You might also like

- Adjudication in GSTDocument5 pagesAdjudication in GSTShiv Swarup PandeyNo ratings yet

- 30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document164 pages30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Dost BhawanaNo ratings yet

- 01.02.2019 CGST Rules-2017 (Part-A Rules) PDFDocument149 pages01.02.2019 CGST Rules-2017 (Part-A Rules) PDFsridharanNo ratings yet

- ST Circ 130 2k10Document2 pagesST Circ 130 2k10supdtconflNo ratings yet

- Memo No 1304Document8 pagesMemo No 1304chandra shekharNo ratings yet

- Central Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Document163 pagesCentral Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Rakshit AgarwalNo ratings yet

- GST Circular PDFDocument11 pagesGST Circular PDFNavnera divisionNo ratings yet

- CGST Rules, 2017Document159 pagesCGST Rules, 2017Rahul RockzzNo ratings yet

- Central Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Document167 pagesCentral Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Pradeep ShahNo ratings yet

- Circular 36 2018 CustomsDocument2 pagesCircular 36 2018 CustomsIAS MeenaNo ratings yet

- Part B Rules 0710Document455 pagesPart B Rules 0710Bhavin DesaiNo ratings yet

- 01.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document163 pages01.07.2020 - CGST Rules, 2017 - (Part-A - Rules)rdabliNo ratings yet

- Adobe Scan 21-Feb-2024Document8 pagesAdobe Scan 21-Feb-2024rahatkokate7No ratings yet

- Income Tax 7 Lakh CircularDocument3 pagesIncome Tax 7 Lakh CircularMCB ACCOUNT BRANCHNo ratings yet

- Income Tax (Deduction For Expenses in Relation To Secretarial Fee and Tax Filing Fee) Rules 2014 (P.U. (A) 336-2014)Document1 pageIncome Tax (Deduction For Expenses in Relation To Secretarial Fee and Tax Filing Fee) Rules 2014 (P.U. (A) 336-2014)Teh Chu LeongNo ratings yet

- DTDocument141 pagesDTManojNo ratings yet

- VILGST - CGST - Circular - Instruction No. 01 - 2022-GSTDocument4 pagesVILGST - CGST - Circular - Instruction No. 01 - 2022-GSTJAYKISHAN VIDHWANINo ratings yet

- 18.07.2019 - CGST - Rules 2017 Part ADocument159 pages18.07.2019 - CGST - Rules 2017 Part AVeli RangeNo ratings yet

- 66522bos53752 cp9Document39 pages66522bos53752 cp9Chandan ganapathi HcNo ratings yet

- IT Circular1 - 2015 PDFDocument59 pagesIT Circular1 - 2015 PDFSellanAnithaNo ratings yet

- 74823bos60500 cp14Document32 pages74823bos60500 cp14Looney ApacheNo ratings yet

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- Instruction No 022022 GST Dated 22032022Document13 pagesInstruction No 022022 GST Dated 22032022GroupA PreventiveNo ratings yet

- Annexure-1 Advisory On Interest Calculator in Gstr-3B: Annexure With Illustra Ve ExampleDocument5 pagesAnnexure-1 Advisory On Interest Calculator in Gstr-3B: Annexure With Illustra Ve ExamplepapuNo ratings yet

- Circular No.: Government India Department Revenue Board Direct Division)Document2 pagesCircular No.: Government India Department Revenue Board Direct Division)ashim1No ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Circular CGST 198Document2 pagesCircular CGST 198Jaipur-B Gr-2No ratings yet

- TapanDocument6 pagesTapanDebashis MitraNo ratings yet

- 4.2. Corporate Income Tax - Part 2Document58 pages4.2. Corporate Income Tax - Part 2Amina SultangaliyevaNo ratings yet

- Circular No 70 - NewDocument3 pagesCircular No 70 - NewHr legaladviserNo ratings yet

- 01.04.2019 CGST Rules, 2017 (Part-A Rules) PDFDocument156 pages01.04.2019 CGST Rules, 2017 (Part-A Rules) PDFSanket KulkarniNo ratings yet

- Circularno 24 CGSTDocument4 pagesCircularno 24 CGSTHr legaladviserNo ratings yet

- Guidelines Recovery Section 79 CGST Act 2017Document3 pagesGuidelines Recovery Section 79 CGST Act 2017Gaurav Kumar PatidarNo ratings yet

- Circular No.45Document5 pagesCircular No.45Hr legaladviserNo ratings yet

- CBEC-20/16/15/2018-GST Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and CustomsDocument2 pagesCBEC-20/16/15/2018-GST Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customsdinesh kasnNo ratings yet

- GST Update130 PDFDocument3 pagesGST Update130 PDFTharun RajNo ratings yet

- Direct TAX Part ADocument497 pagesDirect TAX Part Ashubh karaniaNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Government of Pakistan Federal Board of Revenue (Revenue Division) No.C.4 (1) ITP/2008-ECDocument19 pagesGovernment of Pakistan Federal Board of Revenue (Revenue Division) No.C.4 (1) ITP/2008-ECAhsan RazaNo ratings yet

- 74822bos60500 cp13Document48 pages74822bos60500 cp13Looney ApacheNo ratings yet

- Tax LawDocument535 pagesTax LawPrem MahalaNo ratings yet

- Subject: Sanction of Pending IGST Refund Claims Where The Records Have Not Been Transmitted From The GSTN To DG Systems - RegDocument4 pagesSubject: Sanction of Pending IGST Refund Claims Where The Records Have Not Been Transmitted From The GSTN To DG Systems - RegSanjay ChandelNo ratings yet

- Indirect Taxes - Transformation in GSTDocument53 pagesIndirect Taxes - Transformation in GSTJogender Chauhan100% (1)

- TDS in GSTDocument3 pagesTDS in GSTacm001No ratings yet

- Income Tax Deduction From SalariesDocument112 pagesIncome Tax Deduction From SalarieskumarNo ratings yet

- IT CircularDocument65 pagesIT Circularnavdeepsingh.india8849100% (2)

- Filing of GST ReturnsDocument7 pagesFiling of GST ReturnsRabin DebnathNo ratings yet

- Income Not Part of Total Income Full NotesDocument93 pagesIncome Not Part of Total Income Full NotesCA Rishabh DaiyaNo ratings yet

- Part A Rules 0710Document172 pagesPart A Rules 0710Bhavin DesaiNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- Reverse Charge MechanismDocument19 pagesReverse Charge MechanismSayyadNo ratings yet

- Payment of TaxDocument40 pagesPayment of TaxMayur samdariyaNo ratings yet

- Custom Circulars Guidance NoteDocument30 pagesCustom Circulars Guidance NoteAltafNo ratings yet

- CA Inter Payment of GST Notes @mission - CA - InterDocument36 pagesCA Inter Payment of GST Notes @mission - CA - InterKush BafnaNo ratings yet

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesFrom EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesNo ratings yet

- FAKE ITC SCN Instructions Cir-171!03!2022-CgstDocument4 pagesFAKE ITC SCN Instructions Cir-171!03!2022-CgstGroupA PreventiveNo ratings yet

- Part A Rules 0122Document174 pagesPart A Rules 0122GroupA PreventiveNo ratings yet

- RulesDocument389 pagesRulesSaloni ChhabraNo ratings yet

- Part B Rules 0710Document455 pagesPart B Rules 0710Bhavin DesaiNo ratings yet

- Advisory For Action Fake Itc Recipients Date 19.1.21Document2 pagesAdvisory For Action Fake Itc Recipients Date 19.1.21GroupA PreventiveNo ratings yet

- Project ModelsDocument5 pagesProject ModelsHARSH RANJANNo ratings yet

- FMI7e ch09Document44 pagesFMI7e ch09lehoangthuchien100% (1)

- Unit 4 Receivables ManagementDocument20 pagesUnit 4 Receivables ManagementAbin VargheseNo ratings yet

- Primary MarketDocument26 pagesPrimary MarketumarsmakNo ratings yet

- Hotel IndustryDocument9 pagesHotel IndustryRaghu Citech N SjecNo ratings yet

- Housing Choice Voucher Payments ContractBody of Contract Part B 52641Document12 pagesHousing Choice Voucher Payments ContractBody of Contract Part B 52641shaundirelemonde100% (1)

- 41b EnglishDocument28 pages41b Englishபூவை ஜெ ரூபன்சார்லஸ்No ratings yet

- BAT Financial Analysis ReportDocument11 pagesBAT Financial Analysis ReportTashrif Ul AminNo ratings yet

- Accounting Course ManualDocument238 pagesAccounting Course Manualsanu sayedNo ratings yet

- Policy On Accounts ReceivableDocument8 pagesPolicy On Accounts ReceivableMazhar Hussain Ch.No ratings yet

- Far - Long Quiz - Nov 28, 2019Document1 pageFar - Long Quiz - Nov 28, 2019Renalyn ParasNo ratings yet

- Skim Penyelesaian Pinjaman Kecil Small Debt Resolution SchemeDocument6 pagesSkim Penyelesaian Pinjaman Kecil Small Debt Resolution SchemeFikri HijazNo ratings yet

- Apple Business PlanDocument8 pagesApple Business PlanGeneve GarzonNo ratings yet

- Article 1241Document2 pagesArticle 1241VICTORIA ME�OZANo ratings yet

- Formula Options - Trading - Strategies PDFDocument2 pagesFormula Options - Trading - Strategies PDFSameer Shinde100% (1)

- INDEMNITYDocument8 pagesINDEMNITYGaurav JindalNo ratings yet

- (CredTran) 50 - Willex Indutry V CA - ParafinaDocument2 pages(CredTran) 50 - Willex Indutry V CA - ParafinaAlecParafina100% (1)

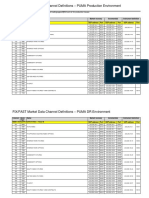

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument3 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- MODULE 1 Overview of EntrepreneurshipDocument32 pagesMODULE 1 Overview of Entrepreneurshipjulietpamintuan100% (11)

- Tax Expenditures in Latin America Civil Society Perspective English Ibp 2019Document27 pagesTax Expenditures in Latin America Civil Society Perspective English Ibp 2019Paolo de RenzioNo ratings yet

- BKash Performance Analysis & ValuationDocument12 pagesBKash Performance Analysis & ValuationZeehenul IshfaqNo ratings yet

- Inflation, Its Types, Causes and MeasuresDocument10 pagesInflation, Its Types, Causes and MeasuresANAM RAUF (GCUF)100% (1)

- FBAI Final ReportDocument14 pagesFBAI Final ReportSrishti JoshiNo ratings yet

- Doctrine of Mortgagee in Good FaithDocument2 pagesDoctrine of Mortgagee in Good FaithVictor FaeldonNo ratings yet

- Operations and Productivity SlidesDocument47 pagesOperations and Productivity SlidesgardeziiNo ratings yet

- Lichello A.I.M. ImprovementsDocument8 pagesLichello A.I.M. Improvementsd1234dNo ratings yet

- AFM-Module 4 Part-B Ratio Analysis ProblemsDocument5 pagesAFM-Module 4 Part-B Ratio Analysis ProblemskanikaNo ratings yet

- Bhanu Chaitanya Kumar (11) : Presented byDocument16 pagesBhanu Chaitanya Kumar (11) : Presented bySriramya PediredlaNo ratings yet

- Business Applications FOR BASE, RATE, PERCENTAGEDocument36 pagesBusiness Applications FOR BASE, RATE, PERCENTAGEVevianJavierCervantesNo ratings yet

- Financial Analyst in NYC NY Resume Jasmin JarquioDocument2 pagesFinancial Analyst in NYC NY Resume Jasmin JarquioJasminJarquioNo ratings yet