You might also like

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Module 6Document6 pagesModule 6Mary Joy CabilNo ratings yet

- Ratio AnalysisDocument16 pagesRatio Analysisabhishekanandsingh123goNo ratings yet

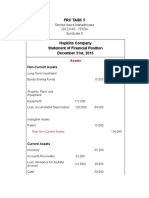

- FRC Task 5Document4 pagesFRC Task 5Denisa Naura MahadhiyasaNo ratings yet

- Assignment #3Document3 pagesAssignment #3Ngll TcmNo ratings yet

- Accounts Receivables and Payables A&BDocument9 pagesAccounts Receivables and Payables A&BAb PiousNo ratings yet

- Unit 1 Intacc3Document5 pagesUnit 1 Intacc3Faith Berrie RemigioNo ratings yet

- Notes On Management AccountingDocument71 pagesNotes On Management AccountingKartikNo ratings yet

- FinMan RemovalDocument15 pagesFinMan RemovalJAL KETH ABUEVANo ratings yet

- Befa Unit - VDocument22 pagesBefa Unit - VMahesh BabuNo ratings yet

- Module 7 Loans Receivable and Impairment of ReceivablesDocument10 pagesModule 7 Loans Receivable and Impairment of Receivablesshaira doctorNo ratings yet

- Solutions Quiz 1 and Quiz 2Document9 pagesSolutions Quiz 1 and Quiz 2BatrisyiaNo ratings yet

- Assignment Bsa-1b Rhaven VinluanDocument4 pagesAssignment Bsa-1b Rhaven VinluanRhaven Kane VinluanNo ratings yet

- Liquidity RatioDocument15 pagesLiquidity RatioLovely Joy CruzNo ratings yet

- U2 RatioAnalysisDocument56 pagesU2 RatioAnalysisvivekprasath soundararajanNo ratings yet

- Financial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesDocument2 pagesFinancial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesMay Grethel Joy PeranteNo ratings yet

- Session 2 Revenue Recognition AR InventoryDocument41 pagesSession 2 Revenue Recognition AR InventoryNANo ratings yet

- Module 5 AgingDocument3 pagesModule 5 Aginglil mixNo ratings yet

- Philippine Christian University Solutions to Problems 5-B4 and 5-B5Document5 pagesPhilippine Christian University Solutions to Problems 5-B4 and 5-B5Coreen Andrade50% (2)

- Liquidity RatiosDocument14 pagesLiquidity RatiosAnon sonNo ratings yet

- Financial Analysis RatiosDocument17 pagesFinancial Analysis RatiosRajesh PatilNo ratings yet

- Cash and Liquidity ManagementDocument14 pagesCash and Liquidity ManagementAldrin ZolinaNo ratings yet

- Question No. 2 Current RatioDocument4 pagesQuestion No. 2 Current Ratioknvs sivakumarNo ratings yet

- Ratio AnalysisDocument9 pagesRatio AnalysisCrazy electroNo ratings yet

- Ch3 Notes BinaluyoDocument19 pagesCh3 Notes BinaluyoScarlet DragonNo ratings yet

- RATIO Practice QuestionsDocument14 pagesRATIO Practice Questionspranay raj rathoreNo ratings yet

- An Assignment On Ratio Analysis AutoDocument20 pagesAn Assignment On Ratio Analysis AutoMehedi HasanNo ratings yet

- MBA Financial AccountingDocument5 pagesMBA Financial AccountingabhinavNo ratings yet

- WORKING CAPITAL MANAGEMENTDocument38 pagesWORKING CAPITAL MANAGEMENTKinNo ratings yet

- Ratio Analysis SRKDocument61 pagesRatio Analysis SRKsrkwin6No ratings yet

- Financial Analysis TestsDocument25 pagesFinancial Analysis Teststheodor_munteanuNo ratings yet

- Liabilities in Accounting Examples & Formulas - How To Calculate Total Liabilities - Video & Lesson TranscriptDocument6 pagesLiabilities in Accounting Examples & Formulas - How To Calculate Total Liabilities - Video & Lesson Transcriptmike tanNo ratings yet

- Pamela Company #11Document7 pagesPamela Company #11Yassi CurtisNo ratings yet

- ACC117 Project 2Document7 pagesACC117 Project 2Aliamaisara ZahiraNo ratings yet

- Maf253 - SS - July 2021Document11 pagesMaf253 - SS - July 2021Shazrul FadzlyNo ratings yet

- IA - Receivables Addtl ConceptsDocument3 pagesIA - Receivables Addtl ConceptsDiana AcostaNo ratings yet

- Accounting Concepts and PrinciplesDocument30 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoNo ratings yet

- Mohd Azmezanshah Bin SezwanDocument4 pagesMohd Azmezanshah Bin SezwanMohd Azmezanshah Bin SezwanNo ratings yet

- Previous Year Memory Based PaperDocument25 pagesPrevious Year Memory Based Paperyash maneNo ratings yet

- Rasio Metode Perhitungan Likuiditas 2020Document26 pagesRasio Metode Perhitungan Likuiditas 2020nurazirapfNo ratings yet

- Module 4Document17 pagesModule 4Usman AliNo ratings yet

- Revised - Econ and Financial Analysis 2nd HomeworkDocument3 pagesRevised - Econ and Financial Analysis 2nd HomeworkcaitlynnsetiabudiNo ratings yet

- Financial AnalysisDocument25 pagesFinancial AnalysisJason Bernard F. RanasNo ratings yet

- Working Capital Management TechniquesDocument4 pagesWorking Capital Management TechniquesKristine dela CruzNo ratings yet

- Problem 2-12 Answer ADocument3 pagesProblem 2-12 Answer ARendyl Earvin BagulloNo ratings yet

- FM Tea B-62Document12 pagesFM Tea B-62sayali bangaleNo ratings yet

- AccountsDocument8 pagesAccountsVishal MehtaNo ratings yet

- Financial Management Problems Solutions 1Document6 pagesFinancial Management Problems Solutions 1Levi Lazareno Eugenio100% (1)

- CH 02Document20 pagesCH 02duy blaNo ratings yet

- DocxDocument65 pagesDocxAllana MierNo ratings yet

- Understand Liabilities in 4 StepsTITLEDocument6 pagesUnderstand Liabilities in 4 StepsTITLEMai RuizNo ratings yet

- Exam Revision - Chapter 3 4Document6 pagesExam Revision - Chapter 3 4Vũ Thị NgoanNo ratings yet

- Chapt 13 Practice SolutionsDocument3 pagesChapt 13 Practice SolutionsLaphat PiriyakiarNo ratings yet

- Short-term examDocument6 pagesShort-term examymkuzangwe16No ratings yet

- Analysis and Interpretation - Ballada-Part 2Document4 pagesAnalysis and Interpretation - Ballada-Part 2Claire Evann Villena EboraNo ratings yet

- Financial Accounting & Analysis - N (1A)Document10 pagesFinancial Accounting & Analysis - N (1A)Tajinder MatharuNo ratings yet

- PDFDocument7 pagesPDFAbegail AdoraNo ratings yet

- Intermediate AccountingDocument36 pagesIntermediate AccountingJerome SarmientoNo ratings yet

- Gross Working CapitalDocument14 pagesGross Working Capitalfizza amjadNo ratings yet

- Control Cash Flows & Extend PaymentsDocument5 pagesControl Cash Flows & Extend PaymentsMiracle SalvadorNo ratings yet

- Forecasting ComputationDocument6 pagesForecasting Computationjonalyn arellanoNo ratings yet

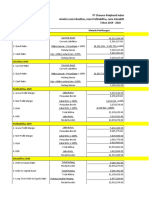

- 2.4 Times: Total Quick Assets 132,739.00 Prepaid Expenses Total Current Assets 164,949.00Document2 pages2.4 Times: Total Quick Assets 132,739.00 Prepaid Expenses Total Current Assets 164,949.00jonalyn arellanoNo ratings yet

- HRM Module Unit 1 2Document7 pagesHRM Module Unit 1 2jonalyn arellanoNo ratings yet

- Reaction Paper On Nike Inc. - Strategic Plan Analysis: Part 1: SummaryDocument3 pagesReaction Paper On Nike Inc. - Strategic Plan Analysis: Part 1: Summaryjonalyn arellanoNo ratings yet

- Activity 1 - Fin. AnalysisDocument1 pageActivity 1 - Fin. Analysisjonalyn arellanoNo ratings yet

- Research Methods Requirement FormatDocument3 pagesResearch Methods Requirement Formatjonalyn arellanoNo ratings yet

- Research Methods Requirement FormatDocument3 pagesResearch Methods Requirement Formatjonalyn arellanoNo ratings yet

- Survey Questionnaire: Check Mark in The Box of Your AnswerDocument6 pagesSurvey Questionnaire: Check Mark in The Box of Your Answerjonalyn arellanoNo ratings yet

- Organizational BehaviorDocument43 pagesOrganizational Behaviorjonalyn arellanoNo ratings yet

- Jon Research FormatDocument2 pagesJon Research Formatjonalyn arellanoNo ratings yet

- Organizational BehaviorDocument43 pagesOrganizational Behaviorjonalyn arellanoNo ratings yet

- Survey Questionnaire: Check Mark in The Box of Your AnswerDocument6 pagesSurvey Questionnaire: Check Mark in The Box of Your Answerjonalyn arellanoNo ratings yet

- Organizational Behavior 1Document40 pagesOrganizational Behavior 1jonalyn arellanoNo ratings yet

- DR Essam Book PDFDocument86 pagesDR Essam Book PDFDariaNo ratings yet

- Financial Stament Review PDFDocument8 pagesFinancial Stament Review PDFglenn dandyne montanoNo ratings yet

- 2nd Activity-Reaction Paper On Local Govt TaxationDocument2 pages2nd Activity-Reaction Paper On Local Govt Taxationjonalyn arellanoNo ratings yet

- Tram Grooved Rails New Catalog January 2018Document12 pagesTram Grooved Rails New Catalog January 2018Szabolcs Attila KöllőNo ratings yet

- tổng hợp đề KTQT 2Document43 pagestổng hợp đề KTQT 2Ly BùiNo ratings yet

- Entrepreneurial Mindset of Nepalese Youths: A Proposal OnDocument9 pagesEntrepreneurial Mindset of Nepalese Youths: A Proposal OnJason RaiNo ratings yet

- 5 - Spa To Transfer TitleDocument2 pages5 - Spa To Transfer TitleAntonio AlfelorNo ratings yet

- Lara's Gift InterestDocument1 pageLara's Gift InterestWendz GatdulaNo ratings yet

- 04 Securities Act, 2015Document17 pages04 Securities Act, 2015Nasir HussainNo ratings yet

- Group Assignment MGCR 382 Fall 2023, Oct. 4Document9 pagesGroup Assignment MGCR 382 Fall 2023, Oct. 4darkninjaNo ratings yet

- Annex "H" Documentary Requirement Alternative Methods of ProcurementDocument2 pagesAnnex "H" Documentary Requirement Alternative Methods of ProcurementAdonis BarraquiasNo ratings yet

- Assignmeliptopnt of LiptonDocument13 pagesAssignmeliptopnt of LiptonKomal Goklani100% (2)

- Capra Intra-Day Trading With Market Interals Part I ManualDocument51 pagesCapra Intra-Day Trading With Market Interals Part I ManualVarun Vasurendran100% (1)

- Ahmed Villas, Kacha Shahab Pura, ., Sialkot Sialkot Arifa MamoonaDocument4 pagesAhmed Villas, Kacha Shahab Pura, ., Sialkot Sialkot Arifa MamoonaZeeshan Haider RizviNo ratings yet

- Addition/Modification/Replacement (Amr) SchemeDocument1 pageAddition/Modification/Replacement (Amr) SchemeDebasis BasaNo ratings yet

- Legal Chart Prabhu231082010Document18 pagesLegal Chart Prabhu231082010vakilarunNo ratings yet

- SEC Objection To Binance VoyagerDocument7 pagesSEC Objection To Binance VoyagerGMG EditorialNo ratings yet

- Case Stdy OPM545 (Boys and Boden)Document15 pagesCase Stdy OPM545 (Boys and Boden)wasab negiNo ratings yet

- Tax 1 Vthsem Module 1,2, and 3Document97 pagesTax 1 Vthsem Module 1,2, and 3Sahana narayanNo ratings yet

- LULU ReportDocument4 pagesLULU Reportyovokew738No ratings yet

- Statement Nov 2022Document25 pagesStatement Nov 2022Josué SoteloNo ratings yet

- ACCY 303 Midterm Exam ReviewDocument12 pagesACCY 303 Midterm Exam ReviewCORNADO, MERIJOY G.No ratings yet

- Fnbslw444 - Case StudyDocument5 pagesFnbslw444 - Case Studyinfobrains05No ratings yet

- It Is The Final Stage in The Strategic Management ProcessDocument66 pagesIt Is The Final Stage in The Strategic Management ProcessnathalieNo ratings yet

- Student Survival Guide for BrusselsDocument22 pagesStudent Survival Guide for BrusselsAdheip RashadaNo ratings yet

- Anand Mahindra ProfileDocument14 pagesAnand Mahindra ProfileKhawar MehdiNo ratings yet

- Meryl Manalo Minutes of The MeetingDocument3 pagesMeryl Manalo Minutes of The MeetingBoogie San JuanNo ratings yet

- Anarock - Annual - Report 2022 - Residential Real EstateDocument39 pagesAnarock - Annual - Report 2022 - Residential Real EstatekabithNo ratings yet

- @afar - Complete (Oct2021-Dec2021)Document39 pages@afar - Complete (Oct2021-Dec2021)Violet BaudelaireNo ratings yet

- Company Law Assignment of Formation of CompanyDocument43 pagesCompany Law Assignment of Formation of CompanyTayyaba TariqNo ratings yet

- AsterDM Annual Report FY 2019-20Document280 pagesAsterDM Annual Report FY 2019-20Jayaprakash MuthuvatNo ratings yet

- CASE STUDY-Walmart VS AmazonDocument3 pagesCASE STUDY-Walmart VS AmazonManasi VermaNo ratings yet

- Small Business An Entrepreneurs Plan 6th Edition Knowles Solutions ManualDocument23 pagesSmall Business An Entrepreneurs Plan 6th Edition Knowles Solutions Manualroryytpvk5g100% (28)