You might also like

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsFrom EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsRating: 5 out of 5 stars5/5 (1)

- Insurance and BondsDocument15 pagesInsurance and BondsJackson TanNo ratings yet

- Question #1: When The Obligor Requested For An Extension of TimeDocument12 pagesQuestion #1: When The Obligor Requested For An Extension of TimeJan ryan100% (2)

- Extinguishment of Obligation - Lecture NotesDocument186 pagesExtinguishment of Obligation - Lecture NotesJanetGraceDalisayFabreroNo ratings yet

- CHAPTER 4 - Extinguishment of ObligationDocument65 pagesCHAPTER 4 - Extinguishment of ObligationJane CANo ratings yet

- Article 1239Document6 pagesArticle 1239Kang Minhee100% (1)

- Obligation and Contract-ExtinguishmentDocument8 pagesObligation and Contract-ExtinguishmentKaren Tuala-GuerraNo ratings yet

- Lecture in Special ProceedingsDocument30 pagesLecture in Special ProceedingsMang K NorNo ratings yet

- 6.1-2. PriorityDocument8 pages6.1-2. PriorityTonyNo ratings yet

- Articles 1239-1243Document18 pagesArticles 1239-1243Gabs SolivenNo ratings yet

- Stone Container Case DiscussionDocument7 pagesStone Container Case DiscussionMeena83% (6)

- Paper-5 Financial Accounting PDFDocument534 pagesPaper-5 Financial Accounting PDFAshish Rai50% (2)

- Oblicon Week 5Document102 pagesOblicon Week 5Ashly MateoNo ratings yet

- Modes of Extiguishment of Obligations Payment: PayorDocument17 pagesModes of Extiguishment of Obligations Payment: PayorRizza Angela Mangalleno100% (1)

- Alemar's Sibal & Sons, Inc. v. Hon. Elbinias, Yupangco & Co. DoctrineDocument1 pageAlemar's Sibal & Sons, Inc. v. Hon. Elbinias, Yupangco & Co. DoctrineVon Lee De LunaNo ratings yet

- Articles 1231-1240 (Extinguishment of Obligations - Payment or Performance I)Document40 pagesArticles 1231-1240 (Extinguishment of Obligations - Payment or Performance I)DJAN IHIAZEL DELA CUADRANo ratings yet

- Extinguishment of ObligationsDocument10 pagesExtinguishment of ObligationsNimfa SabanalNo ratings yet

- Request For Quotation (RFQ)Document12 pagesRequest For Quotation (RFQ)AAYAN001100% (1)

- Republic Bank VS EbradaDocument2 pagesRepublic Bank VS EbradaaxvxxnNo ratings yet

- Ease of Doing Business - BRAZILDocument20 pagesEase of Doing Business - BRAZILkirti raj singh shekhawatNo ratings yet

- Oblicon Finals ModuleDocument37 pagesOblicon Finals ModuleKrizza Ann Olivia NavarroNo ratings yet

- Barq CompiledDocument36 pagesBarq CompiledPamNo ratings yet

- Chapter 4 (Section 1) Study Guide IDocument4 pagesChapter 4 (Section 1) Study Guide ILeinard AgcaoiliNo ratings yet

- JOSE HAUTEA V NLRCDocument2 pagesJOSE HAUTEA V NLRCMavic MoralesNo ratings yet

- Extinguishment of Obligations: Payment Means Not Only Delivery of Money But Also The PerformanceDocument17 pagesExtinguishment of Obligations: Payment Means Not Only Delivery of Money But Also The PerformanceAryan LeeNo ratings yet

- Extinguishment of ObligationsDocument6 pagesExtinguishment of ObligationsRasmus BernardoNo ratings yet

- Completion Examination: ND RDDocument5 pagesCompletion Examination: ND RDNicole DeocarisNo ratings yet

- Spouses Miniano B. Dela Cruz and Leta L. Dela Cruz, (Petitioner) vs. Ana Marie Concepcion, (Respondent) G.R. 172825, October 11, 2012Document2 pagesSpouses Miniano B. Dela Cruz and Leta L. Dela Cruz, (Petitioner) vs. Ana Marie Concepcion, (Respondent) G.R. 172825, October 11, 2012ralph_atmosferaNo ratings yet

- Law Final ExamDocument29 pagesLaw Final Exam靳雪娇No ratings yet

- Compania General de Tabacos Vs GauzonDocument2 pagesCompania General de Tabacos Vs Gauzonbebs CachoNo ratings yet

- Extingushment of Obligation ReviewerDocument18 pagesExtingushment of Obligation ReviewerLabele MikkaNo ratings yet

- Article 1241-1246 (For Reporting)Document3 pagesArticle 1241-1246 (For Reporting)VICTORIA ME�OZANo ratings yet

- Art. 1236. The Creditor Is Not Bound To AcceptDocument3 pagesArt. 1236. The Creditor Is Not Bound To AcceptGraceAnne SorongonNo ratings yet

- Bam026 Group1Document2 pagesBam026 Group1Maureen SanchezNo ratings yet

- Art 1241 1244Document4 pagesArt 1241 1244Maureen SanchezNo ratings yet

- Payment or PerformanceDocument29 pagesPayment or PerformanceRizelle ViloriaNo ratings yet

- Extinguishment of Obligations Payment or PerformanceDocument42 pagesExtinguishment of Obligations Payment or Performanceuchan8557No ratings yet

- BiconDocument8 pagesBiconRuss RoqueroNo ratings yet

- Article 1302Document5 pagesArticle 1302Ian Eldrick Dela CruzNo ratings yet

- Subsection 3Document4 pagesSubsection 3aizelvillateNo ratings yet

- MODULE 3 - Extinguishment of ObligationsDocument8 pagesMODULE 3 - Extinguishment of ObligationsALYSSA LEIGH VILLAREALNo ratings yet

- Obligations Are ExtinguishedDocument24 pagesObligations Are ExtinguishedikayNo ratings yet

- Payment of Performance 2Document28 pagesPayment of Performance 2Avila SimonNo ratings yet

- Extinguishment of ObligationsDocument14 pagesExtinguishment of Obligationsisaah27.tagleNo ratings yet

- SummaryDocument4 pagesSummaryMICHAEL ADOLFONo ratings yet

- Ii. X C: X Can Recover The Excess Payment FromDocument2 pagesIi. X C: X Can Recover The Excess Payment FromCzarina BantayNo ratings yet

- Law 26Document6 pagesLaw 26ram RedNo ratings yet

- Extinguishment of ObligationDocument22 pagesExtinguishment of ObligationKay QuintanaNo ratings yet

- Tan, Rachel - BUSE304MTH-HW2Document3 pagesTan, Rachel - BUSE304MTH-HW2Rachel Jane TanNo ratings yet

- Module 2 - Topic No. 2 - Part6Document10 pagesModule 2 - Topic No. 2 - Part6hanlqNo ratings yet

- Case DigestsDocument53 pagesCase DigestsMingNo ratings yet

- Oblicon Module 8 (Section 1)Document14 pagesOblicon Module 8 (Section 1)Mika MolinaNo ratings yet

- 3rd Assignment For Week May 4 To May 8, 2020Document3 pages3rd Assignment For Week May 4 To May 8, 2020Ara Jane T. PiniliNo ratings yet

- Article 1241: March 25, 2016Document2 pagesArticle 1241: March 25, 2016AtNarulapaNo ratings yet

- 7) Actionable ClaimDocument4 pages7) Actionable ClaimCharran saNo ratings yet

- Article 1241-1249Document3 pagesArticle 1241-1249Andrea Angelica Dumo GalvezNo ratings yet

- Law On Obligations and Contract ActivityDocument4 pagesLaw On Obligations and Contract Activityscholta00No ratings yet

- Obligations+and+Contracts+-+Midterm Coverage UPDATED HANDOUTS 2021Document11 pagesObligations+and+Contracts+-+Midterm Coverage UPDATED HANDOUTS 2021Angela NavaltaNo ratings yet

- Module IV - A Extinguishment of ObligationsDocument44 pagesModule IV - A Extinguishment of ObligationsMaryja CenetaNo ratings yet

- Extinguishment of ObliDocument47 pagesExtinguishment of ObliFirmalan Jacobine Marie F.No ratings yet

- ACFrOgB JejacC8kcOm 5gIUaDdlPlZXMbkXdCT5cGCg0BGCLOEmsGF0-U7cl0msxZZEP9RlwTPa5pGFIxOJta3TmqHoJxZ5HfVpFS8EbddO82S5ARqYLbgDKltQlx2MU7Iknvj6p3vJ8gQ2LzIUDocument2 pagesACFrOgB JejacC8kcOm 5gIUaDdlPlZXMbkXdCT5cGCg0BGCLOEmsGF0-U7cl0msxZZEP9RlwTPa5pGFIxOJta3TmqHoJxZ5HfVpFS8EbddO82S5ARqYLbgDKltQlx2MU7Iknvj6p3vJ8gQ2LzIUPamaran GianNo ratings yet

- Illustration:: Difference Between Donation and CondonationDocument5 pagesIllustration:: Difference Between Donation and Condonationione salveronNo ratings yet

- Ordinary Parlance: It Refers Only To The Delivery of in Legal Mode: Payment May Consist of Not Only in TheDocument3 pagesOrdinary Parlance: It Refers Only To The Delivery of in Legal Mode: Payment May Consist of Not Only in ThePrincess Diane PalisocNo ratings yet

- Article 1634-1635Document11 pagesArticle 1634-1635Bianca Jane MaaliwNo ratings yet

- Module 4Document4 pagesModule 4AEKONo ratings yet

- Actionable Claims - Doc NotesDocument5 pagesActionable Claims - Doc NotesAbhishek tiwariNo ratings yet

- Salvador Panganiban Vs Agustin Cuevas 7 Phil 477 Case DigestDocument19 pagesSalvador Panganiban Vs Agustin Cuevas 7 Phil 477 Case DigestMalvin Aragon BalletaNo ratings yet

- Section 1.: Payment or PerformanceDocument98 pagesSection 1.: Payment or PerformanceChad Daniel MorgadoNo ratings yet

- Section 3Document20 pagesSection 3Gio ReyesNo ratings yet

- Law ExercisesDocument13 pagesLaw ExercisesThug ProNo ratings yet

- Testbank 2Document5 pagesTestbank 2momoloomimaoNo ratings yet

- Colinares V. Ca FactsDocument2 pagesColinares V. Ca FactsBenedict AlvarezNo ratings yet

- Art. 1296Document1 pageArt. 1296VICTORIA ME�OZANo ratings yet

- 1265Document1 page1265VICTORIA ME�OZANo ratings yet

- Art. 1295Document1 pageArt. 1295VICTORIA ME�OZANo ratings yet

- Art. 1294Document1 pageArt. 1294VICTORIA ME�OZANo ratings yet

- Art. 1291Document2 pagesArt. 1291VICTORIA ME�OZANo ratings yet

- Article 1246Document2 pagesArticle 1246VICTORIA ME�OZANo ratings yet

- Article 1243Document1 pageArticle 1243VICTORIA ME�OZANo ratings yet

- Article 1245Document1 pageArticle 1245VICTORIA ME�OZANo ratings yet

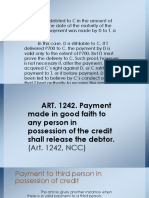

- Article 1242Document1 pageArticle 1242VICTORIA ME�OZANo ratings yet

- Article 1244Document1 pageArticle 1244VICTORIA ME�OZANo ratings yet

- Case LawDocument16 pagesCase LawVICTORIA ME�OZANo ratings yet

- Doctrine of Last AntecedentDocument32 pagesDoctrine of Last Antecedentdrumbeater79No ratings yet

- Browerville Blade - 09/20/2012Document12 pagesBrowerville Blade - 09/20/2012bladepublishingNo ratings yet

- Registration of Amrapali Under RERA CancelledDocument205 pagesRegistration of Amrapali Under RERA CancelledskvaleeNo ratings yet

- Sunbeam CorporationDocument19 pagesSunbeam CorporationKeevin Ashley67% (3)

- Innoventive Industries LTD V Icici Bank Case AnalysisDocument7 pagesInnoventive Industries LTD V Icici Bank Case AnalysisRimika ChauhanNo ratings yet

- DPLC Program Development Loan ApplicationDocument10 pagesDPLC Program Development Loan ApplicationmamaNo ratings yet

- 10000001730Document208 pages10000001730Chapter 11 DocketsNo ratings yet

- Problems of Indian Banking SectorDocument17 pagesProblems of Indian Banking Sectormayank poddarNo ratings yet

- Counsel For in Re Kitec Fitting Litigation Class Plaintiffs: Certificate of ServiceDocument6 pagesCounsel For in Re Kitec Fitting Litigation Class Plaintiffs: Certificate of ServiceChapter 11 DocketsNo ratings yet

- Matias Final Cases Civ Pro 2017 Atty CaycoDocument6 pagesMatias Final Cases Civ Pro 2017 Atty CaycoMichelle Dulce Mariano CandelariaNo ratings yet

- Bailouts and Bankruptcies - Corporate Distress, Troubled Debt Restructurings and Equity StrippingDocument61 pagesBailouts and Bankruptcies - Corporate Distress, Troubled Debt Restructurings and Equity StrippingjeganrajrajNo ratings yet

- Benevis Bankruptcy Doc 82 - Master Serv List PDFDocument6 pagesBenevis Bankruptcy Doc 82 - Master Serv List PDFDentist The MenaceNo ratings yet

- FIN 9781 Midterm 2Document2 pagesFIN 9781 Midterm 2Thabata RibeiroNo ratings yet

- Motion For Relief From Stay Alvin Marrero Vs Pesquera PRPDDocument48 pagesMotion For Relief From Stay Alvin Marrero Vs Pesquera PRPDEmily RamosNo ratings yet

- Voluntary Strike-Off and Dissolution of A Company.Document6 pagesVoluntary Strike-Off and Dissolution of A Company.Dimbacrazy TVNo ratings yet

- Balochistan Sales Tax On Services Act, 2015Document74 pagesBalochistan Sales Tax On Services Act, 2015AbidRazacaNo ratings yet

- Appendix Vol II (NXPL)Document295 pagesAppendix Vol II (NXPL)Nancy Duffy McCarronNo ratings yet

- Ridgway BK Response To ComplaintDocument6 pagesRidgway BK Response To Complaintthe kingfishNo ratings yet