You might also like

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- 2003 DecemberDocument7 pages2003 DecemberSherif AwadNo ratings yet

- Chapter 2 Revision Exercises + SolutionsDocument12 pagesChapter 2 Revision Exercises + SolutionsSanad RousanNo ratings yet

- Corporate Finance 3rd Edition Graham Solution ManualDocument15 pagesCorporate Finance 3rd Edition Graham Solution ManualMark PanchitoNo ratings yet

- FMIBDocument10 pagesFMIBVu Ngoc QuyNo ratings yet

- Part A: Ratios For Rio Tinto PLC For The Year Ended 31st December 2019Document11 pagesPart A: Ratios For Rio Tinto PLC For The Year Ended 31st December 2019Estela Luna ChivasNo ratings yet

- Theory & Practice of Financial Management Faraz Naseem Sunday, April 19th, 2020Document12 pagesTheory & Practice of Financial Management Faraz Naseem Sunday, April 19th, 2020Hassaan KhalidNo ratings yet

- GAR39 14 11 2022 Performance Update 3Q2022Document5 pagesGAR39 14 11 2022 Performance Update 3Q2022Devina Ratna DewiNo ratings yet

- Excercises of Chapter Two-SolutionDocument7 pagesExcercises of Chapter Two-SolutionMohammad Al AkoumNo ratings yet

- FINC 301 Assignment 2023 1Document8 pagesFINC 301 Assignment 2023 1kd5d26xw5rNo ratings yet

- Assignment FinalDocument10 pagesAssignment FinalJamal AbbasNo ratings yet

- De Torres, Kiarra Nicel R. - FABM2 W4Document4 pagesDe Torres, Kiarra Nicel R. - FABM2 W4Kiarra Nicel De TorresNo ratings yet

- Vishal Dwivedi Analysis of Financial Statement MBADFB 2022Document3 pagesVishal Dwivedi Analysis of Financial Statement MBADFB 2022Vishal DwivediNo ratings yet

- If Nothing Is Mentioned in The Question, Use 365 Days For A YearDocument9 pagesIf Nothing Is Mentioned in The Question, Use 365 Days For A YearSaifur R. SabbirNo ratings yet

- Finman ProblemDocument16 pagesFinman ProblemKatrizia FauniNo ratings yet

- Bodie10ce SM CH19Document12 pagesBodie10ce SM CH19beadand1No ratings yet

- Class Case 3 - There's More To Us Than Meets The EyeDocument11 pagesClass Case 3 - There's More To Us Than Meets The EyeHannahPojaFeria50% (2)

- ACC314 Business Finance Management Resit Answers (SEPT) R 19-20Document8 pagesACC314 Business Finance Management Resit Answers (SEPT) R 19-20Rukshani RefaiNo ratings yet

- FFMA Jan 23 AnsDocument7 pagesFFMA Jan 23 AnsMiftah Nur HudaNo ratings yet

- FIN7101 - FIN. BUSINESS - TEST - 01 (PBS 21101107) AzdzharulnizzamDocument6 pagesFIN7101 - FIN. BUSINESS - TEST - 01 (PBS 21101107) AzdzharulnizzamAzdzharulnizzam AlwiNo ratings yet

- Assignment 01Document18 pagesAssignment 01Md. Real MiahNo ratings yet

- Corporate Finance 22vaCRTlVYrpDocument8 pagesCorporate Finance 22vaCRTlVYrpAdityaSinghNo ratings yet

- Chapter 2 Financial Statement and Cash Flow AnalysisDocument15 pagesChapter 2 Financial Statement and Cash Flow AnalysisKapil Singh RautelaNo ratings yet

- Final Exam FM Summer 2021Document2 pagesFinal Exam FM Summer 2021AAYAN FARAZNo ratings yet

- Untitled DocumentDocument6 pagesUntitled DocumentAman SinghNo ratings yet

- Solution Manual For Analysis For Financial Management 12th EditionDocument21 pagesSolution Manual For Analysis For Financial Management 12th Editionmissitcantaboc6sp100% (43)

- Full Download Solution Manual For Analysis For Financial Management 12th Edition PDF Full ChapterDocument36 pagesFull Download Solution Manual For Analysis For Financial Management 12th Edition PDF Full Chapterbuoyala6sjff100% (16)

- ACCOUNTS March 2020 PaperDocument10 pagesACCOUNTS March 2020 PaperShania AlertNo ratings yet

- IN Financial Management 1: Leyte CollegesDocument20 pagesIN Financial Management 1: Leyte CollegesJeric LepasanaNo ratings yet

- Ratio Analysis: Categories of RatiosDocument7 pagesRatio Analysis: Categories of RatiosAhmad vlogsNo ratings yet

- Arid Agriculture University, Rawalpindi: Pirmehr Ali ShahDocument3 pagesArid Agriculture University, Rawalpindi: Pirmehr Ali ShahSami UllahNo ratings yet

- Case Enager IndustriesDocument4 pagesCase Enager IndustriesTry DharsanaNo ratings yet

- KasusDocument4 pagesKasusTry DharsanaNo ratings yet

- Unit 2 Financial AnalysisDocument12 pagesUnit 2 Financial AnalysisGizaw BelayNo ratings yet

- Finman FinalsDocument4 pagesFinman FinalsJoana Ann ImpelidoNo ratings yet

- Tugas Personal 1 FINC6193Document9 pagesTugas Personal 1 FINC6193alif syahputra11No ratings yet

- Tugas Ii Financial Management - Mery Oktori Uly BinuDocument7 pagesTugas Ii Financial Management - Mery Oktori Uly BinuMerryNo ratings yet

- FS Analysis Horizontal Vertical ExerciseDocument5 pagesFS Analysis Horizontal Vertical ExerciseCarla Noreen CasianoNo ratings yet

- WEEK 4 FINANCIAL STATEMENT ANALYSIS Part 2Document42 pagesWEEK 4 FINANCIAL STATEMENT ANALYSIS Part 2GIRLNo ratings yet

- MCQ On Financial ManagementDocument28 pagesMCQ On Financial ManagementibrahimNo ratings yet

- 17 Financial Statement AnalysisDocument3 pages17 Financial Statement AnalysisRiselle Ann SanchezNo ratings yet

- F 2 Nov 09 Specimen AnswersDocument9 pagesF 2 Nov 09 Specimen AnswersRobert MunyaradziNo ratings yet

- 3 Statement Model - BlankDocument6 pages3 Statement Model - BlankAina MichaelNo ratings yet

- Dell Technologies IncDocument8 pagesDell Technologies IncBrute1989No ratings yet

- MS04Document34 pagesMS04Varun MandalNo ratings yet

- Assignment 2Document1 pageAssignment 2Sumbal JameelNo ratings yet

- Cost of DebtDocument7 pagesCost of DebtrajyalakshmiNo ratings yet

- Financial Statement Analysis Study Guide Solutions Fill-in-the-Blank EquationsDocument26 pagesFinancial Statement Analysis Study Guide Solutions Fill-in-the-Blank EquationsSajawal KhanNo ratings yet

- INSTRUCTION: Make Sure Your Mobile Phone Is in Silent Mode and Place It at The Front Together With Bags & BooksDocument2 pagesINSTRUCTION: Make Sure Your Mobile Phone Is in Silent Mode and Place It at The Front Together With Bags & BooksSUPPLYOFFICE EVSUBCNo ratings yet

- C18Y1101 Sadhurshan Sathyawelu BAIBF10020Document14 pagesC18Y1101 Sadhurshan Sathyawelu BAIBF10020saran.woowNo ratings yet

- AFA Tut11 Anaylsis & Interpretation of FSDocument9 pagesAFA Tut11 Anaylsis & Interpretation of FSJIA HUI LIMNo ratings yet

- Assignment6 HW6Document7 pagesAssignment6 HW6RUPIKA R GNo ratings yet

- Tutorial 3 ADocument7 pagesTutorial 3 ANguyên NguyênNo ratings yet

- FS and Ratios Addtl ExercisesDocument5 pagesFS and Ratios Addtl ExercisesRaniel PamatmatNo ratings yet

- Financial Analysis - FM - Group AssignmentDocument15 pagesFinancial Analysis - FM - Group Assignmenttsegayeayal88No ratings yet

- AFD Practice Questions Mock (3399)Document7 pagesAFD Practice Questions Mock (3399)AbhiNo ratings yet

- Financial Ratio Analyses and Their Implications To ManagementDocument31 pagesFinancial Ratio Analyses and Their Implications To ManagementKeisha Kaye SaleraNo ratings yet

- Case Study 2 (Class)Document6 pagesCase Study 2 (Class)ummieulfahNo ratings yet

- Valle Quiz AbcDocument6 pagesValle Quiz Abclorie anne valle100% (2)

- Blue Ocean Strategy Section 1 Group 10Document5 pagesBlue Ocean Strategy Section 1 Group 10NavinNo ratings yet

- Case 4 Blue Ocean Strategy S2G5Document4 pagesCase 4 Blue Ocean Strategy S2G5NavinNo ratings yet

- Coffee Store - Excel FileDocument168 pagesCoffee Store - Excel FileNavinNo ratings yet

- Statistics Assignment 2-3Document8 pagesStatistics Assignment 2-3NavinNo ratings yet

- Product BacklogDocument4 pagesProduct BacklogNavinNo ratings yet

- Cardio Good FitnessDocument3 pagesCardio Good FitnessNavinNo ratings yet

- Statistics Assignment - 2-3Document7 pagesStatistics Assignment - 2-3NavinNo ratings yet

- AsdDocument4 pagesAsdNavinNo ratings yet

- Sprint Planning and Product BacklogDocument9 pagesSprint Planning and Product BacklogNavinNo ratings yet

- Exercise 9.1 1Document10 pagesExercise 9.1 1NavinNo ratings yet

- Kellogg's 2009 2010 Net Cash (Millions USD) Net Cash (Millions USD) Changes in Net Cash (Millions USD) Changes in Net Cash (Millions USD)Document4 pagesKellogg's 2009 2010 Net Cash (Millions USD) Net Cash (Millions USD) Changes in Net Cash (Millions USD) Changes in Net Cash (Millions USD)NavinNo ratings yet

- Problem 1.5ADocument5 pagesProblem 1.5ANavinNo ratings yet

- Problem 13-4 1Document5 pagesProblem 13-4 1NavinNo ratings yet

- Balance Statement Assets Liabilities and Stockholder's EquityDocument5 pagesBalance Statement Assets Liabilities and Stockholder's EquityNavinNo ratings yet

- Balanced Sheet For Stockholder'S Equity Stockholder'S EquityDocument10 pagesBalanced Sheet For Stockholder'S Equity Stockholder'S EquityNavinNo ratings yet

- Decision Case 1.2Document3 pagesDecision Case 1.2NavinNo ratings yet

- Assets Column1 Column2 Column3 Column4 Column5 Column6 Column7 Accounts Receivable Open Account Concession SuppliesDocument26 pagesAssets Column1 Column2 Column3 Column4 Column5 Column6 Column7 Accounts Receivable Open Account Concession SuppliesNavinNo ratings yet

- DC 7-1 1) Allowance For Doubtful Account (All in Millions)Document7 pagesDC 7-1 1) Allowance For Doubtful Account (All in Millions)NavinNo ratings yet

- 1) Exercise 7-1 Estimated Percent Uncollectable Estimated Amount UncollectableDocument17 pages1) Exercise 7-1 Estimated Percent Uncollectable Estimated Amount UncollectableNavinNo ratings yet

- DC2Document12 pagesDC2NavinNo ratings yet

- Decision Case 3.1Document3 pagesDecision Case 3.1NavinNo ratings yet

- CS Garment Inc. v. CIR, G.R. No. 182399, 2014Document11 pagesCS Garment Inc. v. CIR, G.R. No. 182399, 2014JMae MagatNo ratings yet

- Assn #3 - SKDocument2 pagesAssn #3 - SKRUBY SHARMANo ratings yet

- BA202 6302640922 ExerciseDocument2 pagesBA202 6302640922 ExercisePatinya VnrkNo ratings yet

- D. YFC UPSALE Sample FInancial Statement FormatDocument9 pagesD. YFC UPSALE Sample FInancial Statement FormatEmmanuel Mary Angelo ChuaNo ratings yet

- Health, Income, & PovertyDocument6 pagesHealth, Income, & PovertytoiNo ratings yet

- Financial Analysis of P & GDocument25 pagesFinancial Analysis of P & Ghitesh_mahajan_3No ratings yet

- Electronic Filing Instructions For Your 2020 Federal Tax ReturnDocument38 pagesElectronic Filing Instructions For Your 2020 Federal Tax ReturnPeter LaFontaine100% (3)

- Dokumen - Tips CPK CaseDocument11 pagesDokumen - Tips CPK CaseHarke Revo Leonard PoliiNo ratings yet

- TAX-303 (Input Taxes)Document7 pagesTAX-303 (Input Taxes)Princess ManaloNo ratings yet

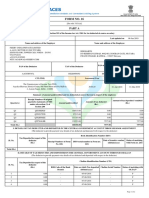

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- AC1025 Commentary 2020Document29 pagesAC1025 Commentary 2020Nghia Tuan NghiaNo ratings yet

- Ding of Accounting Standards 1-15Document25 pagesDing of Accounting Standards 1-15Moeen MakNo ratings yet

- AYB320 - 0122 - Trusts SlidesDocument28 pagesAYB320 - 0122 - Trusts SlidesLinh ĐanNo ratings yet

- Main RatioDocument4 pagesMain RatioJuliette Hamel-GauthierNo ratings yet

- Account TitlesDocument5 pagesAccount TitlesalyNo ratings yet

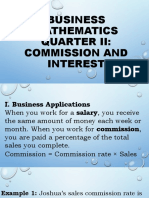

- Business Mathematics Week 2Document37 pagesBusiness Mathematics Week 2Jewel Joy PudaNo ratings yet

- Discussion Questions CVP AnalysisDocument2 pagesDiscussion Questions CVP AnalysisAnnamarisse parungaoNo ratings yet

- Tax-03-01-Basic-Principles of Taxation - EncryptedDocument11 pagesTax-03-01-Basic-Principles of Taxation - Encryptedgean eszekeilNo ratings yet

- Mercury Mining Investment LTD - Audited Reports For 2022Document16 pagesMercury Mining Investment LTD - Audited Reports For 2022tankodanjumacNo ratings yet

- Smart Task 2Document4 pagesSmart Task 2Ruchira ParwandaNo ratings yet

- Orange Modern Business Startup Presentation TemplateDocument23 pagesOrange Modern Business Startup Presentation TemplateAngelica TaniaNo ratings yet

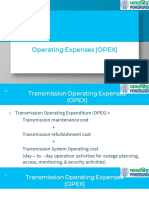

- Operating Expenses (OPEX)Document9 pagesOperating Expenses (OPEX)ASH TVNo ratings yet

- Manacc Assignment 14-3: Make or Buy A ComponentDocument7 pagesManacc Assignment 14-3: Make or Buy A ComponentCuster CoNo ratings yet

- Balance Sheet Ay 2023-24 Mubarak ShaikhDocument5 pagesBalance Sheet Ay 2023-24 Mubarak Shaikhtax advisorNo ratings yet

- Adjusting Review 2Document9 pagesAdjusting Review 2John BushNo ratings yet

- Chapter 4: Accrual Accounting Concepts Case Study: Okendo ConsultingDocument1 pageChapter 4: Accrual Accounting Concepts Case Study: Okendo ConsultingJanNo ratings yet

- Projected Income StatementDocument4 pagesProjected Income StatementRavi DhillonNo ratings yet

- p3b Indonesia - Amerika.Document16 pagesp3b Indonesia - Amerika.Bagus BudionoNo ratings yet

- Phuket Beach HotelDocument3 pagesPhuket Beach HotelKislay KisuNo ratings yet

- Statement of Change in EquityDocument1 pageStatement of Change in EquityYagika JagnaniNo ratings yet