You might also like

- Addtional Cash Flow Problems and SolutionsDocument7 pagesAddtional Cash Flow Problems and SolutionsHossein ParvardehNo ratings yet

- 11 To 20Document96 pages11 To 20JorniNo ratings yet

- MA Assignment IVDocument16 pagesMA Assignment IVJaya BharneNo ratings yet

- Property, Plant, Equipment: Abbey Corporation Statement of Financial Position DECEMBER 31,2015 AssetDocument4 pagesProperty, Plant, Equipment: Abbey Corporation Statement of Financial Position DECEMBER 31,2015 AssetAstri KaruniaNo ratings yet

- Highland Malt Accounting Project PDFDocument12 pagesHighland Malt Accounting Project PDFEng Chee Liang100% (1)

- Assignment 03Document7 pagesAssignment 03Nadeera GalagedarageNo ratings yet

- 2023 - Session12 - 13 FSA2 - MBA - SentDocument32 pages2023 - Session12 - 13 FSA2 - MBA - SentAkshat MathurNo ratings yet

- Examination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash FlowDocument3 pagesExamination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- Financial Analysis TestsDocument25 pagesFinancial Analysis Teststheodor_munteanuNo ratings yet

- FR AS ScannerDocument144 pagesFR AS ScannerPooja GuptaNo ratings yet

- St. Haniel C.A Exercise 6Document11 pagesSt. Haniel C.A Exercise 6ArthurLeonard MalijanNo ratings yet

- Solve Cash Flow ProblemsDocument3 pagesSolve Cash Flow ProblemsMichelle ManuelNo ratings yet

- NGA-SCE Financial Accounting Analysis AssignmentDocument21 pagesNGA-SCE Financial Accounting Analysis Assignmentmohammad fakhruddinNo ratings yet

- Principles of Accounting 5th Edition Smart Solutions ManualDocument9 pagesPrinciples of Accounting 5th Edition Smart Solutions Manualspaidvulcano8wlriz100% (19)

- Case 1Document5 pagesCase 1noor memekNo ratings yet

- MBA Accounts2Document5 pagesMBA Accounts2Yojan PonnettiNo ratings yet

- 130565353X 540322Document19 pages130565353X 540322blackghostNo ratings yet

- Dewa Satria Rachman LubisDocument13 pagesDewa Satria Rachman LubisDewaSatriaNo ratings yet

- Liquidity Ratios - Practice QuestionsDocument14 pagesLiquidity Ratios - Practice QuestionsOsama SaleemNo ratings yet

- P8 MTP 1 For Nov 23 Answers @CAInterLegendsDocument18 pagesP8 MTP 1 For Nov 23 Answers @CAInterLegendsraghavagarwal2252No ratings yet

- Chapter 3 Working CapitalDocument39 pagesChapter 3 Working Capitalericka casiNo ratings yet

- PA Biweekly5 G1Document3 pagesPA Biweekly5 G1Quang NguyenNo ratings yet

- Ratio Analysis - Advanced QuestionsDocument5 pagesRatio Analysis - Advanced Questionsrobinkapoor100% (2)

- Statement of Cash Flow - SolutionDocument8 pagesStatement of Cash Flow - SolutionHân NabiNo ratings yet

- TASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraDocument4 pagesTASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraSincy MathewNo ratings yet

- UntitledDocument13 pagesUntitledTejasree SaiNo ratings yet

- HW5Document6 pagesHW5SHIVANI SHARMANo ratings yet

- Chapter 14Document13 pagesChapter 14VanessaFaithBiscaynoCalunodNo ratings yet

- Cash Flow Statements Interim Check 1 Yolo LTD Question and AnswerDocument5 pagesCash Flow Statements Interim Check 1 Yolo LTD Question and AnswerjunaidahNo ratings yet

- Statement of Cashflow: Tutor Class - 101 HUDA AULIA ARIFIN - 1406533781Document13 pagesStatement of Cashflow: Tutor Class - 101 HUDA AULIA ARIFIN - 1406533781Fiza Xiena100% (1)

- Financial statements analysisDocument3 pagesFinancial statements analysisFEBRI IRAWANNo ratings yet

- Interpretation of Public Sector Financial StatementsDocument4 pagesInterpretation of Public Sector Financial StatementsEsther AkpanNo ratings yet

- Question 1: Debit BalancesDocument9 pagesQuestion 1: Debit BalancesAsdfghjkl LkjhgfdsaNo ratings yet

- Solving - Business Finance 1-6Document28 pagesSolving - Business Finance 1-6Samson, Ma. Louise Ren A.No ratings yet

- Solution Cash FlowDocument7 pagesSolution Cash FlowritamNo ratings yet

- Philippine Christian University Solutions to Problems 5-B4 and 5-B5Document5 pagesPhilippine Christian University Solutions to Problems 5-B4 and 5-B5Coreen Andrade50% (2)

- Cash Flow AssignmentDocument39 pagesCash Flow AssignmentMUHAMMAD HASSANNo ratings yet

- MAS311 Financial Management Exercises Financial Statement AnalysisDocument4 pagesMAS311 Financial Management Exercises Financial Statement AnalysisLeanne QuintoNo ratings yet

- DauderisAnnand-IntroFinAcct-Chapter11 AmendedDocument15 pagesDauderisAnnand-IntroFinAcct-Chapter11 AmendedHome Made Cookin'No ratings yet

- TUGAS UTS INTERMEDIATE ACCOUNTING 1Document18 pagesTUGAS UTS INTERMEDIATE ACCOUNTING 121-010 Desi MailaniNo ratings yet

- FinanceDocument53 pagesFinanceSheethal RamachandraNo ratings yet

- Developing Project Cash Flow Statement: Lecture No. 23 Fundamentals of Engineering EconomicsDocument24 pagesDeveloping Project Cash Flow Statement: Lecture No. 23 Fundamentals of Engineering EconomicsAyman SobhyNo ratings yet

- HW5.FT222004.Archit KumarDocument7 pagesHW5.FT222004.Archit KumarARCHIT KUMARNo ratings yet

- Test 2 Financial - Analysis (Bervie Rondonuwu)Document5 pagesTest 2 Financial - Analysis (Bervie Rondonuwu)Bervie RondonuwuNo ratings yet

- Home Depot Balance SheetDocument4 pagesHome Depot Balance SheetNicolas ErnestoNo ratings yet

- Cash Flow Statement StudentDocument60 pagesCash Flow Statement StudentJanine MosatallaNo ratings yet

- 9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerDocument15 pages9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerMd SaifulNo ratings yet

- Business Finance ComputationsDocument10 pagesBusiness Finance ComputationsacegutierrezNo ratings yet

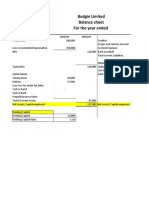

- Budgie Limited Balance Sheet and Profit & Loss AccountDocument6 pagesBudgie Limited Balance Sheet and Profit & Loss AccountAyazNo ratings yet

- Philippine School of Business Administration Midterm Exam AnalysisDocument4 pagesPhilippine School of Business Administration Midterm Exam AnalysisGrace Sinoy BastanteNo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Cash Flow AnalysisDocument19 pagesCash Flow AnalysisSarah GNo ratings yet

- Unit - II Module IIIDocument7 pagesUnit - II Module IIIpltNo ratings yet

- PERMALINO - Learning Activity 19. Working Capital ManagementDocument3 pagesPERMALINO - Learning Activity 19. Working Capital ManagementAra Joyce PermalinoNo ratings yet

- ACCA F9 Mock Examination 2Document5 pagesACCA F9 Mock Examination 2daria0% (1)

- 19 - Ch4 Weekly QuestionsDocument10 pages19 - Ch4 Weekly QuestionsCamilo ToroNo ratings yet

- Practice Problems Chapter 12 Corporate Cash Flow and Project AnalysisDocument57 pagesPractice Problems Chapter 12 Corporate Cash Flow and Project AnalysiszoeyNo ratings yet

- Special Accounting Topics For Business CombinationDocument4 pagesSpecial Accounting Topics For Business CombinationMixx MineNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Project Report IctDocument34 pagesProject Report Ictfizza amjadNo ratings yet

- Financial Statement Analysis of DellDocument14 pagesFinancial Statement Analysis of Dellfizza amjadNo ratings yet

- KMO and factor analysis of 15 items with 4 variablesDocument5 pagesKMO and factor analysis of 15 items with 4 variablesfizza amjadNo ratings yet

- Global Marketing Syllabus Emba563Document8 pagesGlobal Marketing Syllabus Emba563fizza amjadNo ratings yet

- MKT 600, Spring 2022 in Class Assignment: Student Name(s)Document1 pageMKT 600, Spring 2022 in Class Assignment: Student Name(s)fizza amjadNo ratings yet

- Walmart CaseDocument5 pagesWalmart Casefizza amjadNo ratings yet

- Fardapaper Impact of Information Technology Innovation On Firm Performance in KenyaDocument31 pagesFardapaper Impact of Information Technology Innovation On Firm Performance in Kenyafizza amjadNo ratings yet

- LO1 Explain The Different Types, Size and Scope of OrganizationsDocument14 pagesLO1 Explain The Different Types, Size and Scope of Organizationsfizza amjad0% (1)

- Bargaining Power of SuppliersDocument2 pagesBargaining Power of Suppliersfizza amjadNo ratings yet

- Planning: Topic 1: Management FunctionDocument9 pagesPlanning: Topic 1: Management Functionfizza amjadNo ratings yet

- KMO and factor analysis of 15 items with 4 variablesDocument5 pagesKMO and factor analysis of 15 items with 4 variablesfizza amjadNo ratings yet

- Carbon Footprints and Tourism in UAE Challenges Faced by Jumeirah Group and Its SolutionDocument11 pagesCarbon Footprints and Tourism in UAE Challenges Faced by Jumeirah Group and Its Solutionfizza amjadNo ratings yet

- Bargaining Power of SuppliersDocument2 pagesBargaining Power of Suppliersfizza amjadNo ratings yet

- Mubeen Task 6 JulyDocument8 pagesMubeen Task 6 Julyfizza amjadNo ratings yet

- Knowledge Sharing 2500 Payment ClearDocument11 pagesKnowledge Sharing 2500 Payment Clearfizza amjadNo ratings yet

- School ClubDocument1 pageSchool Clubfizza amjadNo ratings yet

- The Matrix of The FormDocument2 pagesThe Matrix of The Formfizza amjadNo ratings yet

- The Policy Making UpdatedDocument8 pagesThe Policy Making Updatedfizza amjadNo ratings yet

- ECO 221 - 2 - Assignment II - No AnswerDocument5 pagesECO 221 - 2 - Assignment II - No Answerfizza amjadNo ratings yet

- Umairah HotalDocument1 pageUmairah Hotalfizza amjadNo ratings yet

- The Following Year It Was Privatized by The Australian GovernmentDocument12 pagesThe Following Year It Was Privatized by The Australian Governmentfizza amjadNo ratings yet

- Data Analysis InsightsDocument17 pagesData Analysis Insightsfizza amjadNo ratings yet

- Answers To Final ExamsDocument42 pagesAnswers To Final Examsfizza amjadNo ratings yet

- Final ProjectDocument24 pagesFinal Projectfizza amjadNo ratings yet

- FIN4480 Resit Class Test Solutions 2018-19 Section A Solution Part A)Document4 pagesFIN4480 Resit Class Test Solutions 2018-19 Section A Solution Part A)fizza amjadNo ratings yet

- 1.1 The JRC Peseta Iii ProjectDocument10 pages1.1 The JRC Peseta Iii Projectfizza amjadNo ratings yet

- Ford mOTOR AND uNILEVERDocument14 pagesFord mOTOR AND uNILEVERfizza amjadNo ratings yet

- HONDASTRATEGICANALYSISDocument12 pagesHONDASTRATEGICANALYSISkalyan jenjuluriNo ratings yet

- Doument 2 EconomicsDocument4 pagesDoument 2 Economicsfizza amjadNo ratings yet

- Cost-Revenue Profit Functions (Using Linear Equations) PDFDocument5 pagesCost-Revenue Profit Functions (Using Linear Equations) PDFLibyaFlower100% (1)

- 2020-2021 Term 1 ECON2011A/B Problem Set 1Document4 pages2020-2021 Term 1 ECON2011A/B Problem Set 1Helen ToNo ratings yet

- Chapter 5Document6 pagesChapter 5ferdeefamousNo ratings yet

- Price Ceiling and FlooringDocument6 pagesPrice Ceiling and FlooringAditi Agarwal100% (1)

- 6 Inventory PDFDocument10 pages6 Inventory PDFJorufel PapasinNo ratings yet

- How To Think About Investing?: Jana VembunarayananDocument24 pagesHow To Think About Investing?: Jana VembunarayananMohamed Rajiv AshaNo ratings yet

- Measuring and Explaining InflationDocument23 pagesMeasuring and Explaining Inflationfahrah daudaNo ratings yet

- Bus Law 103 Midterm Exam QuestionsDocument9 pagesBus Law 103 Midterm Exam Questionsrandyblanza2014No ratings yet

- Math 12 BESR ABM Q2-Week 1Document28 pagesMath 12 BESR ABM Q2-Week 1Victoria Quebral CarumbaNo ratings yet

- C 03 Financial MathematicsDocument50 pagesC 03 Financial MathematicsmonsurNo ratings yet

- Unit 4 Pharma Jurisprudence One Shot NotesDocument13 pagesUnit 4 Pharma Jurisprudence One Shot NotessaurabhpkotkarNo ratings yet

- Australian Rental Market Discussion PaperDocument7 pagesAustralian Rental Market Discussion PaperBob odenkirkNo ratings yet

- Container Account TypesDocument9 pagesContainer Account TypesNelsonMoseM100% (3)

- Game ProposalDocument5 pagesGame ProposalZaryab KhanNo ratings yet

- Marketing Mix - A Study On Smart Group of CompaniesDocument50 pagesMarketing Mix - A Study On Smart Group of CompaniesMohammad Shahidul Islam100% (1)

- FIFO Inventory Valuation and CostingDocument14 pagesFIFO Inventory Valuation and Costingrizwan ul hassanNo ratings yet

- Wassce / Waec Economics Syllabus: PreambleDocument7 pagesWassce / Waec Economics Syllabus: PreambleMichael Asante NsiahNo ratings yet

- Using The Internet in The E-MarketingDocument7 pagesUsing The Internet in The E-Marketingusama ahmadNo ratings yet

- Microeconomics: by Michael J. Buckle, PHD, James Seaton, PHD, Sandeep Singh, PHD, Cfa, Cipim, and Stephen Thomas, PHDDocument28 pagesMicroeconomics: by Michael J. Buckle, PHD, James Seaton, PHD, Sandeep Singh, PHD, Cfa, Cipim, and Stephen Thomas, PHDDouglas ZimunyaNo ratings yet

- Foreign currency risk factorsDocument16 pagesForeign currency risk factorsHastings KapalaNo ratings yet

- Understanding the Importance of Elasticity ConceptsDocument3 pagesUnderstanding the Importance of Elasticity ConceptsRian EsperanzaNo ratings yet

- Standardised PPT On Revised Model GST LawDocument234 pagesStandardised PPT On Revised Model GST LawAnurag JoshiNo ratings yet

- DBB2101 Unit-04Document21 pagesDBB2101 Unit-04anamikarajendran441998No ratings yet

- PAS 29 - Financial Reporting in Hyperinflationary EconomiesDocument7 pagesPAS 29 - Financial Reporting in Hyperinflationary EconomiesKrizzia DizonNo ratings yet

- RESCISSION BY VENDOR AFTER DELIVERYDocument11 pagesRESCISSION BY VENDOR AFTER DELIVERYYannah Hidalgo100% (1)

- Event Planning - Business Model CanvasDocument1 pageEvent Planning - Business Model CanvasSai Ram Bachu75% (4)

- Chapter 3 MCQs and Analytical Qs Supply and DemandDocument8 pagesChapter 3 MCQs and Analytical Qs Supply and Demandhamna ikramNo ratings yet

- Solution Manual For Microeconomics 16th Canadian Edition Christopher T S Ragan Christopher RaganDocument13 pagesSolution Manual For Microeconomics 16th Canadian Edition Christopher T S Ragan Christopher RaganChristopherRamosfgzoNo ratings yet

- Foreign Exchange Rates ExplainedDocument8 pagesForeign Exchange Rates ExplainedTatenda UyaNo ratings yet

- BUS-113 Assignment PDFDocument7 pagesBUS-113 Assignment PDFhasin masudNo ratings yet