You might also like

- Banking Regulations Act, RBI Act, Ni ActDocument65 pagesBanking Regulations Act, RBI Act, Ni ActDeepak GuptaNo ratings yet

- RBI Act 1934 NDocument42 pagesRBI Act 1934 NRohit SinghNo ratings yet

- Banking Law and PracticeDocument89 pagesBanking Law and Practicethangarajbala123No ratings yet

- Full 500 QuestionsDocument64 pagesFull 500 QuestionsarunNo ratings yet

- FED Master Direction No. 5 External Commercial Borrowings, Trade Credit Dec 2021Document27 pagesFED Master Direction No. 5 External Commercial Borrowings, Trade Credit Dec 2021Prabhat SinghNo ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Cgtmse (Credit Guarantee Fund Trust For Micro & Small Enterprises)Document16 pagesCgtmse (Credit Guarantee Fund Trust For Micro & Small Enterprises)Abinash MandilwarNo ratings yet

- Certificate of DepositsDocument8 pagesCertificate of DepositsSweta SinghNo ratings yet

- OMB Form 8-K SEC FilingDocument22 pagesOMB Form 8-K SEC Filingg6hNo ratings yet

- Credit Derivatives and Structured Credit: A Guide for InvestorsFrom EverandCredit Derivatives and Structured Credit: A Guide for InvestorsNo ratings yet

- SEC Form 20-F Annual ReportDocument66 pagesSEC Form 20-F Annual ReportAndre KusumaNo ratings yet

- What Is The Difference Between Commercial Banking and Merchant BankingDocument8 pagesWhat Is The Difference Between Commercial Banking and Merchant BankingScarlett Lewis100% (2)

- Governor Generals - British IndiaDocument5 pagesGovernor Generals - British IndiaSriSriNo ratings yet

- Commercial Banks Functions and RBI RolesDocument5 pagesCommercial Banks Functions and RBI RolessnehaNo ratings yet

- Presentation On Export CreditDocument21 pagesPresentation On Export CreditArpit KhandelwalNo ratings yet

- BankingDocument29 pagesBankingKenneth Wilson BavachanNo ratings yet

- Erma AND MICR PowerpointDocument13 pagesErma AND MICR PowerpointJonathan Realis Capilo100% (1)

- Foreign Exchange-1Document32 pagesForeign Exchange-1Manu MaheshwariNo ratings yet

- Ijser: Banking: Definition and EvolutionDocument9 pagesIjser: Banking: Definition and EvolutionnehaNo ratings yet

- V V V V:) V) V5V$V VV V VV9V8) VVDocument2 pagesV V V V:) V) V5V$V VV V VV9V8) VVBhavneesh ShuklaNo ratings yet

- Law of Limitation in BankingDocument13 pagesLaw of Limitation in Bankingeknath2000100% (1)

- BLO Unit 1-1Document24 pagesBLO Unit 1-1Mohammad MAAZNo ratings yet

- Balance Sheet Management and ALM StrategiesDocument4 pagesBalance Sheet Management and ALM StrategiesakvgauravNo ratings yet

- National Law Institute University, Bhopal: Basics of E-BankingDocument21 pagesNational Law Institute University, Bhopal: Basics of E-BankingDikshaNo ratings yet

- Types of DepOSIT 15-18-21-22Document94 pagesTypes of DepOSIT 15-18-21-22Saurab JainNo ratings yet

- S-10 Banking Operations & Negotiable InstrumentsDocument21 pagesS-10 Banking Operations & Negotiable InstrumentsKshitij SharmaNo ratings yet

- RHB Personal Financing TermsDocument17 pagesRHB Personal Financing TermsDon LotNo ratings yet

- BRPD Circular No. 14-2012 - Master Circular On Loan Classification and ProvisioningDocument16 pagesBRPD Circular No. 14-2012 - Master Circular On Loan Classification and ProvisioningRifat Hasan Rathi100% (4)

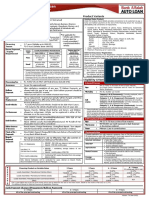

- Alfalah Auto Loan: Policy One PagerDocument1 pageAlfalah Auto Loan: Policy One PagerbilalasifNo ratings yet

- Principles and Practices of Banking - JAIIB: Timing: 3 HoursDocument20 pagesPrinciples and Practices of Banking - JAIIB: Timing: 3 HoursMallikarjuna RaoNo ratings yet

- Government Securities MarketDocument35 pagesGovernment Securities MarketPriyanka DargadNo ratings yet

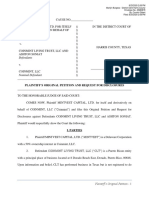

- Coinmint vs. Ashton Soniat Fraud CaseDocument8 pagesCoinmint vs. Ashton Soniat Fraud CaseDon HewlettNo ratings yet

- RBI Regulations and Banking ConceptsDocument30 pagesRBI Regulations and Banking ConceptsMuralidhar GoliNo ratings yet

- RFC Savings Account Guide: Key Features & BenefitsDocument6 pagesRFC Savings Account Guide: Key Features & BenefitsPrachikarambelkar100% (1)

- GSCFF Receivables Discounting Common PracticesDocument16 pagesGSCFF Receivables Discounting Common PracticesMaharaniNo ratings yet

- United States Securities and Exchange Commission Washington, D.C. 20549 Form 1-U Current Report Pursuant To Regulation ADocument8 pagesUnited States Securities and Exchange Commission Washington, D.C. 20549 Form 1-U Current Report Pursuant To Regulation AAnthony ANTONIO TONY LABRON ADAMSNo ratings yet

- SEBI Role and FunctionsDocument28 pagesSEBI Role and FunctionsAnurag Singh100% (4)

- Banking Regulation and LawsDocument6 pagesBanking Regulation and LawsDeepak SinghNo ratings yet

- Formation of Contracts TranscriptDocument13 pagesFormation of Contracts TranscriptLinh TinhNo ratings yet

- Negotiable Instruments Act of IndiaDocument164 pagesNegotiable Instruments Act of IndiaShome BhattacharjeeNo ratings yet

- Banking Law & Regulation (BBA 8th Sem) PDFDocument115 pagesBanking Law & Regulation (BBA 8th Sem) PDFsuresh pathakNo ratings yet

- Assignments: Banking and FinanceDocument19 pagesAssignments: Banking and FinanceAamir Hussian100% (1)

- Treasury Single Account (TSA) As A Strategy For Blocking Revenue LeakagesDocument20 pagesTreasury Single Account (TSA) As A Strategy For Blocking Revenue LeakagesLearning SystemNo ratings yet

- 4 Banking Operations - AFB - Module DDocument44 pages4 Banking Operations - AFB - Module Dwaste mailNo ratings yet

- FINTELLIGENCE 6 12 March 2014 Step by Step Guide To NCD IssuanceDocument5 pagesFINTELLIGENCE 6 12 March 2014 Step by Step Guide To NCD IssuanceAnkit SharmaNo ratings yet

- Minor AccountDocument12 pagesMinor AccountAshwini Venugopal100% (1)

- Fundamental of BankingDocument55 pagesFundamental of BankingSubodh RoyNo ratings yet

- Banking Correspondence ToolsDocument35 pagesBanking Correspondence Toolsmanjusha148825% (4)

- Payment Application Form: Applicant'S ParticularsDocument2 pagesPayment Application Form: Applicant'S ParticularsVijay PuramNo ratings yet

- UCP600Document21 pagesUCP600MingHDynasty100% (1)

- Securities Laws - Only This MuchDocument9 pagesSecurities Laws - Only This MuchOnly This Much100% (2)

- International Remittances: Business Process Outsourcing Consulting System Integration Universal Banking SolutionDocument11 pagesInternational Remittances: Business Process Outsourcing Consulting System Integration Universal Banking Solutionakther_aisNo ratings yet

- A Project Report On: Under The Supervision Of: Submitted By: MD - SageerDocument46 pagesA Project Report On: Under The Supervision Of: Submitted By: MD - Sageerdev42No ratings yet

- UNESCO - Debt Conversion Development Bonds - 2012Document12 pagesUNESCO - Debt Conversion Development Bonds - 2012Daniel BondNo ratings yet

- Partnership Related DocumentsDocument1 pagePartnership Related DocumentsSonalNo ratings yet

- Chasebankusanationalassociation 489913 Wilmingtondelaware 19Document39 pagesChasebankusanationalassociation 489913 Wilmingtondelaware 19Efrain CabreraNo ratings yet

- Policy on Fair Practices CodeDocument5 pagesPolicy on Fair Practices CodeMANOJIT GAINNo ratings yet

- Seminar7 Group Discussion1cDocument55 pagesSeminar7 Group Discussion1cMytee TarasonNo ratings yet

- CompendiumDocument18 pagesCompendiumpranithroyNo ratings yet

- Relationship Between Banker and CustomerDocument10 pagesRelationship Between Banker and Customerswagat098No ratings yet

- Preliminary Cost Estimate For Product Cost CollectorDocument2 pagesPreliminary Cost Estimate For Product Cost CollectorBalanathan VirupasanNo ratings yet

- Organization Development in Global SettingDocument3 pagesOrganization Development in Global Settinghijkayelmnop50% (2)

- Sop 1Document3 pagesSop 1elnionlineNo ratings yet

- Reading Sample Sappress 1517 Procurement With SAP MM Business User GuideDocument47 pagesReading Sample Sappress 1517 Procurement With SAP MM Business User GuideEdu RonanNo ratings yet

- Unit 2 Illustration ProblemDocument1 pageUnit 2 Illustration ProblemCharlene RodrigoNo ratings yet

- Protection of Registered Trademarks Against Trademarks Not Registered in Certain Classes - IPleadersDocument14 pagesProtection of Registered Trademarks Against Trademarks Not Registered in Certain Classes - IPleadersAbhik SahaNo ratings yet

- Bayer CropScience Limited 2021-22 - Web Upload (17 MB) - IndiaDocument192 pagesBayer CropScience Limited 2021-22 - Web Upload (17 MB) - IndiaAadarsh jainNo ratings yet

- tAX FINALSDocument8 pagestAX FINALSAmie Jane MirandaNo ratings yet

- Skill Development, Theories of Learning, Technology IntelligenceDocument7 pagesSkill Development, Theories of Learning, Technology IntelligencePankajNo ratings yet

- CRM Initiatives at 3M PDFDocument10 pagesCRM Initiatives at 3M PDFPradumna KasaudhanNo ratings yet

- VDA Volume 6.3 Chapter 9.1 Process Audit Evaluation PDFDocument1 pageVDA Volume 6.3 Chapter 9.1 Process Audit Evaluation PDFalliceyewNo ratings yet

- Employee Engagement ReportDocument51 pagesEmployee Engagement Reportradhika100% (1)

- Zodius Capital II Fund Launch 070414Document2 pagesZodius Capital II Fund Launch 070414avendusNo ratings yet

- EWC EWM93 Process Overview en XXDocument7 pagesEWC EWM93 Process Overview en XXJoaquin GonzalezNo ratings yet

- Coatue Management - East Meets West EMW Deck 22 24 June 2023 RosewoodDocument46 pagesCoatue Management - East Meets West EMW Deck 22 24 June 2023 RosewoodAlex ArtemyevNo ratings yet

- Tatmeen Onboarding Presentation For MAH, Licensed Agents, and 3PLsDocument53 pagesTatmeen Onboarding Presentation For MAH, Licensed Agents, and 3PLsJaweed SheikhNo ratings yet

- DrVijayMalik Company Analyses Vol 1Document241 pagesDrVijayMalik Company Analyses Vol 1padmaniaNo ratings yet

- English Shva - 2020 FSDocument184 pagesEnglish Shva - 2020 FSSimonasNo ratings yet

- TNEB Online PaymentDocument1 pageTNEB Online PaymentShaha budeenNo ratings yet

- The Official PRINCE2 Agile Accreditor Sample Examination Papers Terms of UseDocument24 pagesThe Official PRINCE2 Agile Accreditor Sample Examination Papers Terms of UseFriendNo ratings yet

- Hazard & Incident Reporting Procedure - HS307Document8 pagesHazard & Incident Reporting Procedure - HS307Vertical CubeNo ratings yet

- Elite Paint HRM 410Document33 pagesElite Paint HRM 410Tasmia Loona0% (2)

- Questions About The Case Study: ELE PLCDocument2 pagesQuestions About The Case Study: ELE PLCMicaela Hidalgo RamírezNo ratings yet

- Car Sale AgreementDocument1 pageCar Sale AgreementMuhammad Abdullah basit KhanNo ratings yet

- Management Accounting NotesDocument9 pagesManagement Accounting NoteskamdicaNo ratings yet

- NML Test 3Document3 pagesNML Test 3milenamusovskaNo ratings yet

- Share PerformanceTask BDocument5 pagesShare PerformanceTask BMariela PelaezNo ratings yet

- Value PropositionDocument2 pagesValue PropositionasghNo ratings yet

- SAP Procurement CertificationDocument6 pagesSAP Procurement CertificationFerhanMalik0% (1)

- Cost Concepts, Classification and Analysis: Practice ExerciseDocument9 pagesCost Concepts, Classification and Analysis: Practice ExerciseKuya ANo ratings yet