNo ratings yet

- Iicci PruDocument60 pagesIicci PruCA Manoj GuptaNo ratings yet

- Terms of Business - For ConsumersDocument8 pagesTerms of Business - For ConsumersMădălin Gabriel IgnișcaNo ratings yet

- Silver Health BrochureDocument2 pagesSilver Health BrochureSandeep GhosthNo ratings yet

- Insurance in Your Super Member Number: 600318930Document6 pagesInsurance in Your Super Member Number: 600318930Eggy PalangatNo ratings yet

- 0873 Yourlifeplan Ta KFDocument8 pages0873 Yourlifeplan Ta KFmails4vipsNo ratings yet

- Pds BuildingDocument60 pagesPds BuildingJohnNo ratings yet

- Family Income Benefit Key FactsDocument8 pagesFamily Income Benefit Key FactsPatrick BoydNo ratings yet

- Aalpw 1220Document21 pagesAalpw 1220David SantosNo ratings yet

- Life Insurance Policy DocumentDocument24 pagesLife Insurance Policy DocumentDev D-starNo ratings yet

- Debate 51 ANZDocument27 pagesDebate 51 ANZKelly J. (Lady Grey)No ratings yet

- Bajaj Allianz Super CashGain Insurance Plan SummaryDocument2 pagesBajaj Allianz Super CashGain Insurance Plan SummaryElangovan PurushothamanNo ratings yet

- Aviva i-Life Secure Provides Regular Income for 15 YearsDocument1 pageAviva i-Life Secure Provides Regular Income for 15 YearsPinal JEngineerNo ratings yet

- Analysis of Indian Insurance IndustryDocument32 pagesAnalysis of Indian Insurance Industrymayur_rughaniNo ratings yet

- Health InsuranceDocument11 pagesHealth InsurancedishaNo ratings yet

- Insurance and Banking NotesDocument21 pagesInsurance and Banking NotesIsha ParwaniNo ratings yet

- Australiansuper: Product Disclosure StatementDocument32 pagesAustraliansuper: Product Disclosure StatementNick KNo ratings yet

- PDS SuperOptionsDocument32 pagesPDS SuperOptionsNick KNo ratings yet

- PDS PublicSectorDocument16 pagesPDS PublicSectorNick KNo ratings yet

- GHD Superannuation Plan: Product Disclosure StatementDocument32 pagesGHD Superannuation Plan: Product Disclosure StatementNick KNo ratings yet

- AustralianSuper PDS - Everything You Need to KnowDocument16 pagesAustralianSuper PDS - Everything You Need to KnowNick KNo ratings yet

- TTR Income: Product Disclosure StatementDocument52 pagesTTR Income: Product Disclosure StatementNick KNo ratings yet

- AU-Vanguard Guide To Your AMMA Tax StatementDocument8 pagesAU-Vanguard Guide To Your AMMA Tax StatementNick KNo ratings yet

- Generations Personal Super and Pension Additional InformationDocument22 pagesGenerations Personal Super and Pension Additional InformationNick KNo ratings yet

- Personal Plan: Product Disclosure StatementDocument28 pagesPersonal Plan: Product Disclosure StatementNick KNo ratings yet

- AU-Vanguard Personal Investor Investment MenuDocument12 pagesAU-Vanguard Personal Investor Investment MenuNick KNo ratings yet

- Generations Super and Pension Product Disclosure StatementDocument39 pagesGenerations Super and Pension Product Disclosure StatementNick KNo ratings yet

- IAccess Investment OptionsDocument20 pagesIAccess Investment OptionsNick KNo ratings yet

- Info Card 2016-17Document12 pagesInfo Card 2016-17Nick KNo ratings yet

- AU-Vanguard Managed Funds-Reference GuideDocument19 pagesAU-Vanguard Managed Funds-Reference GuideNick KNo ratings yet

- AU-Unitholder-notice-Vanguard AMMA Tax Statement GlossaryDocument4 pagesAU-Unitholder-notice-Vanguard AMMA Tax Statement GlossaryNick KNo ratings yet

- AU-Vanguard Certification GuideDocument1 pageAU-Vanguard Certification GuideNick KNo ratings yet

- AU AGC Product Reference GuideDocument20 pagesAU AGC Product Reference GuideNick KNo ratings yet

- Short Bursts of Exercise Key To Feeling Full: Fron Jackson-WebbDocument3 pagesShort Bursts of Exercise Key To Feeling Full: Fron Jackson-WebbNick KNo ratings yet

- Financial Services Guide: As at 5 October 2021Document5 pagesFinancial Services Guide: As at 5 October 2021Nick KNo ratings yet

- Medtronic MM780G New Insulin Pump Order FormDocument4 pagesMedtronic MM780G New Insulin Pump Order FormNick KNo ratings yet

- AU-Vanguard Personal Investor Guide Part ADocument28 pagesAU-Vanguard Personal Investor Guide Part ANick KNo ratings yet

- Wowrpg Tech PrimerDocument4 pagesWowrpg Tech PrimerFryeShieldNo ratings yet

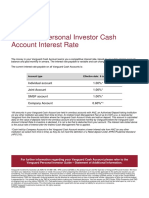

- AU-Vanguard Personal Investor-Cash Account Interest RateDocument1 pageAU-Vanguard Personal Investor-Cash Account Interest RateNick KNo ratings yet

- Common Riverbank Weeds Lower Hawk Nepean BookletDocument68 pagesCommon Riverbank Weeds Lower Hawk Nepean BookletNick KNo ratings yet

- Wow Unofficial Errata PDFDocument5 pagesWow Unofficial Errata PDFFryeShieldNo ratings yet

- Epic Rogue of Seven Sneak Attacks A Round A Creature (3Document4 pagesEpic Rogue of Seven Sneak Attacks A Round A Creature (3Nick KNo ratings yet

- Woolworths Supermarkets Agreement 2018 Final 02.10.2018Document68 pagesWoolworths Supermarkets Agreement 2018 Final 02.10.2018Nick KNo ratings yet

- Frankpocketguide - Realviewdigital.com Global Print - Asp PaDocument2 pagesFrankpocketguide - Realviewdigital.com Global Print - Asp PaNick KNo ratings yet

- OLDMUTUAL RETAIL PRODUCTsDocument7 pagesOLDMUTUAL RETAIL PRODUCTsNonny EzeNo ratings yet

- Jeevan Utsav (Sridhar) 2023Document66 pagesJeevan Utsav (Sridhar) 2023VENUGOPAL VNo ratings yet

- Superannuation WorksheetDocument2 pagesSuperannuation WorksheetAaron100% (1)

- Topic 1 - Introduction To InvestingDocument26 pagesTopic 1 - Introduction To InvestingLim Wei HanNo ratings yet

- Finland Highlight TaxDocument9 pagesFinland Highlight TaxDogeNo ratings yet

- Bar Q and ADocument20 pagesBar Q and AshakiraNo ratings yet

- EVP Attributes That Attract Veteran Candidates: ... 3x Inability To Take RisksDocument1 pageEVP Attributes That Attract Veteran Candidates: ... 3x Inability To Take RisksDiana LeheneNo ratings yet

- IRS EmpanelmentDocument2 pagesIRS Empanelmentajay chaturvediNo ratings yet

- Galt 500Document2 pagesGalt 500satishNo ratings yet

- The Innovative Enterprise and Developmental State Drive Economic GrowthDocument51 pagesThe Innovative Enterprise and Developmental State Drive Economic GrowthLautaroNo ratings yet

- High Court of Calcutta education case decisionsDocument84 pagesHigh Court of Calcutta education case decisionsShashank SumanNo ratings yet

- Case Study: Salary Inequities at Acme ManufacturingDocument2 pagesCase Study: Salary Inequities at Acme ManufacturingUmialyNo ratings yet

- Chapter 4-Final Income TaxationDocument17 pagesChapter 4-Final Income TaxationPrincesa RoqueNo ratings yet

- PD 1638 - AFP - Military - Personnel - RetirementDocument7 pagesPD 1638 - AFP - Military - Personnel - RetirementJolas BrutasNo ratings yet

- Income Tax Fundamentals 2019 37th Edition Whittenburg Solutions ManualDocument15 pagesIncome Tax Fundamentals 2019 37th Edition Whittenburg Solutions ManualMarvinGarnerfedpm100% (14)

- Q Who Can Enroll in The 401 (K) Retirement Savings Plan?Document3 pagesQ Who Can Enroll in The 401 (K) Retirement Savings Plan?us511No ratings yet

- 2010 General Mills Kellogg's Current Assets Current Liabilities Current Ratio 0.92 0.92Document3 pages2010 General Mills Kellogg's Current Assets Current Liabilities Current Ratio 0.92 0.92SHIVANI SHARMANo ratings yet

- Proposed PF Rule Amendment Draft by DG ShippingDocument19 pagesProposed PF Rule Amendment Draft by DG ShippingLegal babuNo ratings yet

- Guinea Tax 2Document6 pagesGuinea Tax 2Onur KopanNo ratings yet

- Handout 13 Chart of AccountDocument3 pagesHandout 13 Chart of AccountKyle Adrian ParoneNo ratings yet

- Grameenphone Audited Financial Statements 2022Document60 pagesGrameenphone Audited Financial Statements 2022S.R. EMONNo ratings yet

- Dawood Family Takaful LTDDocument2 pagesDawood Family Takaful LTDTaimoor AhmmedNo ratings yet

- Cash & Cash Equivalent Lecture NotesDocument6 pagesCash & Cash Equivalent Lecture NotesRena Lyn ManzanoNo ratings yet

- Constitutional Perspective - IDocument18 pagesConstitutional Perspective - IjasminjajarefeNo ratings yet

- Juixs Floyd Morpheus Manalo: Tax Code: S Attendance Period Payroll Period Release DateDocument1 pageJuixs Floyd Morpheus Manalo: Tax Code: S Attendance Period Payroll Period Release DateFLOYD MORPHEUSNo ratings yet

- Tata Consultancy Services Employees' Provident Fund: PF NoDocument1 pageTata Consultancy Services Employees' Provident Fund: PF Nosweta sharmaNo ratings yet