You might also like

- LLQP Exam Prep Study NotesDocument361 pagesLLQP Exam Prep Study NotesMikaila Burnett100% (1)

- Role of Integreted Marketing Communication in Life Insurence New PDFDocument99 pagesRole of Integreted Marketing Communication in Life Insurence New PDFSora Ghosh0% (1)

- Renewal Premium Receipt: Policy Number Date & Time AmountDocument1 pageRenewal Premium Receipt: Policy Number Date & Time AmountGokuNo ratings yet

- NPS Exit Manual User GuideDocument5 pagesNPS Exit Manual User GuideNavendu PandeyNo ratings yet

- FAQs On Final Exit, Annuity and Continuation - Deferment Process For eNPS SubscribersDocument13 pagesFAQs On Final Exit, Annuity and Continuation - Deferment Process For eNPS SubscribersfoxbatneoNo ratings yet

- Gratuity PolicyDocument4 pagesGratuity PolicySiddhraj Singh KushwahaNo ratings yet

- Finance and AccountingDocument12 pagesFinance and AccountingvigneshpandiNo ratings yet

- Sec.80 DDDocument4 pagesSec.80 DDSurbhi PunshiNo ratings yet

- Jeevan - Akshay-Vi Premium VasuDocument24 pagesJeevan - Akshay-Vi Premium VasumbadevilNo ratings yet

- Lifelong BrochureDocument10 pagesLifelong BrochureSambaiahMallelaNo ratings yet

- Exit Amend123Document10 pagesExit Amend123Ketan DiwateNo ratings yet

- LIC Jeevan Azad Brochure EngDocument14 pagesLIC Jeevan Azad Brochure EngPravin PatilNo ratings yet

- Income-Tax-Fy2016-17 Income-Tax Benefits From Life Insurance and Rates For Assessment Year 2017-2018 (Financial Year 2016-2017)Document3 pagesIncome-Tax-Fy2016-17 Income-Tax Benefits From Life Insurance and Rates For Assessment Year 2017-2018 (Financial Year 2016-2017)Puran Singh LabanaNo ratings yet

- 03 Revised FAQs For Central Government Sector CG and Central Autonomous Bodies CABsDocument15 pages03 Revised FAQs For Central Government Sector CG and Central Autonomous Bodies CABsKoushik MannaNo ratings yet

- 2016 SSS Guidebook RetirementDocument16 pages2016 SSS Guidebook RetirementhddhjdjdndndjdjdjNo ratings yet

- DeductionsDocument42 pagesDeductionsNithya RajNo ratings yet

- 2016 SSS Guidebook RetirementDocument16 pages2016 SSS Guidebook RetirementjayinthelongrunNo ratings yet

- Dhan Vriddhi English Sales BrochureDocument16 pagesDhan Vriddhi English Sales BrochureNimesh PrakashNo ratings yet

- Now I Can Secure My Family's Future With Just A Click.: Bharti AXA Life ProtectDocument12 pagesNow I Can Secure My Family's Future With Just A Click.: Bharti AXA Life ProtectVenkatram Reddy KamasaniNo ratings yet

- Extend Your Lifeline by 15 Years.: SecureDocument1 pageExtend Your Lifeline by 15 Years.: SecurePinal JEngineerNo ratings yet

- Salient Features:: LIC Introduces New Jeevan Nidhi' - Deferred Pension PlanDocument5 pagesSalient Features:: LIC Introduces New Jeevan Nidhi' - Deferred Pension PlanPramod Kumar SaxenaNo ratings yet

- Akansha Investment Services: Home Products Services SMS Service FAQ Contact DetailsDocument6 pagesAkansha Investment Services: Home Products Services SMS Service FAQ Contact Detailssarup007No ratings yet

- Dhan Varsha Sales BrochureDocument12 pagesDhan Varsha Sales BrochureCyril PilligrinNo ratings yet

- Bajaj Alliance Lifelong-Brochure PDFDocument9 pagesBajaj Alliance Lifelong-Brochure PDFSriram SundararamanNo ratings yet

- EPF Claim-Withdrawal ProvisionsDocument5 pagesEPF Claim-Withdrawal ProvisionsImran MohammadNo ratings yet

- Lic Leaflet Endoment Plan4 5x8 Inches WXH NewDocument16 pagesLic Leaflet Endoment Plan4 5x8 Inches WXH NewVishal 777No ratings yet

- LIC Jeevan Umang Brochure 9-Inch-X-8-Inch Eng PDFDocument21 pagesLIC Jeevan Umang Brochure 9-Inch-X-8-Inch Eng PDFManish MauryaNo ratings yet

- Sales Brochure LIC Bima Jyoti NEW WEBDocument20 pagesSales Brochure LIC Bima Jyoti NEW WEBSamNo ratings yet

- Nps One PagerDocument2 pagesNps One PagerldorayaNo ratings yet

- Lic Pension PlansDocument5 pagesLic Pension PlansMarsh JainNo ratings yet

- LIC Jeevan Umang Brochure 9-Inch-X-8-Inch Eng (2021)Document21 pagesLIC Jeevan Umang Brochure 9-Inch-X-8-Inch Eng (2021)sri_plnsNo ratings yet

- Welcome Letter - N-EAP0008408146 - 05022023Document3 pagesWelcome Letter - N-EAP0008408146 - 05022023Aniket GavhankarNo ratings yet

- Mediclaim 80dDocument5 pagesMediclaim 80dPaymaster ServicesNo ratings yet

- Section 80D Deduction For Mediclaim Insurance PremiumDocument46 pagesSection 80D Deduction For Mediclaim Insurance PremiumsameerNo ratings yet

- Part 2Document2 pagesPart 2blimjucoNo ratings yet

- Question:-Q Write Note On Deduction U/s 80 C To 80 UDocument15 pagesQuestion:-Q Write Note On Deduction U/s 80 C To 80 UnikhilNo ratings yet

- Icare Brochure PDFDocument6 pagesIcare Brochure PDFyatinthoratscrbNo ratings yet

- Chpater 8 Pension & WelfareDocument54 pagesChpater 8 Pension & WelfareSami Ur RehmanNo ratings yet

- PMJBY Application Form in EnglishDocument3 pagesPMJBY Application Form in EnglishAnonymous PHCzwD8eAONo ratings yet

- APY FAQs PDFDocument8 pagesAPY FAQs PDFKishan VarshneyNo ratings yet

- Acts and RulesDocument6 pagesActs and Rulesjaykishan prasadNo ratings yet

- Chapter-7 DeductionDocument7 pagesChapter-7 DeductionBrinda RNo ratings yet

- Sales - Brochure - LIC S New Money Back 25 Yrs PlanDocument11 pagesSales - Brochure - LIC S New Money Back 25 Yrs PlanShubham PandeyNo ratings yet

- Benefits:: Participation in ProfitsDocument10 pagesBenefits:: Participation in Profitslakshman777No ratings yet

- Lic PPTDocument21 pagesLic PPTvsharma0091No ratings yet

- Kasih FamiliDocument26 pagesKasih FamiliBig DaddyCoolNo ratings yet

- Sales Brochure LIC S Navjeevan To CC DeptDocument14 pagesSales Brochure LIC S Navjeevan To CC DeptRajasekar KaruppusamyNo ratings yet

- Ko Tak Capital Multiplier PlanDocument2 pagesKo Tak Capital Multiplier PlanemailtotesttestNo ratings yet

- Great Critical Care Relief GCCRDocument7 pagesGreat Critical Care Relief GCCRraathi_cdiNo ratings yet

- Nirvana Pension Policy - Tata-AIG: SuitabilityDocument4 pagesNirvana Pension Policy - Tata-AIG: Suitabilityprabs9869No ratings yet

- LIC's Jeevan Umang (UIN: 512N312V02) (A Non-Linked, Participating, Individual, Life Assurance Savings (Whole Life) Plan)Document14 pagesLIC's Jeevan Umang (UIN: 512N312V02) (A Non-Linked, Participating, Individual, Life Assurance Savings (Whole Life) Plan)manoj gokikarNo ratings yet

- Life Secure Brochure - 1Document13 pagesLife Secure Brochure - 1spikysanchitNo ratings yet

- Lic Leaflet Jeevan Anand 4 5x8 Inches WXH DEC 2020Document16 pagesLic Leaflet Jeevan Anand 4 5x8 Inches WXH DEC 2020bantwal_venkateshNo ratings yet

- Sbi Life EshieldDocument6 pagesSbi Life EshieldAnkit VyasNo ratings yet

- GsisDocument28 pagesGsisKristiana Montenegro GelingNo ratings yet

- Insurance Pension PlansDocument35 pagesInsurance Pension Plansedrich1932No ratings yet

- Lic Market Plus IDocument8 pagesLic Market Plus Ianpuselvi125No ratings yet

- Income Tax Rates (For Individuals, Hufs, Association of Persons, Body of Individuals) Assessment Year 2011-2012 Relevant To Financial Year 2010-2011Document6 pagesIncome Tax Rates (For Individuals, Hufs, Association of Persons, Body of Individuals) Assessment Year 2011-2012 Relevant To Financial Year 2010-2011jhancyNo ratings yet

- TM Module IV NotesDocument16 pagesTM Module IV NotesAnkur DubeyNo ratings yet

- Deductions 2021 22Document5 pagesDeductions 2021 22Karan RajakNo ratings yet

- Benefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)Document11 pagesBenefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)coolestkasinovaNo ratings yet

- Sales Brochure LIC S Saral PensionDocument10 pagesSales Brochure LIC S Saral PensionKshitij KumarNo ratings yet

- Attendance by PhotographyDocument1 pageAttendance by PhotographySrihariteja Achanta PNo ratings yet

- 28.12.2022 Hon'Ble CM's Anakapalli District ScheduleDocument2 pages28.12.2022 Hon'Ble CM's Anakapalli District ScheduleSrihariteja Achanta PNo ratings yet

- Mock Drill For Covid19 ManualDocument5 pagesMock Drill For Covid19 ManualSrihariteja Achanta PNo ratings yet

- CalendarDocument1 pageCalendarSrihariteja Achanta PNo ratings yet

- CFMS DecentralizedActvitiesDocument3 pagesCFMS DecentralizedActvitiesSrihariteja Achanta PNo ratings yet

- TELANGANA SSS Rules, SriPathanjaliDocument91 pagesTELANGANA SSS Rules, SriPathanjaliSrihariteja Achanta PNo ratings yet

- Why Conserve Forests SriPKSharmaIFS (Retd)Document19 pagesWhy Conserve Forests SriPKSharmaIFS (Retd)Srihariteja Achanta PNo ratings yet

- Ap State PoliceDocument12 pagesAp State PoliceSrihariteja Achanta PNo ratings yet

- JudgementOrder WritingDocument26 pagesJudgementOrder WritingSrihariteja Achanta PNo ratings yet

- Check List For Offfice Inspctions - Collectorates1Document57 pagesCheck List For Offfice Inspctions - Collectorates1Srihariteja Achanta PNo ratings yet

- NPS Views - (Subscriber & DDO)Document16 pagesNPS Views - (Subscriber & DDO)Srihariteja Achanta PNo ratings yet

- 684 - TGDocument6 pages684 - TGSrihariteja Achanta PNo ratings yet

- This Form Is To Be Used by The Nodal Office (Prao/Dta/Pao/Dto/Pop/Cho) Registered Under Nps To Update/Modify Bank Account Details in The Cra SystemDocument1 pageThis Form Is To Be Used by The Nodal Office (Prao/Dta/Pao/Dto/Pop/Cho) Registered Under Nps To Update/Modify Bank Account Details in The Cra SystemSrihariteja Achanta PNo ratings yet

- Job ProfileDocument24 pagesJob ProfileSrihariteja Achanta PNo ratings yet

- Protocol PDFDocument28 pagesProtocol PDFSrihariteja Achanta PNo ratings yet

- Modalities For Leave ApplicationDocument4 pagesModalities For Leave ApplicationSrihariteja Achanta PNo ratings yet

- P. Subashchandra Bose,: Accounts Officer-NHM, O/o. The DM&HO, ChittoorDocument3 pagesP. Subashchandra Bose,: Accounts Officer-NHM, O/o. The DM&HO, ChittoorSrihariteja Achanta PNo ratings yet

- Insurance Awareness Video 6 To 8 PDFDocument23 pagesInsurance Awareness Video 6 To 8 PDFrr04121999No ratings yet

- Exit From National Pension System Due To Superannuation and Incapacitation...Document6 pagesExit From National Pension System Due To Superannuation and Incapacitation...Kiran AlluriNo ratings yet

- Tree of WealthDocument121 pagesTree of WealthJoseAliceaNo ratings yet

- Chat GPT Banking SystemDocument7 pagesChat GPT Banking SystemSebas GarciaNo ratings yet

- Chapter - Five: Major Classification of InsuranceDocument61 pagesChapter - Five: Major Classification of InsuranceberNo ratings yet

- Invoice 8763639678Document1 pageInvoice 8763639678Arjun VyasNo ratings yet

- Full Download Ebook PDF Personal Financial Planning 14th Edition PDFDocument27 pagesFull Download Ebook PDF Personal Financial Planning 14th Edition PDFjames.sepulveda805100% (29)

- Cmfas M 9: OduleDocument23 pagesCmfas M 9: Odulezihan.pohNo ratings yet

- Examination: Subject CT5 - Contingencies Core TechnicalDocument7 pagesExamination: Subject CT5 - Contingencies Core TechnicalMadonnaNo ratings yet

- Bain Morgan REPORT Part 1Document4 pagesBain Morgan REPORT Part 1Romrick TorregosaNo ratings yet

- Tata PlanDocument8 pagesTata PlanLIFE HACKNo ratings yet

- Fundamental Analysis On Max Life InsuranceDocument16 pagesFundamental Analysis On Max Life InsuranceSimon StilerNo ratings yet

- R.U DarbyDocument2 pagesR.U DarbyMm ZNo ratings yet

- Sbaa 1401Document126 pagesSbaa 1401gayuammu1135No ratings yet

- Project Report: Life Insurance Corporation of IndiaDocument60 pagesProject Report: Life Insurance Corporation of IndiaSammy Zala100% (1)

- Assignment in Insurance Policy - Meaning - Explanation - TypesDocument4 pagesAssignment in Insurance Policy - Meaning - Explanation - TypesManish Kr. Singh (B.A. LLB 16)No ratings yet

- VL Mock Exam Set 1Document12 pagesVL Mock Exam Set 1Arvin AltamiaNo ratings yet

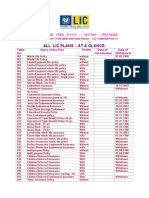

- All LIC PlansDocument4 pagesAll LIC Planslicvivek100% (1)

- Job Shadowing JournalDocument4 pagesJob Shadowing Journalapi-568505765No ratings yet

- Internship REPORT HumotyDocument28 pagesInternship REPORT HumotyDeepak BardejaNo ratings yet

- PAA 2M SA TPD 1M ADD LCB 36k ApeDocument10 pagesPAA 2M SA TPD 1M ADD LCB 36k ApeRey Christopher CastilloNo ratings yet

- Hon'Ble Mr. Justice Shantanu S. Kemkar, President Hon'Ble Mr. Shyam Sunder Bansal, Member Hon'Ble Mr. Prabhat Parashar, MemberDocument9 pagesHon'Ble Mr. Justice Shantanu S. Kemkar, President Hon'Ble Mr. Shyam Sunder Bansal, Member Hon'Ble Mr. Prabhat Parashar, MemberAnand ShahaniNo ratings yet

- ViewReport-icici Prem ReceiptDocument1 pageViewReport-icici Prem ReceiptPramod Shanker MathurNo ratings yet

- Indian Insurance Industry AnalysisDocument90 pagesIndian Insurance Industry Analysismansidube138680% (10)

- Endowment PolicyDocument38 pagesEndowment PolicyGourav DeNo ratings yet

- Bagrao Raviraj Kashinath: A Project Synopsis FOR Life Insurance Submitted byDocument26 pagesBagrao Raviraj Kashinath: A Project Synopsis FOR Life Insurance Submitted byJai GaneshNo ratings yet

- BBAE 0401 Principles & Practices of Life Insurance SyllabusDocument82 pagesBBAE 0401 Principles & Practices of Life Insurance SyllabusEkansh MaheshwariNo ratings yet