You might also like

- Internal Test 4 - CaseDocument6 pagesInternal Test 4 - CaseShivani Jadhav25% (8)

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- 21st Century Fox 5YR DCFDocument10 pages21st Century Fox 5YR DCFsoham sahaNo ratings yet

- 2budget at A Glance 2023-24 (English)Document31 pages2budget at A Glance 2023-24 (English)Chandrima MannaNo ratings yet

- Budget 2022-23 (English) - 0Document31 pagesBudget 2022-23 (English) - 0niks dNo ratings yet

- AFF's Tax Memorandum On Finance Bill, 2021Document47 pagesAFF's Tax Memorandum On Finance Bill, 2021ahmad muzaffarNo ratings yet

- PrepzFy - LBO - VemptyDocument3 pagesPrepzFy - LBO - VemptykouakouNo ratings yet

- 1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationDocument8 pages1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationJajahinaNo ratings yet

- Dipawali ReportDocument16 pagesDipawali ReportKeval ShahNo ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- Apollo Hospitals Enterprise Limited NSEI APOLLOHOSP FinancialsDocument40 pagesApollo Hospitals Enterprise Limited NSEI APOLLOHOSP Financialsakumar4uNo ratings yet

- Jollibee Foods Corporation PSE JFC FinancialsDocument38 pagesJollibee Foods Corporation PSE JFC FinancialsJasper Andrew AdjaraniNo ratings yet

- EconomyDocument2 pagesEconomyAnand DhakadNo ratings yet

- Chapter - 1Document24 pagesChapter - 1mrinal halderNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- The Presentation MaterialsDocument35 pagesThe Presentation MaterialsZerohedgeNo ratings yet

- Canada OECD Economic Outlook May 2021Document4 pagesCanada OECD Economic Outlook May 2021Qian XinzhouNo ratings yet

- 2012-13 Preliminary Budget Presentation Nov 2011Document32 pages2012-13 Preliminary Budget Presentation Nov 2011weikertdNo ratings yet

- 2019 11 14 PH e DMCDocument7 pages2019 11 14 PH e DMC124th EAGLECOM KimJaveroNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Document5 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Namrata ShahNo ratings yet

- ABB Q3 2022 Financial InformationDocument48 pagesABB Q3 2022 Financial InformationMATHU MOHANNo ratings yet

- Financial Modelling Complete Internal Test 4Document6 pagesFinancial Modelling Complete Internal Test 4vaibhav100% (1)

- STRABAG - SE - Geschäftsbericht 2020 - E - ADocument264 pagesSTRABAG - SE - Geschäftsbericht 2020 - E - ASiddhartha ShekharNo ratings yet

- Microsoft Corporation NasdaqGS MSFT FinancialsDocument35 pagesMicrosoft Corporation NasdaqGS MSFT FinancialssimplyashuNo ratings yet

- FCW - Human Security 22-30Document30 pagesFCW - Human Security 22-30rodolfo opidoNo ratings yet

- Table 1. Macroeconomic Indicators: MoroccoDocument5 pagesTable 1. Macroeconomic Indicators: MoroccoazfatrafNo ratings yet

- Analysts Meeting BM Q2-2019 (LONG FORM)Document104 pagesAnalysts Meeting BM Q2-2019 (LONG FORM)RadiSujadi24041977No ratings yet

- Backus Valuation ExcelDocument28 pagesBackus Valuation ExcelAdrian MontoyaNo ratings yet

- RD Release 2Q21 20210810 ENDocument19 pagesRD Release 2Q21 20210810 ENRodrigo FerreiraNo ratings yet

- Analyst Presentation (Mar 10)Document32 pagesAnalyst Presentation (Mar 10)agarwalomNo ratings yet

- H1 2022 Results PresentationDocument28 pagesH1 2022 Results PresentationUday KiranNo ratings yet

- Branch FormatDocument1 pageBranch FormatShweta YaragattiNo ratings yet

- Britannia 1Document40 pagesBritannia 1Dipesh GuptaNo ratings yet

- Informe Del Institute of International FinanceDocument1 pageInforme Del Institute of International FinanceDiario PulseNo ratings yet

- Topics Impact of Payra Deep Sea Port On Bangladesh Economy: ID BatchDocument9 pagesTopics Impact of Payra Deep Sea Port On Bangladesh Economy: ID BatchRaju RiadNo ratings yet

- Upgrade To Buy VNM Trades at A Seven-Year Low: Company UpdateDocument11 pagesUpgrade To Buy VNM Trades at A Seven-Year Low: Company Updatetài chính Kinh tế lượngNo ratings yet

- Fortis Healthcare Limited BSE 532843 FinancialsDocument44 pagesFortis Healthcare Limited BSE 532843 Financialsakumar4uNo ratings yet

- The Graph Showing Net Working CapitalDocument31 pagesThe Graph Showing Net Working CapitalPRATIK PALKHENo ratings yet

- Nestle India Dupont AnalysisDocument2 pagesNestle India Dupont AnalysisINDIAN REALITY SHOWSNo ratings yet

- Resumer Du MemoireDocument10 pagesResumer Du Memoirerita tamohNo ratings yet

- Budget Indicators: Sergio M. MarxuachDocument19 pagesBudget Indicators: Sergio M. MarxuachOscar J. SerranoNo ratings yet

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDocument14 pagesWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNo ratings yet

- HCL Tech q1 Fy22 Investor ReleaseDocument29 pagesHCL Tech q1 Fy22 Investor ReleasemsanrxlNo ratings yet

- LaosDocument1 pageLaosGuan ChyeNo ratings yet

- UNIONBANK - Investor Presentation - 13-May-22 - TickertapeDocument69 pagesUNIONBANK - Investor Presentation - 13-May-22 - Tickertapesukash sNo ratings yet

- Value Investing FundamentalDocument7 pagesValue Investing FundamentalAdam PermanaNo ratings yet

- Constellation Software Inc.: A. Historical Figures Restated To Comply With Revised DefinitionDocument8 pagesConstellation Software Inc.: A. Historical Figures Restated To Comply With Revised DefinitionSugar RayNo ratings yet

- FCF bảng CDocument3 pagesFCF bảng CĐình Thịnh LêNo ratings yet

- Karnataka Bank 2022 PerfomaceDocument59 pagesKarnataka Bank 2022 Perfomacesahal95264No ratings yet

- Constellation Software IncDocument6 pagesConstellation Software IncSugar RayNo ratings yet

- Exide IndustriesDocument55 pagesExide IndustriesSALONI JaiswalNo ratings yet

- Total Income - Annual: Sales Sales YoyDocument16 pagesTotal Income - Annual: Sales Sales YoyKshatrapati SinghNo ratings yet

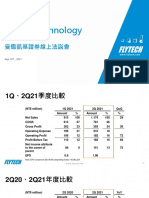

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Suumary of Key Drivers 1.0Document6 pagesSuumary of Key Drivers 1.0Matthew SiagianNo ratings yet

- Kahoot! (Buy TP NOK150) : The Compound Interest Effect With Triple Digit Revenue Growth and +40% FCF Margin Is Massive!Document24 pagesKahoot! (Buy TP NOK150) : The Compound Interest Effect With Triple Digit Revenue Growth and +40% FCF Margin Is Massive!jainantoNo ratings yet

- SiemensDocument9 pagesSiemensCam SNo ratings yet

- Accounting For Managers: Report Over The Financial Performance of JB HifiDocument8 pagesAccounting For Managers: Report Over The Financial Performance of JB HifiMah Noor FastNUNo ratings yet

- IDirect BudgetReview 2022-23Document13 pagesIDirect BudgetReview 2022-23Nagesha pa nagaNo ratings yet

- 18 Statistics Key Economic IndicatorsDocument17 pages18 Statistics Key Economic Indicatorsjohnmarch146No ratings yet

- Bwcu Htsqwn00sorvupdk.3Document22 pagesBwcu Htsqwn00sorvupdk.3JoshKernNo ratings yet

- Mncs From LDCS: The Case of Indian Joint Ventures Abroad : K. BalakrishnanDocument16 pagesMncs From LDCS: The Case of Indian Joint Ventures Abroad : K. BalakrishnanSmriti SaxenaNo ratings yet

- PHP 1 SFZ Z1Document19 pagesPHP 1 SFZ Z1Smriti SaxenaNo ratings yet

- E Prospectus UG COP 2022 23Document58 pagesE Prospectus UG COP 2022 23Smriti SaxenaNo ratings yet

- Block 1Document96 pagesBlock 1Smriti SaxenaNo ratings yet

- Minimum Wages For Ronald Mcdonald Monopsonies A Theory of Monopsonistic CompetitionDocument18 pagesMinimum Wages For Ronald Mcdonald Monopsonies A Theory of Monopsonistic CompetitionSmriti SaxenaNo ratings yet

- CBSE Expression Series 2021Document2 pagesCBSE Expression Series 2021Smriti SaxenaNo ratings yet

- 2 RDBMS ConceptsDocument20 pages2 RDBMS ConceptsSmriti SaxenaNo ratings yet

- DBMS Assignment 2022Document2 pagesDBMS Assignment 2022Smriti SaxenaNo ratings yet

- WSS Table No. 05 Ratios and RatesDocument90 pagesWSS Table No. 05 Ratios and RatesSmriti SaxenaNo ratings yet

- The Ocean of Churn PDFDocument26 pagesThe Ocean of Churn PDFSmriti SaxenaNo ratings yet

- Class XII Applied Math Mock TestDocument4 pagesClass XII Applied Math Mock TestSmriti SaxenaNo ratings yet

- Prachi CUET-UG AccountancyDocument22 pagesPrachi CUET-UG AccountancySmriti Saxena100% (1)

- Using Boss Tone Studio For Me-25Document4 pagesUsing Boss Tone Studio For Me-25Oskar WojciechowskiNo ratings yet

- LMU-2100™ Gprs/Cdmahspa Series: Insurance Tracking Unit With Leading TechnologiesDocument2 pagesLMU-2100™ Gprs/Cdmahspa Series: Insurance Tracking Unit With Leading TechnologiesRobert MateoNo ratings yet

- Dialog Suntel MergerDocument8 pagesDialog Suntel MergerPrasad DilrukshanaNo ratings yet

- 30 Creative Activities For KidsDocument4 pages30 Creative Activities For KidsLaloGomezNo ratings yet

- Role of The Government in HealthDocument6 pagesRole of The Government in Healthptv7105No ratings yet

- 4th Sem Electrical AliiedDocument1 page4th Sem Electrical AliiedSam ChavanNo ratings yet

- Fedex Service Guide: Everything You Need To Know Is OnlineDocument152 pagesFedex Service Guide: Everything You Need To Know Is OnlineAlex RuizNo ratings yet

- Weekly Learning PlanDocument2 pagesWeekly Learning PlanJunrick DalaguitNo ratings yet

- Lab 6 PicoblazeDocument6 pagesLab 6 PicoblazeMadalin NeaguNo ratings yet

- Epidemiologi DialipidemiaDocument5 pagesEpidemiologi DialipidemianurfitrizuhurhurNo ratings yet

- Interruptions - 02.03.2023Document2 pagesInterruptions - 02.03.2023Jeff JeffNo ratings yet

- Avalon LF GB CTP MachineDocument2 pagesAvalon LF GB CTP Machinekojo0% (1)

- PLT Lecture NotesDocument5 pagesPLT Lecture NotesRamzi AbdochNo ratings yet

- Proceedings of SpieDocument7 pagesProceedings of SpieNintoku82No ratings yet

- Reverse Engineering in Rapid PrototypeDocument15 pagesReverse Engineering in Rapid PrototypeChaubey Ajay67% (3)

- Difference Between Mountain Bike and BMXDocument3 pagesDifference Between Mountain Bike and BMXShakirNo ratings yet

- XgxyDocument22 pagesXgxyLïkïth RäjNo ratings yet

- TAS5431-Q1EVM User's GuideDocument23 pagesTAS5431-Q1EVM User's GuideAlissonNo ratings yet

- A320 TakeoffDocument17 pagesA320 Takeoffpp100% (1)

- Expense Tracking - How Do I Spend My MoneyDocument2 pagesExpense Tracking - How Do I Spend My MoneyRenata SánchezNo ratings yet

- COOKERY10 Q2W4 10p LATOJA SPTVEDocument10 pagesCOOKERY10 Q2W4 10p LATOJA SPTVECritt GogolinNo ratings yet

- Heavy LiftDocument4 pagesHeavy Liftmaersk01No ratings yet

- Hexoskin - Information For Researchers - 01 February 2023Document48 pagesHexoskin - Information For Researchers - 01 February 2023emrecan cincanNo ratings yet

- Powerpoint Presentation: Calcium Sulphate in Cement ManufactureDocument7 pagesPowerpoint Presentation: Calcium Sulphate in Cement ManufactureDhruv PrajapatiNo ratings yet

- MOTOR INSURANCE - Two Wheeler Liability Only SCHEDULEDocument1 pageMOTOR INSURANCE - Two Wheeler Liability Only SCHEDULESuhail V VNo ratings yet

- Privacy: Based On Slides Prepared by Cyndi Chie, Sarah Frye and Sharon Gray. Fifth Edition Updated by Timothy HenryDocument50 pagesPrivacy: Based On Slides Prepared by Cyndi Chie, Sarah Frye and Sharon Gray. Fifth Edition Updated by Timothy HenryAbid KhanNo ratings yet

- Arduino Based Voice Controlled Robot: Aditya Chaudhry, Manas Batra, Prakhar Gupta, Sahil Lamba, Suyash GuptaDocument3 pagesArduino Based Voice Controlled Robot: Aditya Chaudhry, Manas Batra, Prakhar Gupta, Sahil Lamba, Suyash Guptaabhishek kumarNo ratings yet

- Microwave Drying of Gelatin Membranes and Dried Product Properties CharacterizationDocument28 pagesMicrowave Drying of Gelatin Membranes and Dried Product Properties CharacterizationDominico Delven YapinskiNo ratings yet

- Manual 40ku6092Document228 pagesManual 40ku6092Marius Stefan BerindeNo ratings yet

- Polytropic Process1Document4 pagesPolytropic Process1Manash SinghaNo ratings yet