You might also like

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- Credit AppraisalDocument6 pagesCredit AppraisalAnjali Angel ThakurNo ratings yet

- FIN 2101 Module Book - UpdatedDocument123 pagesFIN 2101 Module Book - UpdatedRay LowNo ratings yet

- The Insurance Act 1938Document26 pagesThe Insurance Act 1938Rahul Kumar80% (5)

- Blackstone and The Sale of Citigroup's Loan PortfolioDocument10 pagesBlackstone and The Sale of Citigroup's Loan PortfolioRonak Jain0% (1)

- This Study Resource Was: Biological Assets Question 21-1 Multiple Choice (PAS 41)Document6 pagesThis Study Resource Was: Biological Assets Question 21-1 Multiple Choice (PAS 41)Alexandra Nicole IsaacNo ratings yet

- Unit II Banking and Insurance Law Study NotesDocument12 pagesUnit II Banking and Insurance Law Study NotesSekar M KPRCAS-CommerceNo ratings yet

- Bank of The Philippine Islands-CisDocument9 pagesBank of The Philippine Islands-CisKershey SalacNo ratings yet

- ANTLMONEY LAUNDERING INNDIADocument12 pagesANTLMONEY LAUNDERING INNDIAanila rathodaNo ratings yet

- Constitution of Insurance Regulatory and Development AuthorityDocument27 pagesConstitution of Insurance Regulatory and Development Authoritymaha27No ratings yet

- 6 IRDADocument23 pages6 IRDASudha AgarwalNo ratings yet

- IRDADocument21 pagesIRDAJyoti SukhijaNo ratings yet

- Presented by Yashasvini Tharani Rashmi Vandana Devi PriyaDocument30 pagesPresented by Yashasvini Tharani Rashmi Vandana Devi PriyaRASHUNo ratings yet

- IRDA Regulation Relating To General InsuranceDocument14 pagesIRDA Regulation Relating To General InsurancerahulhaldankarNo ratings yet

- Irda (Insurance Regulatory & Development Authority)Document20 pagesIrda (Insurance Regulatory & Development Authority)harishkoppalNo ratings yet

- IRDAI Regulates India's Insurance SectorDocument7 pagesIRDAI Regulates India's Insurance SectorFaisal AhmadNo ratings yet

- Insurance Regulatory and Development Authority (Irda) : A Law of Insurance Project OnDocument5 pagesInsurance Regulatory and Development Authority (Irda) : A Law of Insurance Project OnAnju PanickerNo ratings yet

- IRDA Act SummaryDocument67 pagesIRDA Act SummaryVirendra JhaNo ratings yet

- Insurance Regulatory & Development Authority of India (IRDAI)Document10 pagesInsurance Regulatory & Development Authority of India (IRDAI)Deeptangshu KarNo ratings yet

- IRDADocument2 pagesIRDAJIYA DOSHINo ratings yet

- IRDA Act, 1999: Presentation OnDocument58 pagesIRDA Act, 1999: Presentation Ondeepakarora201188No ratings yet

- Mulund College of CommerceDocument11 pagesMulund College of CommerceashwitaNo ratings yet

- Calss PresentationDocument6 pagesCalss PresentationKasiNo ratings yet

- Unit 3 InsuranceDocument5 pagesUnit 3 InsuranceAkash SharmaNo ratings yet

- The Irda ActDocument3 pagesThe Irda ActAdeel RahmanNo ratings yet

- INSURANCE & IRDA REGULATIONSDocument33 pagesINSURANCE & IRDA REGULATIONSrajisumaNo ratings yet

- Malhotra Committee recommendations led to IRDA formationDocument4 pagesMalhotra Committee recommendations led to IRDA formationKanishq BawejaNo ratings yet

- Insurance Regulatory and Development AuthorityDocument12 pagesInsurance Regulatory and Development AuthorityVipin JacobNo ratings yet

- IntroductionDocument14 pagesIntroductionVedant NavalkarNo ratings yet

- IRDA PresentationDocument22 pagesIRDA PresentationSamhitha KandlakuntaNo ratings yet

- IRDAI's Role and FunctionsDocument5 pagesIRDAI's Role and FunctionsKirti ChotwaniNo ratings yet

- Presented By-Akhilesh (IMB2010008) : Insurance Regulatory and Development AuthorityDocument22 pagesPresented By-Akhilesh (IMB2010008) : Insurance Regulatory and Development Authoritybhuwanesh-man-rajbhandari-5259No ratings yet

- Insurance Law Notes RnDocument84 pagesInsurance Law Notes RnRudraksh NagarNo ratings yet

- The Relevance of Insurance Regulatory Authority of India in The Indian Insurance Sector IDocument12 pagesThe Relevance of Insurance Regulatory Authority of India in The Indian Insurance Sector IVaijayanti SharmaNo ratings yet

- Private Entry Insurance Sector GrowthDocument21 pagesPrivate Entry Insurance Sector GrowthSaurabh HampiNo ratings yet

- IrdaDocument15 pagesIrdaNitesh SudanNo ratings yet

- Unit - IV Banking and Insurance Law Study NotesDocument4 pagesUnit - IV Banking and Insurance Law Study NotesSekar M KPRCAS-CommerceNo ratings yet

- Insurance Regulatory and Development AuthorityDocument3 pagesInsurance Regulatory and Development AuthorityDeepak SharmaNo ratings yet

- Irda (Insurance Regulatory & Development Authority)Document22 pagesIrda (Insurance Regulatory & Development Authority)guru_shettiNo ratings yet

- Development Authority Act, 1999 and Duly Passed by The Government of IndiaDocument2 pagesDevelopment Authority Act, 1999 and Duly Passed by The Government of IndiaNancygirdherNo ratings yet

- Insurance Regulatory and Development Authority (IRDA)Document4 pagesInsurance Regulatory and Development Authority (IRDA)Chandini KambapuNo ratings yet

- Insurance - Unit 3&4Document20 pagesInsurance - Unit 3&4Dhruv GandhiNo ratings yet

- Development Authority (IRDA) Is A National Agency of The: Government of India HyderabadDocument5 pagesDevelopment Authority (IRDA) Is A National Agency of The: Government of India HyderabadSwarna RajpootNo ratings yet

- A Project Report OnDocument22 pagesA Project Report Onangel_ekta20079048No ratings yet

- IRDA Project - Akanksha - LLMDocument9 pagesIRDA Project - Akanksha - LLMPULKIT KHANDELWALNo ratings yet

- IRDA ActDocument11 pagesIRDA ActShaifali ChauhanNo ratings yet

- IrdaDocument10 pagesIrdafundoo16No ratings yet

- Insurance Regulatory and Development Authority of IndiaDocument6 pagesInsurance Regulatory and Development Authority of IndiaAkanksha PandeyNo ratings yet

- 09 Chapter 3Document32 pages09 Chapter 3palak2407No ratings yet

- Channi InsuranceDocument16 pagesChanni InsuranceSanjeev KashyapNo ratings yet

- Role of Final)Document37 pagesRole of Final)mamta_sawant25No ratings yet

- Role and Functions of India's Insurance Regulator IRDADocument3 pagesRole and Functions of India's Insurance Regulator IRDARaghav DhillonNo ratings yet

- IRDA by The DudesDocument13 pagesIRDA by The DudesAbhimanyu MaheshwariNo ratings yet

- Expectations: Duties, Powers and Functions of IRDADocument3 pagesExpectations: Duties, Powers and Functions of IRDAAlnoor PujaniNo ratings yet

- IRDADocument11 pagesIRDAkhrn_himanshuNo ratings yet

- Presented By: Sai Reddy Sravana Karthik V.B.RaoDocument29 pagesPresented By: Sai Reddy Sravana Karthik V.B.RaoSravana KarthikNo ratings yet

- IRDADocument12 pagesIRDAShreya PavithranNo ratings yet

- IRDADocument17 pagesIRDAHemant DeshmukhNo ratings yet

- Insurance Regulatory Framework: Main Reasons For Insurance Regulation IrdaiDocument12 pagesInsurance Regulatory Framework: Main Reasons For Insurance Regulation IrdaiIndeevar SarkarNo ratings yet

- Irda - IiiDocument15 pagesIrda - IiiB.Com (BI) CommerceNo ratings yet

- Unit - 6Document15 pagesUnit - 6Yaggendra GargNo ratings yet

- Authority of India (IRDA of India) After The Formal Declaration of Insurance Laws (Amendment)Document3 pagesAuthority of India (IRDA of India) After The Formal Declaration of Insurance Laws (Amendment)hima binduNo ratings yet

- Irda 1999Document15 pagesIrda 1999Charu LataNo ratings yet

- Institute of Management Studies Davv Indore Mba (Financial Administration) Ii ND Semester - Fa 303C Insurance and Bank ManagementDocument2 pagesInstitute of Management Studies Davv Indore Mba (Financial Administration) Ii ND Semester - Fa 303C Insurance and Bank ManagementjaiNo ratings yet

- Should Insurer Compensate Loss from RiotsDocument33 pagesShould Insurer Compensate Loss from RiotsKanchan GuptaNo ratings yet

- Optimizing Sales and Distribution of MilkDocument70 pagesOptimizing Sales and Distribution of MilkRavi Shankar SharmaNo ratings yet

- Unit - IV Banking and Insurance Law Study NotesDocument4 pagesUnit - IV Banking and Insurance Law Study NotesSekar M KPRCAS-CommerceNo ratings yet

- Banking and Insurance Unit III Study NotesDocument13 pagesBanking and Insurance Unit III Study NotesSekar M KPRCAS-CommerceNo ratings yet

- BANKING AND INSURANCE LAW HISTORYDocument12 pagesBANKING AND INSURANCE LAW HISTORYSekar M KPRCAS-CommerceNo ratings yet

- BANKING AND INSURANCE LAW MARK STATEMENTDocument2 pagesBANKING AND INSURANCE LAW MARK STATEMENTSekar M KPRCAS-CommerceNo ratings yet

- KPR College Marketing Management CourseDocument127 pagesKPR College Marketing Management CourseSekar M KPRCAS-CommerceNo ratings yet

- Canara BankDocument21 pagesCanara BankVinayNo ratings yet

- Financial ModuleDocument7 pagesFinancial ModuleVarad VinherkarNo ratings yet

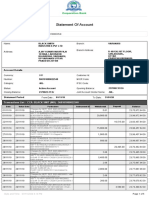

- Statement of AccountDocument5 pagesStatement of AccountAjay MauryaNo ratings yet

- IntangiblesworksheetDocument2 pagesIntangiblesworksheetammad uddinNo ratings yet

- Transaction HeaderDocument3 pagesTransaction HeaderطارقمجدىNo ratings yet

- Internship Report On Fsibl On Ratio AnalysisDocument32 pagesInternship Report On Fsibl On Ratio AnalysisAlamesu50% (2)

- A Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BankDocument67 pagesA Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BanklalsinghNo ratings yet

- Beams10e Ch07 Intercompany Profit Transactions BondsDocument25 pagesBeams10e Ch07 Intercompany Profit Transactions BondsIrma RismayantiNo ratings yet

- UPI: Understanding India's Unified Payments InterfaceDocument23 pagesUPI: Understanding India's Unified Payments InterfaceRITIK YADAVNo ratings yet

- IMPLEMENTING INDONESIA'S NEW HOUSING POLICY:THE WAY FORWARD. DraftDocument77 pagesIMPLEMENTING INDONESIA'S NEW HOUSING POLICY:THE WAY FORWARD. DraftOswar MungkasaNo ratings yet

- Valuation of Inventories.a Cost Basis ApproachDocument36 pagesValuation of Inventories.a Cost Basis ApproachMarvin Agustin De CastroNo ratings yet

- Loan Application ProcessDocument17 pagesLoan Application Processsamm yuuNo ratings yet

- Chapter 8 - Part ADocument22 pagesChapter 8 - Part AKwan Kwok AsNo ratings yet

- Project Report On Risk MGT in Life InsuranceDocument77 pagesProject Report On Risk MGT in Life InsuranceAlpatron shit'sNo ratings yet

- 02 Edu91 FM Practice Sheets QuestionsDocument77 pages02 Edu91 FM Practice Sheets Questionsprince soniNo ratings yet

- Askari Bank Personal Loan CBD Excel SheetDocument4 pagesAskari Bank Personal Loan CBD Excel Sheetsumbul imranNo ratings yet

- Group 3 Financial MarketsDocument17 pagesGroup 3 Financial MarketsLady Lou Ignacio LepasanaNo ratings yet

- Merchant Banking Research PaperDocument3 pagesMerchant Banking Research PaperSajid ShaikhNo ratings yet

- HIG 2012 - Model Test PromptDocument2 pagesHIG 2012 - Model Test PromptLoïc HalleuxNo ratings yet

- Calculate LTV ratio and monthly amortizationDocument4 pagesCalculate LTV ratio and monthly amortizationMichelle GozonNo ratings yet

- Cash and Cash Equivalents PDFDocument7 pagesCash and Cash Equivalents PDFFritzey Faye RomeronaNo ratings yet

- Nike Financial Analysis - EditedDocument12 pagesNike Financial Analysis - EditedmosesNo ratings yet

- Corporate Governance RatingsDocument3 pagesCorporate Governance RatingsSOHEL ALAM 17BBLB050No ratings yet

- Bpi Endorsement LetterDocument1 pageBpi Endorsement Letterthesamgyup31No ratings yet