You might also like

- Economics-1 1Document11 pagesEconomics-1 1hannah mae tabanaoNo ratings yet

- Engineering Economy: Simple Interest Effective Rate of InterestDocument10 pagesEngineering Economy: Simple Interest Effective Rate of InterestPaul Gerard AguilarNo ratings yet

- Bicol University College of Engineering Civil Engineering DepartmentDocument4 pagesBicol University College of Engineering Civil Engineering DepartmentJannel Llanillo JamisolaNo ratings yet

- Economics 1Document12 pagesEconomics 1jhozabethcarbonelNo ratings yet

- AnnuityDocument29 pagesAnnuityChristed aljo barroga100% (1)

- 3 Compound InterestDocument3 pages3 Compound InterestJohn Carlo Andales LumabasNo ratings yet

- ECONOMICSDocument12 pagesECONOMICSJenielle SisonNo ratings yet

- CALCULATING ANNUITIES AND FUTURE VALUESDocument10 pagesCALCULATING ANNUITIES AND FUTURE VALUESLyzette LeanderNo ratings yet

- Chapter 3 Understanding Money and Its Management Last PartDocument28 pagesChapter 3 Understanding Money and Its Management Last PartSarah Mae WenceslaoNo ratings yet

- Module 2 FactorsDocument45 pagesModule 2 FactorsMeifrinaldiGamaBizenNo ratings yet

- GE301 Chap2.2 Compund Interest Part 1 InterestDocument6 pagesGE301 Chap2.2 Compund Interest Part 1 InterestdablackmambaNo ratings yet

- Chapter 2Document26 pagesChapter 2TSARNo ratings yet

- 411_Chapter02_66-761520-16911405009257Document85 pages411_Chapter02_66-761520-16911405009257Ken TheeraNo ratings yet

- Factors: How Time and Interest Affect MoneyDocument62 pagesFactors: How Time and Interest Affect MoneyGörkem DamdereNo ratings yet

- Lesson 6 Compound InterestDocument14 pagesLesson 6 Compound InterestDaniela CaguioaNo ratings yet

- Chapter 2 - Interest and Money Time Relationships Week 4Document5 pagesChapter 2 - Interest and Money Time Relationships Week 4Jouryel Ian Roy TapongotNo ratings yet

- Module 3Document5 pagesModule 3RyuddaenNo ratings yet

- Time Value of Money: Economic Basis To Evaluate Engineering ProjectsDocument43 pagesTime Value of Money: Economic Basis To Evaluate Engineering ProjectsFajriansyah Herawan PangestuNo ratings yet

- Module 3 InterestDocument11 pagesModule 3 InterestGurtejSinghChana100% (1)

- Annual Compounding Factors and CalculationsDocument24 pagesAnnual Compounding Factors and CalculationsJim LindaNo ratings yet

- Engineering EconomicsDocument10 pagesEngineering EconomicsrenegadeNo ratings yet

- Solved Problems in Engineering Economy 2014 PDFDocument61 pagesSolved Problems in Engineering Economy 2014 PDFAngela Lapuz100% (1)

- Calculate Cost of Goods with InflationDocument4 pagesCalculate Cost of Goods with InflationKean LonggayNo ratings yet

- Multiple Compounding Periods in A Year: Example: Credit Card DebtDocument36 pagesMultiple Compounding Periods in A Year: Example: Credit Card DebtnorahNo ratings yet

- Econ 101E (Module 3) Hand-Out Money-Time Relationship 1st Sem 2020-2021Document5 pagesEcon 101E (Module 3) Hand-Out Money-Time Relationship 1st Sem 2020-2021May May MagluyanNo ratings yet

- Presentation 2 Simple Interest Compound Interest 2Document22 pagesPresentation 2 Simple Interest Compound Interest 2Qwertyuiop QwertyuiopNo ratings yet

- (4-1) Future Value (FV) Single-Payment Compound Amount FormulaDocument6 pages(4-1) Future Value (FV) Single-Payment Compound Amount FormulaMr sfeanNo ratings yet

- Lecture 2 - How Time and Interest Affect MoneyDocument50 pagesLecture 2 - How Time and Interest Affect MoneyDanar AdityaNo ratings yet

- Engineering Economics: Factor Name Converts Symbol FormulaDocument7 pagesEngineering Economics: Factor Name Converts Symbol FormulaJowel MercadoNo ratings yet

- Engineering Economics Excerpt From FE Reference PDFDocument7 pagesEngineering Economics Excerpt From FE Reference PDFBo Han HuangNo ratings yet

- Solved Problems in Engineering Economy 2016 - CompressDocument61 pagesSolved Problems in Engineering Economy 2016 - CompressCol. Jerome Carlo Magmanlac, ACP100% (1)

- Inflation & AnnuityDocument3 pagesInflation & AnnuityEstera ShawnNo ratings yet

- Simple Interest CalculatorDocument13 pagesSimple Interest Calculatorjm mNo ratings yet

- Formulas: F - Future Value P - Present/Principal ValueDocument2 pagesFormulas: F - Future Value P - Present/Principal ValueJimuel Ace SarmientoNo ratings yet

- Factors: How Time and Interest Affect MoneyDocument64 pagesFactors: How Time and Interest Affect MoneyOrangeNo ratings yet

- Factors: How Time and Interest Affect Money: Engineering EconomyDocument33 pagesFactors: How Time and Interest Affect Money: Engineering Economymudassir ahmadNo ratings yet

- Chapter 2 Engineering EconomyDocument33 pagesChapter 2 Engineering Economymudassir ahmadNo ratings yet

- Lecture 2-Factors - UquDocument43 pagesLecture 2-Factors - UquKreemNo ratings yet

- FE Reference PagesDocument7 pagesFE Reference PagesCarolyn BaezNo ratings yet

- Business Investment Appraisal (3375)Document54 pagesBusiness Investment Appraisal (3375)Armudin PurbaNo ratings yet

- Compund Interest TablesDocument18 pagesCompund Interest TablesCindy HosianiNo ratings yet

- Compund Interest TablesDocument18 pagesCompund Interest TablesAnna DewiNo ratings yet

- Time Value of MoneyDocument4 pagesTime Value of MoneyaKSHAT sHARMANo ratings yet

- Econ 101E (Hand-Out 2) 2019-Money-Time RelationshipDocument13 pagesEcon 101E (Hand-Out 2) 2019-Money-Time RelationshipFrancisco CarbonNo ratings yet

- Annuities - A Series of Equal Payments Occurring at Equal Periods of TimeDocument5 pagesAnnuities - A Series of Equal Payments Occurring at Equal Periods of TimeMarcial MilitanteNo ratings yet

- Types of Annuities - Engineering EconomyDocument9 pagesTypes of Annuities - Engineering EconomySeungcheol ChoiNo ratings yet

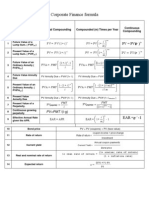

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Em5 Lesson 3 Economic Study MethodDocument7 pagesEm5 Lesson 3 Economic Study MethodParisNo ratings yet

- Economy FORMULASDocument5 pagesEconomy FORMULASRichard CalpitoNo ratings yet

- InterestsDocument3 pagesInterestsEstera ShawnNo ratings yet

- CE 561 Lecture Notes: Engineering Economic AnalysisDocument21 pagesCE 561 Lecture Notes: Engineering Economic AnalysisIyoi ShumiNo ratings yet

- FYI: For Your Interest!Document8 pagesFYI: For Your Interest!Aguila AlvinNo ratings yet

- Genmath Las Week1-2Document13 pagesGenmath Las Week1-2Aguila AlvinNo ratings yet

- Cash-Flow Analysis: Ekonomi Rekayas ADocument38 pagesCash-Flow Analysis: Ekonomi Rekayas ANurrohim SyukriNo ratings yet

- The Time Value of Money Continuous Compounding Discount InflationDocument21 pagesThe Time Value of Money Continuous Compounding Discount InflationSTEVE DOMINIC SISNONo ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Week 3 - DLP4Document4 pagesWeek 3 - DLP4JM CopinoNo ratings yet

- Reading & Writing PT3: Character Trait OrganizeDocument1 pageReading & Writing PT3: Character Trait OrganizeJM CopinoNo ratings yet

- PT#4 Copino, Jackielou Marie, 11-STEM 9ADocument1 pagePT#4 Copino, Jackielou Marie, 11-STEM 9AJM CopinoNo ratings yet

- PT#3 Copino, Jackielou Marie, 11-STEM 9ADocument2 pagesPT#3 Copino, Jackielou Marie, 11-STEM 9AJM CopinoNo ratings yet

- Affinity Laws and CompressorsDocument26 pagesAffinity Laws and CompressorsJM CopinoNo ratings yet

- COPINO, Jenie Marl A. ZGE 1108 - ME1 Introspective EssayDocument2 pagesCOPINO, Jenie Marl A. ZGE 1108 - ME1 Introspective EssayJM CopinoNo ratings yet

- CMS F014 - Document Retention and Disposal RequirementsDocument2 pagesCMS F014 - Document Retention and Disposal RequirementsIT Support - FernanNo ratings yet

- 2020-11-30 Affidavit of Portland Regional Chamber of CommerceDocument3 pages2020-11-30 Affidavit of Portland Regional Chamber of CommerceNEWS CENTER MaineNo ratings yet

- Bricks and Clicks vs. E-Tailing: Comparing Best Buy andDocument19 pagesBricks and Clicks vs. E-Tailing: Comparing Best Buy andapi-66679454No ratings yet

- Analisis Keuangan PershDocument8 pagesAnalisis Keuangan PershMeilinda AryantoNo ratings yet

- MBA 231 Marketing Management PDFDocument16 pagesMBA 231 Marketing Management PDFSNEHA SIVAKUMAR 1730152No ratings yet

- Visual Inspection Report FormDocument2 pagesVisual Inspection Report Formrosid_alhusna60% (5)

- Case: Ii: Lecturer: Mr. Shakeel BaigDocument2 pagesCase: Ii: Lecturer: Mr. Shakeel BaigKathleen De JesusNo ratings yet

- EPLC Annual Operational Analysis ChecklistDocument1 pageEPLC Annual Operational Analysis ChecklistTawfiq4444No ratings yet

- Ralph Lauren Seeks Tax Refund Through LoopholeDocument3 pagesRalph Lauren Seeks Tax Refund Through LoopholeJeff Weiner100% (1)

- AA Commerce BrandsDocument12 pagesAA Commerce BrandsGiang NguyenNo ratings yet

- Master the World of Finance in LondonDocument14 pagesMaster the World of Finance in LondonJM KoffiNo ratings yet

- DSWD-QMS-GF-005 - REV 05 - CSM Questionnaire English VersionDocument1 pageDSWD-QMS-GF-005 - REV 05 - CSM Questionnaire English VersionChrisAlmerRamosNo ratings yet

- Second Activity in Allied - TOEICDocument2 pagesSecond Activity in Allied - TOEICRia Joy SanchezNo ratings yet

- 2000 5000 Imo Company Update 20230215Document145 pages2000 5000 Imo Company Update 20230215Contra Value BetsNo ratings yet

- Successful Career DevelopmentDocument7 pagesSuccessful Career DevelopmentAynurNo ratings yet

- Trading Agreement 2018 - SolidmarkDocument2 pagesTrading Agreement 2018 - SolidmarkPhillip James TabiqueNo ratings yet

- Paradox of The StarDocument8 pagesParadox of The Starapi-355247368No ratings yet

- Rameen Khan 5B.Document18 pagesRameen Khan 5B.Umair FarooquiNo ratings yet

- PROSPECTIVE TENANT QUESTIONNAIRE (Updated 31.05.19 BHJ and MJBS) - 1Document10 pagesPROSPECTIVE TENANT QUESTIONNAIRE (Updated 31.05.19 BHJ and MJBS) - 1Duke Jno100% (1)

- Identity Theft Letter For COVID-19Document2 pagesIdentity Theft Letter For COVID-19Wgme ProducersNo ratings yet

- Lecture 1 - Structured ProductDocument39 pagesLecture 1 - Structured ProductruoyuanquanNo ratings yet

- Annual Compliance Calendar - Companies Act, 2013 LISTED COMPANY - Series 527 PDFDocument13 pagesAnnual Compliance Calendar - Companies Act, 2013 LISTED COMPANY - Series 527 PDFGaurav SharmaNo ratings yet

- Tugas 4 AKM - Kelompok 5 - 142200278Document13 pagesTugas 4 AKM - Kelompok 5 - 142200278muhammad alfariziNo ratings yet

- Gaurav PDFDocument70 pagesGaurav PDFSandesh GajbhiyeNo ratings yet

- Mail Date: Letter ID: July 30, 2020 L0072489609 C8902954-0 Travis S Swanson CLM: NameDocument3 pagesMail Date: Letter ID: July 30, 2020 L0072489609 C8902954-0 Travis S Swanson CLM: NameTravis SwansonNo ratings yet

- Business Strategy: An Introduction To Market Driven StrategyDocument19 pagesBusiness Strategy: An Introduction To Market Driven StrategyAkki vaidNo ratings yet

- Is Globalization OverDocument188 pagesIs Globalization OverDiego A. Odchimar IIINo ratings yet

- Problem 1Document4 pagesProblem 1Live LoveNo ratings yet

- SAP FICO Training Videos - Materials Folder Screenshots PDFDocument8 pagesSAP FICO Training Videos - Materials Folder Screenshots PDFSajanAndyNo ratings yet

- Corporate Governance Theory and Board StructuresDocument2 pagesCorporate Governance Theory and Board StructuresAmber GanNo ratings yet