You might also like

- TransFirst - Merchant - Card Processing - Operating - Guide - v6-0915Document139 pagesTransFirst - Merchant - Card Processing - Operating - Guide - v6-0915sreejaNo ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit Cardsomeonestupid19690% (1)

- Credit Card Processing A Look Inside The Black BoxDocument17 pagesCredit Card Processing A Look Inside The Black BoxNoOne100% (1)

- Equifax Online Dispute 5353011954 Synchrony BankDocument81 pagesEquifax Online Dispute 5353011954 Synchrony BankNeil Gillespie100% (1)

- Owing WorksheetDocument7 pagesOwing Worksheetapi-273999449No ratings yet

- Incoming Wire Instructions: Questions?Document2 pagesIncoming Wire Instructions: Questions?Niknjim PoseyNo ratings yet

- Important Full Forms and Abbreviations For Banking ExamsDocument12 pagesImportant Full Forms and Abbreviations For Banking Examspallavi D GNo ratings yet

- HK GRCC Platinum - Transfer-In App FormDocument1 pageHK GRCC Platinum - Transfer-In App FormpercysmithNo ratings yet

- Glossary - Payment Processing Terms From Chase PaymentechDocument24 pagesGlossary - Payment Processing Terms From Chase PaymentechPratibha Shetty100% (1)

- Pub CH Merchant ProcessingDocument90 pagesPub CH Merchant ProcessingMuumini De Souza NezzaNo ratings yet

- Please Use The Checking and Savings Account Application ToDocument3 pagesPlease Use The Checking and Savings Account Application ToGulrana AlamNo ratings yet

- The Financial Services Fact Book 2013Document263 pagesThe Financial Services Fact Book 2013Jay KabNo ratings yet

- Credit Card Statement (10) - UnlockedDocument2 pagesCredit Card Statement (10) - UnlockedAnand DNo ratings yet

- Clover Go ContractDocument9 pagesClover Go Contracttaoacu20000% (1)

- Boa CardDocument5 pagesBoa Cardapi-285069637100% (1)

- From Learning To Earning, We'll Help You All The Way.: A Guide To Your New Graduate AccountDocument16 pagesFrom Learning To Earning, We'll Help You All The Way.: A Guide To Your New Graduate Accountjordan25_93_75673196No ratings yet

- Collection LettersDocument32 pagesCollection LettersKaneez KaneezNo ratings yet

- Merchant Accounts Are Bank Accounts That Allow Your Business To Accept Card Payments From CustomersDocument43 pagesMerchant Accounts Are Bank Accounts That Allow Your Business To Accept Card Payments From CustomersRohit Kumar Baghel100% (1)

- $CASHOUTDocument22 pages$CASHOUTEnz DavieNo ratings yet

- Electronicpaymentppt 140601022736 Phpapp02Document13 pagesElectronicpaymentppt 140601022736 Phpapp02Vamshi100% (1)

- Ideposit Merchant ApplicationDocument4 pagesIdeposit Merchant Applicationcris4455No ratings yet

- Chap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFDocument7 pagesChap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFCarl James Austria100% (1)

- Family Dollar Paystub 24-04-2020 PDFDocument1 pageFamily Dollar Paystub 24-04-2020 PDFLuis MartinezNo ratings yet

- Check - A Bill of Exchange Drawn On A Bank Payable On Demand (Sec. 185)Document3 pagesCheck - A Bill of Exchange Drawn On A Bank Payable On Demand (Sec. 185)Caren deLeonNo ratings yet

- Telegraphic Transfer GuideDocument12 pagesTelegraphic Transfer GuideBenedict Wong Cheng WaiNo ratings yet

- Banking Operations: Cheques & EndorsementsDocument12 pagesBanking Operations: Cheques & EndorsementsSharath SaunshiNo ratings yet

- Keywordio Longtail KeywordsDocument8 pagesKeywordio Longtail KeywordsAkshat GroverNo ratings yet

- Debit Card & Credit Card: Presented By:-Amrish SaddamDocument22 pagesDebit Card & Credit Card: Presented By:-Amrish Saddamprakash singh bishtNo ratings yet

- SBI ATM Card To Card Money Transfer Through ATM - Latest InfoDocument8 pagesSBI ATM Card To Card Money Transfer Through ATM - Latest InfoviketjhaNo ratings yet

- MPR Grant Application - FinalDocument3 pagesMPR Grant Application - FinalWest Central TribuneNo ratings yet

- Credit CardsDocument21 pagesCredit Cardsdixita_chotalia3829100% (1)

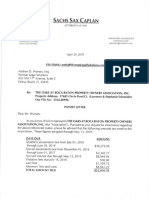

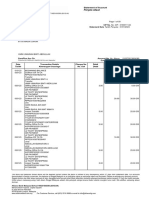

- Payoff Letter From Gonzalez, Counsel Sachs Sax Caplan For Oaks at Boca Raton Property Owners AssociationDocument4 pagesPayoff Letter From Gonzalez, Counsel Sachs Sax Caplan For Oaks at Boca Raton Property Owners Associationlarry-612445100% (1)

- Introduction To Accounting & Baiscs of JournalDocument227 pagesIntroduction To Accounting & Baiscs of Journaldateraj100% (1)

- Obligation and NegoDocument33 pagesObligation and NegoMichael ArevaloNo ratings yet

- 4 Causes of Action Were FiledDocument19 pages4 Causes of Action Were Filedzandree burgosNo ratings yet

- Ach Autharization FormDocument2 pagesAch Autharization FormAlexander Weir-WitmerNo ratings yet

- Traverlers Cheqes AssignmentDocument3 pagesTraverlers Cheqes AssignmentPradeep DhanushkaNo ratings yet

- A Seminar Report OnDocument27 pagesA Seminar Report OnKushal ShahNo ratings yet

- Ach Code CardDocument2 pagesAch Code CardSankaetPathakNo ratings yet

- Check Acceptance Procedure - RevisedDocument4 pagesCheck Acceptance Procedure - RevisedJoe EskenaziNo ratings yet

- CFPB Your Money Your Goals Choosing Paid ToolDocument6 pagesCFPB Your Money Your Goals Choosing Paid ToolJocelyn CyrNo ratings yet

- Payments 101 201709 v5 PDFDocument57 pagesPayments 101 201709 v5 PDFCarlos Pérez GonzálezNo ratings yet

- DocuSign PDFDocument7 pagesDocuSign PDFLourdesNo ratings yet

- Inside CRDocument18 pagesInside CRheadpncNo ratings yet

- Statement JAN PDFDocument59 pagesStatement JAN PDFUmay DelishaNo ratings yet

- Letter of Credit HardDocument35 pagesLetter of Credit HardReHopNo ratings yet

- Iphone 11 Imagine PDFDocument2 pagesIphone 11 Imagine PDFJonassy SumaïliNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Ashutosh SinhaNo ratings yet

- 04 RCBC Vs OdradaDocument1 page04 RCBC Vs OdradaJimenez LorenzNo ratings yet

- Merchant Account ChangeDocument1 pageMerchant Account Changeaglenn788934No ratings yet

- Arceo, Jr. Vs People of The PHDocument2 pagesArceo, Jr. Vs People of The PHToni CalsadoNo ratings yet

- Card Premium Bank Open Up For ACH and DD Carder404updateeDocument3 pagesCard Premium Bank Open Up For ACH and DD Carder404updateeoriarector782No ratings yet

- RFBT Challenge #2 AnswerkeyDocument5 pagesRFBT Challenge #2 Answerkeylovely cNo ratings yet

- Atms: Automated Teller MachinesDocument31 pagesAtms: Automated Teller MachinesOnkar KanadeNo ratings yet

- Black BookDocument28 pagesBlack BookAayat ShaikhNo ratings yet

- EziDebit - DDR Form - CompletePTDocument2 pagesEziDebit - DDR Form - CompletePTAndrewNeilYoungNo ratings yet

- Credit Card: Dr. Yamini Sharma D.M.SDocument31 pagesCredit Card: Dr. Yamini Sharma D.M.SJames RossNo ratings yet

- 61 Campos V. People of The Philippines and First Women'S Credit CorpDocument1 page61 Campos V. People of The Philippines and First Women'S Credit CorpGSSNo ratings yet

- YES Prosperity Credit Card MITC - 14052021Document8 pagesYES Prosperity Credit Card MITC - 14052021Prinshu TrivediNo ratings yet

- Card Acceptance Merchant Application FormDocument2 pagesCard Acceptance Merchant Application FormmikeNo ratings yet

- Credit Card Authorization Form: Thomas A. KeelerDocument1 pageCredit Card Authorization Form: Thomas A. KeelerThomas KeelerNo ratings yet

- Comercial BanksDocument21 pagesComercial BanksSanto AntonyNo ratings yet

- SUPERCARD Most Important Terms and Conditions (MITC)Document14 pagesSUPERCARD Most Important Terms and Conditions (MITC)Diwana Hai dilNo ratings yet

- Credit Card Cancellation FormDocument2 pagesCredit Card Cancellation Formwms_klangNo ratings yet

- Credit CardDocument3 pagesCredit Cardapi-371068989No ratings yet

- Payflowgateway GuideDocument256 pagesPayflowgateway GuidejojofunNo ratings yet

- Rules PDFDocument6 pagesRules PDFAshlynNo ratings yet

- Platinum Ser GuideDocument97 pagesPlatinum Ser GuideRohit RoyNo ratings yet

- PenskeDocument1 pagePenskeGiullz EuguiNo ratings yet

- SAIF Glossary - Workers CompDocument23 pagesSAIF Glossary - Workers CompGiullz EuguiNo ratings yet

- Ambulatory Care Services: Standard WorkDocument6 pagesAmbulatory Care Services: Standard WorkGiullz EuguiNo ratings yet

- Dial OutsDocument1 pageDial OutsGiullz EuguiNo ratings yet

- Consent Form Pelvic ExaminationDocument2 pagesConsent Form Pelvic ExaminationGiullz EuguiNo ratings yet

- HIPAA - FW & A ReviewDocument5 pagesHIPAA - FW & A ReviewGiullz EuguiNo ratings yet

- Guide On Handling Difficult Situations As A Medical InterpreterDocument15 pagesGuide On Handling Difficult Situations As A Medical InterpreterGiullz EuguiNo ratings yet

- Prime Bank Internship ReportDocument89 pagesPrime Bank Internship ReportTareqNo ratings yet

- CjbsDocument8 pagesCjbsRochak Agarwal0% (1)

- 1025i - Making Application To AusDocument3 pages1025i - Making Application To AusMild SevenNo ratings yet

- MTD Consultancy Services - RFP Document Word FileDocument179 pagesMTD Consultancy Services - RFP Document Word FileDevanshNuwalNo ratings yet

- Savings Account Statement: Capitec B AnkDocument1 pageSavings Account Statement: Capitec B AnkTshegofatso MosetlheNo ratings yet

- PFR Volume IDocument327 pagesPFR Volume IMaria WebbNo ratings yet

- 2020 NEQAS CC Registration Form and Order of PaymentDocument2 pages2020 NEQAS CC Registration Form and Order of PaymentNovie FeneciosNo ratings yet

- Jim Peron's Associations With The Adult and Child Sex' Movement (The Locke Foundation Report)Document32 pagesJim Peron's Associations With The Adult and Child Sex' Movement (The Locke Foundation Report)Nicolas MartinNo ratings yet

- D Min Dissertation Ver 3 Minatani 4.14.22Document114 pagesD Min Dissertation Ver 3 Minatani 4.14.22Corey MinataniNo ratings yet

- 1579924336896cioPXJ0dIGhcXSjl PDFDocument2 pages1579924336896cioPXJ0dIGhcXSjl PDFchennakesava rao veerapaneniNo ratings yet

- ILS AssessmentDocument12 pagesILS AssessmentjohnhaysNo ratings yet

- Assam Schedule IIIDocument4 pagesAssam Schedule IIIManash100% (1)

- Final Voucher SampleDocument3 pagesFinal Voucher SampleLeonard Anthony AperongNo ratings yet

- Project Report On PSB Bank For Intership TrainingDocument23 pagesProject Report On PSB Bank For Intership TrainingSrishti SinghNo ratings yet

- A. TheoryDocument10 pagesA. TheoryROMULO CUBID100% (1)

- Reliance Two Wheeler Package Policy - Schedule: Policy Number: 920222223121261091 Proposal/Covernote No: R01052205931Document6 pagesReliance Two Wheeler Package Policy - Schedule: Policy Number: 920222223121261091 Proposal/Covernote No: R01052205931MuraliMohanNo ratings yet

- GST - Payment ChallanDocument2 pagesGST - Payment ChallanPatel SumitNo ratings yet

- Internship Report On MCB Bank UsmanDocument61 pagesInternship Report On MCB Bank UsmanmajidNo ratings yet

- Prudential Bank v. Tupasi-ValenzuelaDocument9 pagesPrudential Bank v. Tupasi-ValenzuelaaitoomuchtvNo ratings yet

- Books of Prime Entry / JournalDocument23 pagesBooks of Prime Entry / JournalSai TejaNo ratings yet