You might also like

- Circular No 07 2022Document4 pagesCircular No 07 2022nitin DRINo ratings yet

- UntitledDocument2 pagesUntitledibrahim javedNo ratings yet

- ValueAddedTaxAmendmentAct2022 PDFDocument17 pagesValueAddedTaxAmendmentAct2022 PDFDesmar WhitfieldNo ratings yet

- Points - Defending On The Issue of - Proper Officer and Amendments Made by The Finance Act 2022Document117 pagesPoints - Defending On The Issue of - Proper Officer and Amendments Made by The Finance Act 2022Sabrina CanoNo ratings yet

- Changes in GST LawDocument31 pagesChanges in GST LawSUNIL PUJARINo ratings yet

- Latest Idt AmendmentsDocument35 pagesLatest Idt Amendmentscsaditya20No ratings yet

- Indirect Tax Budget Updates 2022Document36 pagesIndirect Tax Budget Updates 2022ajitNo ratings yet

- Amendment CustomsDocument50 pagesAmendment Customsamithamp20No ratings yet

- Highlights of Union Budget IdtDocument9 pagesHighlights of Union Budget IdtCA Keshav MadaanNo ratings yet

- Act 1821Document18 pagesAct 1821Defimediagroup LdmgNo ratings yet

- Custom Circulars Guidance NoteDocument30 pagesCustom Circulars Guidance NoteAltafNo ratings yet

- Economic Laws Module 1Document405 pagesEconomic Laws Module 1Mohammed AslamNo ratings yet

- RSA Legal - Union Budget Analysis - Indirect TaxDocument20 pagesRSA Legal - Union Budget Analysis - Indirect TaxshwetaNo ratings yet

- Indirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Document57 pagesIndirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Mukul MograNo ratings yet

- Bank Guarantee Exemption CircularDocument7 pagesBank Guarantee Exemption Circularbibhas1No ratings yet

- Key Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestDocument23 pagesKey Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestshwetaNo ratings yet

- Islamabad Capital Territory (Tax On Services) Ordinance, 2001Document12 pagesIslamabad Capital Territory (Tax On Services) Ordinance, 2001Bilal KhanNo ratings yet

- Finance Bill 2013Document65 pagesFinance Bill 2013amars25No ratings yet

- Guidance Note On Tax Audit-Exposure DraftDocument248 pagesGuidance Note On Tax Audit-Exposure DraftPiyush KumarNo ratings yet

- Amendments in Finance Bill 2022Document20 pagesAmendments in Finance Bill 2022Prashant MunotNo ratings yet

- Supplements RCDNR December2022Document11 pagesSupplements RCDNR December2022sukritiNo ratings yet

- Annex-A: Further To Amend Certain Tax LawsDocument7 pagesAnnex-A: Further To Amend Certain Tax LawsAfreen MirzaNo ratings yet

- 01.04.2019 CGST Rules, 2017 (Part-A Rules) PDFDocument156 pages01.04.2019 CGST Rules, 2017 (Part-A Rules) PDFSanket KulkarniNo ratings yet

- Inland Revenue (Amendment) Bill PublishedDocument40 pagesInland Revenue (Amendment) Bill PublishedDarshana Sanjeewa100% (1)

- Order by The Commissioner of State Tax, Gujarat State, AhmedabadDocument10 pagesOrder by The Commissioner of State Tax, Gujarat State, Ahmedabadarpit85No ratings yet

- GST Supplement - Dec 2022Document10 pagesGST Supplement - Dec 2022SAMAR SINGH CHAUHANNo ratings yet

- Supplementary: Indirect Tax Laws & PracticeDocument9 pagesSupplementary: Indirect Tax Laws & PracticeSwetaNo ratings yet

- Factoring Regulation Bill, 2020Document9 pagesFactoring Regulation Bill, 2020Ritwik MehtaNo ratings yet

- Revenue Regulations On Retirement Benefit Plans PDFDocument15 pagesRevenue Regulations On Retirement Benefit Plans PDFJadeNo ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- LTU KarachiDocument40 pagesLTU Karachiblueman4u0% (2)

- قانون ضريبة الدخلDocument49 pagesقانون ضريبة الدخلMr AzounyNo ratings yet

- Finance Act No.06 of 2022 (CGST)Document8 pagesFinance Act No.06 of 2022 (CGST)Santosh Kumar NahakNo ratings yet

- Circular No. 38 /2016-Customs: - (1) Notwithstanding Anything Contained in This Act ButDocument18 pagesCircular No. 38 /2016-Customs: - (1) Notwithstanding Anything Contained in This Act ButAnshNo ratings yet

- SKA - Sectionwise GST Analysis - Finance Bill 2021Document24 pagesSKA - Sectionwise GST Analysis - Finance Bill 2021Sandip GoyalNo ratings yet

- COST AUDIT REPORT Meaninng of Value AdditionDocument28 pagesCOST AUDIT REPORT Meaninng of Value AdditionVikas JainNo ratings yet

- Act 20 of 2020Document8 pagesAct 20 of 2020Kriti KumarNo ratings yet

- Section 137 To 146aDocument11 pagesSection 137 To 146aSher DilNo ratings yet

- Laws of Malaysia: Act A1632Document11 pagesLaws of Malaysia: Act A1632Wei LinNo ratings yet

- AFF's Memorandum On Federal & Provincial Finance Acts, 2022Document61 pagesAFF's Memorandum On Federal & Provincial Finance Acts, 2022ABODE PVT LIMITEDNo ratings yet

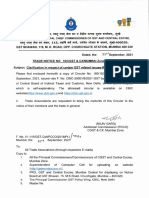

- Trade Notice No 10-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Document6 pagesTrade Notice No 10-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Gautam jainNo ratings yet

- IDT Amendement ICAIDocument0 pagesIDT Amendement ICAISuresh SharmaNo ratings yet

- GazetteDocument692 pagesGazetteKashif NiaziNo ratings yet

- Taxation Law, Full NotesDocument26 pagesTaxation Law, Full NotesPavan GuptaNo ratings yet

- CMO 28 2003 SGL Accreditation Clearance ProceduresDocument16 pagesCMO 28 2003 SGL Accreditation Clearance ProceduresJamaica Marjadas100% (1)

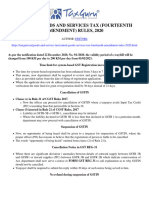

- Central Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inDocument9 pagesCentral Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inwaqtkeebaatein12No ratings yet

- Circulars/Notifications: Legal UpdateDocument6 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Cost Audit Report Rules, 2001 Ministry of Law, Justice and Company Affairs (Department of Company Affairs)Document25 pagesCost Audit Report Rules, 2001 Ministry of Law, Justice and Company Affairs (Department of Company Affairs)MAHESHNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Circular 1 2023Document1 pageCircular 1 2023KunalKumarNo ratings yet

- (Amendments For Nov 2010 / May 2011 Students) : Compiled by CA Sarthak Jain 9229223040Document17 pages(Amendments For Nov 2010 / May 2011 Students) : Compiled by CA Sarthak Jain 9229223040timirkantaNo ratings yet

- Financ BillDocument19 pagesFinanc BillmimrandawoodyNo ratings yet

- Revised Guidelines For Arrest Bail For Offences Under Customs Act, 1962 - Taxguru - inDocument3 pagesRevised Guidelines For Arrest Bail For Offences Under Customs Act, 1962 - Taxguru - inRITWIK GKNo ratings yet

- BOC CMO 32-2017 Reactivation of The Post Clearance Audit Group of The Bureau of CustomsDocument3 pagesBOC CMO 32-2017 Reactivation of The Post Clearance Audit Group of The Bureau of CustomsPortCalls100% (2)

- Circular No. 36 /2020-CustomsDocument16 pagesCircular No. 36 /2020-CustomsAshok KumarNo ratings yet

- Indirect TaxDocument4 pagesIndirect TaxAtharva SamantNo ratings yet

- Short Title, Extent and Commencement.Document13 pagesShort Title, Extent and Commencement.SagarNo ratings yet

- Section 11A. Paid or Erroneously Refunded. - : Recovery of Duties Not Levied or Not Paid or Short-Levied or ShortDocument9 pagesSection 11A. Paid or Erroneously Refunded. - : Recovery of Duties Not Levied or Not Paid or Short-Levied or ShortSushant SaxenaNo ratings yet

- ISA 250B The Auditor S Right and Duty To Report ToDocument22 pagesISA 250B The Auditor S Right and Duty To Report ToJosiah MwashitaNo ratings yet

- Instant Download Orgb 3 3rd Edition Nelson Solutions Manual PDF Full ChapterDocument16 pagesInstant Download Orgb 3 3rd Edition Nelson Solutions Manual PDF Full ChapterAnnaBurkekfon100% (5)

- PROPERTY Refers To Things Which Are Capable of Satisfying Human Wants and NeedsDocument5 pagesPROPERTY Refers To Things Which Are Capable of Satisfying Human Wants and NeedsBriana Kinagan AmangaoNo ratings yet

- TO: Mr. Michael B. Velasco: (Type Text)Document1 pageTO: Mr. Michael B. Velasco: (Type Text)sypiojeffreyNo ratings yet

- ICC FraudNet Global Annual Report 2023 LRDocument266 pagesICC FraudNet Global Annual Report 2023 LRAZHAR HASANNo ratings yet

- Financial Building Corp. v. Rudlin International Corp.Document3 pagesFinancial Building Corp. v. Rudlin International Corp.kathrynmaydevezaNo ratings yet

- People v. BenipayoDocument1 pagePeople v. BenipayoShella Hannah Salih0% (1)

- PropertyDocument8 pagesPropertyVaibhav MukhraiyaNo ratings yet

- Domondon Taxation Notes 2010-1 PDFDocument79 pagesDomondon Taxation Notes 2010-1 PDFBryna OngtiocoNo ratings yet

- Volleyball GuidelinesDocument4 pagesVolleyball GuidelinesKobe B. ZenabyNo ratings yet

- Certified AML - KYC Compliance OfficerDocument9 pagesCertified AML - KYC Compliance OfficerRicky MartinNo ratings yet

- The Zoning OrdinanceDocument56 pagesThe Zoning OrdinanceMJ CarreonNo ratings yet

- Chapter 2 LeaDocument12 pagesChapter 2 LeaChakalo HapalonNo ratings yet

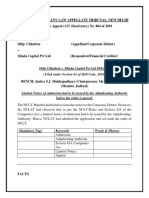

- Dilip Chhabria v. Minda Capital PVT LTDDocument3 pagesDilip Chhabria v. Minda Capital PVT LTDvarshiniNo ratings yet

- Chapter 4 - Criticism of Austin S Command Theory by HartDocument8 pagesChapter 4 - Criticism of Austin S Command Theory by Hartavinash nashNo ratings yet

- Del Monte Corporation-USA vs. Court of AppealsDocument13 pagesDel Monte Corporation-USA vs. Court of AppealsKristine Hipolito SerranoNo ratings yet

- SUCCESSION Intestate NotesDocument11 pagesSUCCESSION Intestate NotesnelfiamieraNo ratings yet

- Indeterminate Sentence LawDocument49 pagesIndeterminate Sentence LawGarco L. ConconNo ratings yet

- V. Jelks Et Al - Document No. 3Document10 pagesV. Jelks Et Al - Document No. 3Justia.comNo ratings yet

- EquityDocument2 pagesEquityzeusapocalypseNo ratings yet

- Kinney Charles Gadsden 66428 09-O-18100-3Document17 pagesKinney Charles Gadsden 66428 09-O-18100-3AdamNo ratings yet

- Credit & Transaction CasesDocument4 pagesCredit & Transaction CasesNica09_foreverNo ratings yet

- Panchayat Raj PDFDocument9 pagesPanchayat Raj PDFSUVENDU JENANo ratings yet

- CP-028 Corpuz v. SiapnoDocument2 pagesCP-028 Corpuz v. SiapnoBea Czarina NavarroNo ratings yet

- The Applicant Herein Craves The Leave of This Hon'ble Court To Most Humbly State and Submit ThatDocument21 pagesThe Applicant Herein Craves The Leave of This Hon'ble Court To Most Humbly State and Submit ThatParvaz CaziNo ratings yet

- Kautilya Theory of StateDocument15 pagesKautilya Theory of StateFRONTMAN 666No ratings yet

- American Civil Liberties Union of Massachusetts and American Oversight V Ice Prosecution of Massachusetts Judge Joseph and Court Officer MacgregorDocument9 pagesAmerican Civil Liberties Union of Massachusetts and American Oversight V Ice Prosecution of Massachusetts Judge Joseph and Court Officer MacgregorLaw&CrimeNo ratings yet

- Cruz vs. So Hiong DigestDocument3 pagesCruz vs. So Hiong DigestEmir MendozaNo ratings yet

- CPC Model QuestionsDocument23 pagesCPC Model QuestionsHarsh PatelNo ratings yet

- Final Press ForensicDocument59 pagesFinal Press ForensicA Kumar LegacyNo ratings yet

- JurisprudenceDocument11 pagesJurisprudencePuneet Tigga100% (1)