You might also like

- PAS 1 Presentation of Financial Statements: Quiz 1: Multiple ChoiceDocument3 pagesPAS 1 Presentation of Financial Statements: Quiz 1: Multiple Choicetrixie mae88% (8)

- Retirement Planning Calculator - MR Money TVDocument6 pagesRetirement Planning Calculator - MR Money TVCath CNo ratings yet

- Arsenal FC Financial AnalysisDocument14 pagesArsenal FC Financial AnalysisDidiDieva0% (1)

- Finacle Friendly A Handbook On CbsDocument289 pagesFinacle Friendly A Handbook On CbsS. Allen78% (23)

- Beechy 7e Tif Ch09Document20 pagesBeechy 7e Tif Ch09mashta04No ratings yet

- Trading Course SyllabusDocument13 pagesTrading Course SyllabusCrypto CosmonautNo ratings yet

- Financial AnalysisDocument20 pagesFinancial AnalysisJosNo ratings yet

- Fabm2 Pre-AssessmentDocument6 pagesFabm2 Pre-AssessmentGleire Anne CatambacanNo ratings yet

- Quiz 1. Conceptual Framework and Accounting Standards: PointsDocument21 pagesQuiz 1. Conceptual Framework and Accounting Standards: PointsMarcus MonocayNo ratings yet

- ACC109 Exam Review: Key Financial Reporting ConceptsDocument12 pagesACC109 Exam Review: Key Financial Reporting ConceptsRosemarie VillanuevaNo ratings yet

- 304 - Fin - Advance Financial Management MCQ Test - 1Document8 pages304 - Fin - Advance Financial Management MCQ Test - 1Shubham ArgadeNo ratings yet

- w4 w6 c4 Concept Fsa ProblemDocument15 pagesw4 w6 c4 Concept Fsa Problemjustine cabanaNo ratings yet

- Completed ProjectDocument64 pagesCompleted ProjectPuneeth ArNo ratings yet

- Description: Tags: 0601chapter5Document51 pagesDescription: Tags: 0601chapter5anon-7700No ratings yet

- Student InformationDocument19 pagesStudent InformationJohnrick VallenteNo ratings yet

- Lesson 1. Financial Statements (Cabrera & Cabrera, 2017)Document10 pagesLesson 1. Financial Statements (Cabrera & Cabrera, 2017)Axel MendozaNo ratings yet

- Final Exam Simulation 1Document17 pagesFinal Exam Simulation 1Carmel Rae TalimioNo ratings yet

- Statements.: Online Activities (Synchronous/ Asynchronous)Document5 pagesStatements.: Online Activities (Synchronous/ Asynchronous)Rosejane EMNo ratings yet

- A Study On Financial Forecasting and Performance of ZOHO CORPORATION PRIVATE LIMITEDDocument22 pagesA Study On Financial Forecasting and Performance of ZOHO CORPORATION PRIVATE LIMITEDmanoj saravanan0% (1)

- Description: Tags: 0601chapter5Document61 pagesDescription: Tags: 0601chapter5anon-973077No ratings yet

- Cases in Finance Assignment FinalDocument22 pagesCases in Finance Assignment FinalIbrahimNo ratings yet

- B215 AC01 - Numbers and Words - 6th Presentation - 17apr2009Document23 pagesB215 AC01 - Numbers and Words - 6th Presentation - 17apr2009tohqinzhiNo ratings yet

- GL and COA GuideDocument3 pagesGL and COA GuideWahyu JanokoNo ratings yet

- Cfa3 3Document2 pagesCfa3 3Trinh NguyễnNo ratings yet

- FINA2004 Unit 5Document11 pagesFINA2004 Unit 5Taedia HibbertNo ratings yet

- Financial AnalysisDocument69 pagesFinancial AnalysisOlawale Oluwatoyin Bolaji100% (2)

- Financial Statement Analysis ToolsDocument5 pagesFinancial Statement Analysis ToolsBommana SanjanaNo ratings yet

- Acct 4102Document40 pagesAcct 4102Shimul HossainNo ratings yet

- Financial ManagementDocument55 pagesFinancial ManagementayhenferellNo ratings yet

- 489 - Assignment 01 Front Sheet - Fall2020Document11 pages489 - Assignment 01 Front Sheet - Fall2020Bảo NhưNo ratings yet

- CH 06Document60 pagesCH 06Aisha PatelNo ratings yet

- Financial Statement Analysis With MCQ and QuestionsDocument55 pagesFinancial Statement Analysis With MCQ and QuestionsAyush BholeNo ratings yet

- (Scan QR Code To Answer Pre-Assessment) : 1 of 22 (For Dfcamclp Used Only)Document22 pages(Scan QR Code To Answer Pre-Assessment) : 1 of 22 (For Dfcamclp Used Only)maelyn calindong100% (1)

- Pre Test: Biliran Province State UniversityDocument6 pagesPre Test: Biliran Province State Universitymichi100% (1)

- Orca Share Media1668925931673 6999982710921667804Document26 pagesOrca Share Media1668925931673 6999982710921667804Chekani Kristine MamhotNo ratings yet

- Financial Performance 1Document54 pagesFinancial Performance 1bagyaNo ratings yet

- Business Finance: FinalDocument8 pagesBusiness Finance: FinalBryanNo ratings yet

- 1A An Overview of Financial StatementsDocument6 pages1A An Overview of Financial StatementsKevin ChengNo ratings yet

- Accounting Ratios Information: An Instrument For Business Performance AnalysisDocument6 pagesAccounting Ratios Information: An Instrument For Business Performance AnalysisEditor IJTSRDNo ratings yet

- Presentation of Financial StatementsDocument5 pagesPresentation of Financial StatementsVergel MartinezNo ratings yet

- BA5103 Accounting For Management 2marks Unit 3Document19 pagesBA5103 Accounting For Management 2marks Unit 3Shanthi PriyaNo ratings yet

- C39e54c7 1617599931071Document13 pagesC39e54c7 1617599931071Abby NavarroNo ratings yet

- Lec 3 Introduction To FSA 2023Document3 pagesLec 3 Introduction To FSA 2023Khadeeza ShammeeNo ratings yet

- K04046 Building A Best-in-Class Finance Function (Best Practices Report) 20121112 PDFDocument106 pagesK04046 Building A Best-in-Class Finance Function (Best Practices Report) 20121112 PDFinfosahay100% (1)

- PPTDocument60 pagesPPTSonia ChristabellaNo ratings yet

- Jawaban Assigment CH 1Document5 pagesJawaban Assigment CH 1AjiwNo ratings yet

- Audit Quiz Chapter 8,9,10 Review and ResultsDocument7 pagesAudit Quiz Chapter 8,9,10 Review and ResultsMatus HanunNo ratings yet

- Description: Tags: Blue5Document53 pagesDescription: Tags: Blue5anon-394938No ratings yet

- Module 001 Week001-Finacct3 Financial Statements and Conceptual Framework For Financial ReportingDocument10 pagesModule 001 Week001-Finacct3 Financial Statements and Conceptual Framework For Financial Reportingman ibeNo ratings yet

- Financial StatementsDocument3 pagesFinancial StatementsNana LeeNo ratings yet

- Solutions - Chapter 5Document21 pagesSolutions - Chapter 5Dre ThathipNo ratings yet

- acoount projectDocument54 pagesacoount projectvikassharma7068No ratings yet

- Intermediate Accounting 3 (Reviewer)Document6 pagesIntermediate Accounting 3 (Reviewer)Eury Zin GalvezNo ratings yet

- Lesson Plan in Business FinanceDocument9 pagesLesson Plan in Business FinanceEmelen VeranoNo ratings yet

- Selection of Location For A ProjectDocument35 pagesSelection of Location For A ProjectTushar PatilNo ratings yet

- Working Capital & Methods Used For Financial Planning, Needs & Limitations, Types of Financial Statement AnalysisDocument5 pagesWorking Capital & Methods Used For Financial Planning, Needs & Limitations, Types of Financial Statement AnalysisBoobalan RNo ratings yet

- ACC704 - Tutorial 1 QuestionsDocument4 pagesACC704 - Tutorial 1 QuestionsJake LukmistNo ratings yet

- Financial Decision MakingDocument7 pagesFinancial Decision MakingDalreen GamageNo ratings yet

- Financial Performance of AurabindoDocument105 pagesFinancial Performance of AurabindoBalaji AdhikesavanNo ratings yet

- Financial Intelligence: Mastering the Numbers for Business SuccessFrom EverandFinancial Intelligence: Mastering the Numbers for Business SuccessNo ratings yet

- Partnership Revised Corporation Domingo p1 CompressDocument465 pagesPartnership Revised Corporation Domingo p1 CompressanonymousNo ratings yet

- StratCost PAAsDocument25 pagesStratCost PAAsanonymousNo ratings yet

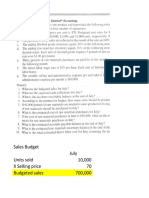

- Budgeting Sec BDocument8 pagesBudgeting Sec BanonymousNo ratings yet

- Group4 Case Study1 Hot Shot Plastic CompanyDocument14 pagesGroup4 Case Study1 Hot Shot Plastic CompanyanonymousNo ratings yet

- Budgeting: Solutions To QuestionsDocument64 pagesBudgeting: Solutions To Questionsمصطفى العادليNo ratings yet

- Post-Assessment (Long Quiz 3) - Attempt ReviewDocument22 pagesPost-Assessment (Long Quiz 3) - Attempt ReviewanonymousNo ratings yet

- Post Assessment Long Quiz 2 Attempt ReviewDocument35 pagesPost Assessment Long Quiz 2 Attempt ReviewanonymousNo ratings yet

- Chapter 1 Practice Test - Problems (Answers)Document12 pagesChapter 1 Practice Test - Problems (Answers)anonymousNo ratings yet

- Chapter 1 Illustrative Case 1 - AuditDocument7 pagesChapter 1 Illustrative Case 1 - AuditanonymousNo ratings yet

- Khilji Co Rate Card 2021 22Document14 pagesKhilji Co Rate Card 2021 22Khalid ButtNo ratings yet

- Impact of M&A on Tata Steel and Cours GroupDocument8 pagesImpact of M&A on Tata Steel and Cours Groupaashish0128No ratings yet

- Individual Work: Subject: The New York Stock Exchange: Market Capitalization, TrendsDocument8 pagesIndividual Work: Subject: The New York Stock Exchange: Market Capitalization, TrendsArina SapovalovaNo ratings yet

- Q.Discuss The Various Sources of Financing Working Capital. (OR) Q. Explain The Sources of Financing of Current AssetsDocument5 pagesQ.Discuss The Various Sources of Financing Working Capital. (OR) Q. Explain The Sources of Financing of Current AssetsSiva SankariNo ratings yet

- Forex StrategyDocument11 pagesForex StrategyNoman Khan100% (1)

- Authorised Charges For Document Writing in TamilnaduDocument2 pagesAuthorised Charges For Document Writing in Tamilnadumoghly100% (1)

- Millions of Dollars Except Per-Share DataDocument14 pagesMillions of Dollars Except Per-Share DataAjax0% (1)

- BPI UITF Client Suitability Assessment FormDocument6 pagesBPI UITF Client Suitability Assessment FormNorman PeñaNo ratings yet

- Topic 8 Internal ControlDocument16 pagesTopic 8 Internal ControlheyNo ratings yet

- Medina Guce Galindes Salanga 2018 Barangay Governance PDFDocument16 pagesMedina Guce Galindes Salanga 2018 Barangay Governance PDFPaulojoy BuenaobraNo ratings yet

- Halina Travel and Tours FINAL OUTPUTDocument66 pagesHalina Travel and Tours FINAL OUTPUTGene Justine SacdalanNo ratings yet

- HBR: Realize Your Customers' Fukk Profit PotentialDocument5 pagesHBR: Realize Your Customers' Fukk Profit PotentialAnuj AgarwalNo ratings yet

- The Relevance of Leverage, Profitability, Market Performance, and Macroeconomic To Stock PriceDocument11 pagesThe Relevance of Leverage, Profitability, Market Performance, and Macroeconomic To Stock PriceHalimahNo ratings yet

- Bonds valuation and amortization assessmentDocument2 pagesBonds valuation and amortization assessmentJohn FloresNo ratings yet

- Security Bank & Trust Company vs. Cuenca PDFDocument46 pagesSecurity Bank & Trust Company vs. Cuenca PDFRogie ApoloNo ratings yet

- Investment Avenues Available in BangladeshDocument16 pagesInvestment Avenues Available in BangladeshangelNo ratings yet

- Revenue Recognition MethodsDocument21 pagesRevenue Recognition Methodsbekbek12No ratings yet

- BAED-BFIN2121 Business Finance: Home BAED-BFIN2121-2122S Week 7: Sources of Funds I Learning Activity 002Document7 pagesBAED-BFIN2121 Business Finance: Home BAED-BFIN2121-2122S Week 7: Sources of Funds I Learning Activity 002Luisa RadaNo ratings yet

- CEO President VP Director CFO in California Resume David JosephDocument3 pagesCEO President VP Director CFO in California Resume David JosephDavid JosephNo ratings yet

- Manav's Salary SlipDocument1 pageManav's Salary SlipManav Unique WorldNo ratings yet

- The Warehouse Annual Report 2016Document96 pagesThe Warehouse Annual Report 2016Ngan PhamNo ratings yet

- PROBLEM EXERCISES IN TAXATION (Series 2019 - Part II) Prepared by Dr. Jeannie P. LimDocument16 pagesPROBLEM EXERCISES IN TAXATION (Series 2019 - Part II) Prepared by Dr. Jeannie P. LimXerjiah YuagaNo ratings yet

- Sol Q5Document3 pagesSol Q5Shubham RankaNo ratings yet

- Accounting For Management: Total No. of Questions 17Document2 pagesAccounting For Management: Total No. of Questions 17vikramvsuNo ratings yet

- Funded NextDocument1 pageFunded NextSathya PrakashNo ratings yet