You might also like

- PIE Auditor Registration Regulations: Practice Note 14Document25 pagesPIE Auditor Registration Regulations: Practice Note 14Abdelmadjid djibrineNo ratings yet

- RAPS QCI Document PDFDocument124 pagesRAPS QCI Document PDFSurya Teja SarmaNo ratings yet

- ISA 210 Agreeing The Terms of Audit EngagementsDocument6 pagesISA 210 Agreeing The Terms of Audit EngagementsBilal RazaNo ratings yet

- Licensing ProceduresDocument37 pagesLicensing ProceduresDlamini SiceloNo ratings yet

- SBI Annexure - A: Empanelment of CA Firms as Concurrent AuditorsDocument55 pagesSBI Annexure - A: Empanelment of CA Firms as Concurrent AuditorsRamesh gopeNo ratings yet

- Registration TermsDocument6 pagesRegistration Termsmrthilagam100% (1)

- Guidelines in The Omnibus Investments Code of 1987Document4 pagesGuidelines in The Omnibus Investments Code of 1987Vince AbucejoNo ratings yet

- FRC Nigeria Audit Regulations 2020 SummaryDocument29 pagesFRC Nigeria Audit Regulations 2020 SummaryTaiwo OretugaNo ratings yet

- Preliminary Engagement ActivitiesDocument4 pagesPreliminary Engagement ActivitiesZafar IqbalNo ratings yet

- Start-Up Schemes Details MKDocument5 pagesStart-Up Schemes Details MKRaz NawadwiNo ratings yet

- FILING GUIDELINES FOR INVESTMENT REGISTRATIONDocument4 pagesFILING GUIDELINES FOR INVESTMENT REGISTRATIONGabe RuaroNo ratings yet

- Guidance-noteLondon Stock ExchangeDocument16 pagesGuidance-noteLondon Stock ExchangeSky walkingNo ratings yet

- EIC Inspection Agency Recognition SchemeDocument8 pagesEIC Inspection Agency Recognition Schemesantoshelapanda9167No ratings yet

- SBI empanelment of CA firms as concurrent auditorsDocument33 pagesSBI empanelment of CA firms as concurrent auditorsShadab Malik67% (3)

- (Req-MOZ-2024-017) - 04 - Sections II, III, IV, VDocument40 pages(Req-MOZ-2024-017) - 04 - Sections II, III, IV, VLeonardo nguenhaNo ratings yet

- Guide Registrar RFQDocument14 pagesGuide Registrar RFQabbeyjvNo ratings yet

- TenderDocument16 pagesTenderAr. Shadab SaifiNo ratings yet

- Resolution Plan - Meaning, Content, Drafting and SubmissionDocument3 pagesResolution Plan - Meaning, Content, Drafting and SubmissionAnkit SinghNo ratings yet

- Result Gazette SBDDocument40 pagesResult Gazette SBDSalma noureenNo ratings yet

- Final - Adv Auditing (O) - Suggested AnsDocument14 pagesFinal - Adv Auditing (O) - Suggested AnsPraveen Reddy DevanapalleNo ratings yet

- gem bid ruleDocument33 pagesgem bid ruleSunil KumarNo ratings yet

- CDA guidelines for cooperative external auditor accreditationDocument11 pagesCDA guidelines for cooperative external auditor accreditationAndres Lorenzo III50% (2)

- Audit RPT Nov 19Document44 pagesAudit RPT Nov 19himanshurjrNo ratings yet

- PBD ConsultancyDocument129 pagesPBD ConsultancyNes-tValdezNo ratings yet

- Odisha Hydro Power Corporation EOIDocument12 pagesOdisha Hydro Power Corporation EOISoumyaranjan SinghNo ratings yet

- PR3C FSSC 22000Document17 pagesPR3C FSSC 22000faiza chenkirNo ratings yet

- Detailed Summary OF Performance Task NO.1: College of Engineering, Architecture, and TechnologyDocument12 pagesDetailed Summary OF Performance Task NO.1: College of Engineering, Architecture, and TechnologyEdbert PajaritoNo ratings yet

- The County Government On Nyeri: Item Description: Repairs and Maintenance ofDocument23 pagesThe County Government On Nyeri: Item Description: Repairs and Maintenance ofAkuku SamNo ratings yet

- skills-development-provider-and-assessment-centre-criteria-and-guidelinesDocument10 pagesskills-development-provider-and-assessment-centre-criteria-and-guidelinesDonald CageNo ratings yet

- ADVANCED AUDITING AND PROFESSIONAL ETHICS-3 ADocument26 pagesADVANCED AUDITING AND PROFESSIONAL ETHICS-3 ACAtestseriesNo ratings yet

- Prequalification Document Automation of NJHPC's Operation: ThroughDocument15 pagesPrequalification Document Automation of NJHPC's Operation: Through3J Solutions BDNo ratings yet

- Nabl 152Document12 pagesNabl 152shahpinkalNo ratings yet

- Session 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureDocument88 pagesSession 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureVaibhav JainNo ratings yet

- Archi AuditDocument65 pagesArchi AuditAnilGoyalNo ratings yet

- R.A 9184 - Procurement of Infrastructure Projects PDFDocument7 pagesR.A 9184 - Procurement of Infrastructure Projects PDFMary Joy RuilesNo ratings yet

- QCI Application for IndiaGHP and HACCP CertificationDocument6 pagesQCI Application for IndiaGHP and HACCP CertificationMonica SinghNo ratings yet

- Frequently Asked Questions For RQFII SingaporeDocument2 pagesFrequently Asked Questions For RQFII SingaporeMuhammad AnasNo ratings yet

- Philippine Standard On Related Services 4400Document10 pagesPhilippine Standard On Related Services 4400JecNo ratings yet

- Philippine Auditing Standards on Agreed-Upon Procedures EngagementsDocument14 pagesPhilippine Auditing Standards on Agreed-Upon Procedures EngagementsTeresa RevilalaNo ratings yet

- Philippine Bidding DocumentsDocument127 pagesPhilippine Bidding Documentsb.cuevas15No ratings yet

- RG 01 Rev 00 - Guidelines For The Registration of Conformity Assessment Bodies (CABs) in UAEDocument6 pagesRG 01 Rev 00 - Guidelines For The Registration of Conformity Assessment Bodies (CABs) in UAEAnonymous G6ceYCzwtNo ratings yet

- Finalactivity BatistisDocument5 pagesFinalactivity BatistisPhoebe MagnoNo ratings yet

- Page 1 of 3Document3 pagesPage 1 of 3Shyam SunderNo ratings yet

- SIFMA Letter On QI Agreement 3-23-20 FINALDocument7 pagesSIFMA Letter On QI Agreement 3-23-20 FINALABC DEFNo ratings yet

- Microsoft Word - Terms and ConditionsDocument3 pagesMicrosoft Word - Terms and ConditionsIsaac SamuelNo ratings yet

- 50672rmo 39-2010Document4 pages50672rmo 39-2010Quinnie PiolNo ratings yet

- Post QualificationDocument4 pagesPost QualificationGie Bernal CamachoNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument32 pages© The Institute of Chartered Accountants of Indiasurbhi jainNo ratings yet

- HKSRS 4400 Procedures Financial InformationDocument8 pagesHKSRS 4400 Procedures Financial InformationAgus WijayaNo ratings yet

- Final-Decision-Notice-Sanctions-against-PwC-in-relation-to-PwC’s-audit-of-Kier-07-06-22Document46 pagesFinal-Decision-Notice-Sanctions-against-PwC-in-relation-to-PwC’s-audit-of-Kier-07-06-22TomNo ratings yet

- Standard Operating Procedure: 2 Floor, OPF Building G-5/2 IslamabadDocument17 pagesStandard Operating Procedure: 2 Floor, OPF Building G-5/2 IslamabadShahid SiddiqueNo ratings yet

- Technical ReleaseDocument35 pagesTechnical ReleasezilchhourNo ratings yet

- RFP Audit and Certification ISO 22301 & 27001 March 20222022-03-07 102425519Document50 pagesRFP Audit and Certification ISO 22301 & 27001 March 20222022-03-07 102425519umangmehtaNo ratings yet

- IAF MD 15 CB Indicators Issue 11407 2014 PublicationVersionDocument8 pagesIAF MD 15 CB Indicators Issue 11407 2014 PublicationVersionFrehedernandNo ratings yet

- Model ITT Marine ConstructionDocument62 pagesModel ITT Marine ConstructionRio HandokoNo ratings yet

- General Rules Certification ServicesDocument18 pagesGeneral Rules Certification ServicesrookhnNo ratings yet

- 47 Repair of Generators Equipment Machinery and Plants 1Document22 pages47 Repair of Generators Equipment Machinery and Plants 1Akuku SamNo ratings yet

- Small Works RFQ Section II III IV VDocument22 pagesSmall Works RFQ Section II III IV VAiman AliNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Letter From Committee On Wages and Hours American Institute of ADocument4 pagesLetter From Committee On Wages and Hours American Institute of AAbdelmadjid djibrineNo ratings yet

- Crosswalk Sqms 1 Sqcs 8Document15 pagesCrosswalk Sqms 1 Sqcs 8Abdelmadjid djibrineNo ratings yet

- Business Technology Report 2023 - FinalDocument49 pagesBusiness Technology Report 2023 - FinalAbdelmadjid djibrineNo ratings yet

- Letter From Scovell Wellington & Company To Members of The AmeriDocument2 pagesLetter From Scovell Wellington & Company To Members of The AmeriAbdelmadjid djibrineNo ratings yet

- USDA Food Insecurity Programs - Barriers & Policy RecommendationsDocument2 pagesUSDA Food Insecurity Programs - Barriers & Policy RecommendationsAbdelmadjid djibrineNo ratings yet

- Journal of Accountancy July 1913 Vol. 15 Issue 1 (Whole Issue)Document97 pagesJournal of Accountancy July 1913 Vol. 15 Issue 1 (Whole Issue)Abdelmadjid djibrineNo ratings yet

- Uniform CPA Examination May 1981-May 1985 Selected Questions &Document647 pagesUniform CPA Examination May 1981-May 1985 Selected Questions &Abdelmadjid djibrineNo ratings yet

- 33 11092Document13 pages33 11092Abdelmadjid djibrineNo ratings yet

- Request For Information On Digital AssetsDocument2 pagesRequest For Information On Digital AssetsZerohedgeNo ratings yet

- Summary Note of The Accounting Standards Advisory Forum: Region MembersDocument32 pagesSummary Note of The Accounting Standards Advisory Forum: Region MembersAbdelmadjid djibrineNo ratings yet

- Federal Reserve Board Orders $9.5M Penalty for EagleBank Regulation ViolationsDocument5 pagesFederal Reserve Board Orders $9.5M Penalty for EagleBank Regulation ViolationsAbdelmadjid djibrineNo ratings yet

- A Crypto-Asset Generally Refers To Any Digital Asset Implemented Using Cryptographic TechniquesDocument4 pagesA Crypto-Asset Generally Refers To Any Digital Asset Implemented Using Cryptographic TechniquesAbdelmadjid djibrineNo ratings yet

- RG Primer On GHG Emissions Management Systems August 2018Document29 pagesRG Primer On GHG Emissions Management Systems August 2018Abdelmadjid djibrineNo ratings yet

- Sharpening The Focus On FraudDocument28 pagesSharpening The Focus On FraudAbdelmadjid djibrineNo ratings yet

- Spotlight: Audit Committee ResourceDocument5 pagesSpotlight: Audit Committee ResourceAbdelmadjid djibrineNo ratings yet

- Comp pr2022 146Document13 pagesComp pr2022 146Abdelmadjid djibrineNo ratings yet

- AICPA Service Center Training GuideDocument18 pagesAICPA Service Center Training GuideAbdelmadjid djibrineNo ratings yet

- Practice Note 14: Public Interest Entity (PIE) Auditor Registration RegulationsDocument46 pagesPractice Note 14: Public Interest Entity (PIE) Auditor Registration RegulationsAbdelmadjid djibrineNo ratings yet

- SEC Charges Auditors for Failing to Identify Goodwill Impairment Issues at Sequential BrandsDocument30 pagesSEC Charges Auditors for Failing to Identify Goodwill Impairment Issues at Sequential BrandsAbdelmadjid djibrineNo ratings yet

- Enf 20220816 A 2Document6 pagesEnf 20220816 A 2Abdelmadjid djibrineNo ratings yet

- 34 95223Document3 pages34 95223Abdelmadjid djibrineNo ratings yet

- 34 95193Document10 pages34 95193Abdelmadjid djibrineNo ratings yet

- Audit Firm Governance Code: Practice Note 14Document22 pagesAudit Firm Governance Code: Practice Note 14Abdelmadjid djibrineNo ratings yet

- 34 95076Document8 pages34 95076Abdelmadjid djibrineNo ratings yet

- FINAL DECISION NOTICE Sanctions Against UHY Hacker Young and Martin Jones in Relation To Laura Ashley Holdings 13 07 22Document67 pagesFINAL DECISION NOTICE Sanctions Against UHY Hacker Young and Martin Jones in Relation To Laura Ashley Holdings 13 07 22Abdelmadjid djibrineNo ratings yet

- See Accounting and Auditing Enforcement Release No. 2958, Dated March 30, 2009Document2 pagesSee Accounting and Auditing Enforcement Release No. 2958, Dated March 30, 2009Abdelmadjid djibrineNo ratings yet

- Practice Note 14: Position PaperDocument14 pagesPractice Note 14: Position PaperAbdelmadjid djibrineNo ratings yet

- Restoring Trust in Audit and Corporate Governance Govt ResponseDocument197 pagesRestoring Trust in Audit and Corporate Governance Govt ResponseAbdelmadjid djibrineNo ratings yet

- Case Chapter 8Document3 pagesCase Chapter 8Safwan MundaNo ratings yet

- McKee Tort NoticeDocument9 pagesMcKee Tort NoticeMegan BantaNo ratings yet

- Memorandum of Understanding (MOU) - Prima Lab SADocument5 pagesMemorandum of Understanding (MOU) - Prima Lab SAAyesha Akhtar100% (1)

- Lesson Plan Information Sheet: General Review of The MPM Version Date: 07/30/2012Document34 pagesLesson Plan Information Sheet: General Review of The MPM Version Date: 07/30/2012AnandaMandalNo ratings yet

- Public Corporation Mid-Term Examination IDocument1 pagePublic Corporation Mid-Term Examination ICedrick Contado Susi BocoNo ratings yet

- JNT List of Transaction SampleDocument133 pagesJNT List of Transaction SamplemoymoyNo ratings yet

- Crim Rev Digest Case Assignment Title 78Document7 pagesCrim Rev Digest Case Assignment Title 78Jan Lawrence OlacoNo ratings yet

- COMELEC Ruling on Certificate of Candidacy ChallengeDocument16 pagesCOMELEC Ruling on Certificate of Candidacy ChallengeMark John Geronimo BautistaNo ratings yet

- Philippine National Police, Police Regional Office Calabarzon Cavite Police Provincial Office Imus City Police StationDocument3 pagesPhilippine National Police, Police Regional Office Calabarzon Cavite Police Provincial Office Imus City Police StationJam JamNo ratings yet

- Fort Bonifacio Development Corporation Vs Sorongon and FongDocument1 pageFort Bonifacio Development Corporation Vs Sorongon and Fongjoy dayagNo ratings yet

- CBL Consent&CoercionDocument2 pagesCBL Consent&Coercionalice jiahuiiNo ratings yet

- Exclusive License for "This ain't what you wantDocument2 pagesExclusive License for "This ain't what you wantGavin PaulNo ratings yet

- LEGAL MAXIMS AND PHRASES FOR CLAT, JUDICIARY AND LAW EXAMSDocument14 pagesLEGAL MAXIMS AND PHRASES FOR CLAT, JUDICIARY AND LAW EXAMSAshhab Khan100% (2)

- IBC Knowledge Capsule on Framework for Personal GuarantorsDocument8 pagesIBC Knowledge Capsule on Framework for Personal GuarantorsprdyumnNo ratings yet

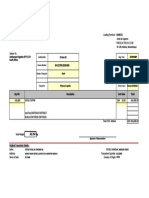

- Commercial Invoice TitleDocument1 pageCommercial Invoice Titlealsone07No ratings yet

- Property LawDocument115 pagesProperty Law04 Abhijith P KerantakathNo ratings yet

- EPP1-ZLT2BW5W-Passport Application FormDocument5 pagesEPP1-ZLT2BW5W-Passport Application FormJimmi WNo ratings yet

- Environmental Marketing Legal Aspects GuideDocument3 pagesEnvironmental Marketing Legal Aspects GuidemrycojesNo ratings yet

- Letter To Marcos and Hild Re Proposed Rule - 12.4.23 For TRANSMITTALDocument6 pagesLetter To Marcos and Hild Re Proposed Rule - 12.4.23 For TRANSMITTALTLNo ratings yet

- Gamboa vs. Teves, G.R. No. 176579, June 28, 2011Document2 pagesGamboa vs. Teves, G.R. No. 176579, June 28, 2011Jeorge Verba100% (1)

- Asmita Gaha Magar InsuranceDocument6 pagesAsmita Gaha Magar InsuranceNikhil Visa ServicesNo ratings yet

- Nicholas Cosmo of Agape World - 1997 Criminal ComplaintDocument13 pagesNicholas Cosmo of Agape World - 1997 Criminal ComplaintBrian WillinghamNo ratings yet

- Vivifi India Finance PVT LTDDocument5 pagesVivifi India Finance PVT LTDRamesh yaraboluNo ratings yet

- The Budget Process-Cabilangan Crispin JayDocument3 pagesThe Budget Process-Cabilangan Crispin JayJerico ManaloNo ratings yet

- Laoang CIS Project Completion ReportDocument7 pagesLaoang CIS Project Completion ReportJeline ReyesNo ratings yet

- Tax Invoice TN2200314988 Original For Recipient: Sold-ToDocument4 pagesTax Invoice TN2200314988 Original For Recipient: Sold-ToG Sandeep BelurNo ratings yet

- Volvo Clutch Wear CheckDocument3 pagesVolvo Clutch Wear ChecksengottaiyanNo ratings yet

- WebDocument134 pagesWebAmase Kis Ser100% (1)

- Unit 5 Democratic InterventionsDocument24 pagesUnit 5 Democratic InterventionsCristina Marie ManceraNo ratings yet

- Mirasol V DPWHDocument2 pagesMirasol V DPWHJeffrey Ahmed SampulnaNo ratings yet