You might also like

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Chema LiteDocument8 pagesChema LiteHàMềmNo ratings yet

- 2021 Unit 7 Tutorial QuestionsDocument6 pages2021 Unit 7 Tutorial Questions日日日No ratings yet

- 11&13quiz For Exam4Document16 pages11&13quiz For Exam4Amanda ThurstonNo ratings yet

- Question 44 (65 Minutes) (Chapters 11, 12) : NotesDocument2 pagesQuestion 44 (65 Minutes) (Chapters 11, 12) : Notesromie2bNo ratings yet

- Taxation-Ii: (A) What Do You Mean by "Arm's Length Price" and What Are The Methods To Be Used For TheDocument4 pagesTaxation-Ii: (A) What Do You Mean by "Arm's Length Price" and What Are The Methods To Be Used For Theswarna dasNo ratings yet

- Questions Chapter 10Document21 pagesQuestions Chapter 10SA 10No ratings yet

- Chapter 7 PDFDocument18 pagesChapter 7 PDFJay BrockNo ratings yet

- MT Test Review-Taxation 1-Win 2024Document4 pagesMT Test Review-Taxation 1-Win 2024Mariola AlkuNo ratings yet

- Accounting/Series 4 2007 (Code3001)Document17 pagesAccounting/Series 4 2007 (Code3001)Hein Linn Kyaw100% (2)

- M.B.A (2016 Pattern)Document39 pagesM.B.A (2016 Pattern)Radha ChoudhariNo ratings yet

- F7 SolutionsDocument15 pagesF7 Solutionsnoor ul anumNo ratings yet

- 2021 - A2S2 Solution-OplossingDocument19 pages2021 - A2S2 Solution-OplossingmeghdyckNo ratings yet

- Accounting (IAS) /series 4 2007 (Code3901)Document17 pagesAccounting (IAS) /series 4 2007 (Code3901)Hein Linn Kyaw0% (1)

- Tax (SEM. VI) 2019 PATTERNDocument4 pagesTax (SEM. VI) 2019 PATTERNganuNo ratings yet

- II PUC ACC REVISED POQs FOR 2022-23Document3 pagesII PUC ACC REVISED POQs FOR 2022-23Shree Lakshmi vNo ratings yet

- Principles of Taxation ND2020Document2 pagesPrinciples of Taxation ND2020Sharif MahmudNo ratings yet

- Test 3 Tax SolutionsDocument17 pagesTest 3 Tax SolutionsManjulaNo ratings yet

- DT - Test 2 - D23 - NSDocument3 pagesDT - Test 2 - D23 - NSMadhav TailorNo ratings yet

- Division "A": VIDYA SAGAR CAREER INSTITUTE LIMITED, Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54Document281 pagesDivision "A": VIDYA SAGAR CAREER INSTITUTE LIMITED, Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54mktg.seagullshippingNo ratings yet

- As GR 1 Ipcc Compiler 2015-18Document24 pagesAs GR 1 Ipcc Compiler 2015-18KRISHNA MANDLOINo ratings yet

- Zimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3Document7 pagesZimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3chauromweaNo ratings yet

- FSA - Tutorial 6-Fall 2023 With SolutionsDocument5 pagesFSA - Tutorial 6-Fall 2023 With SolutionsnourbenmiledtbsNo ratings yet

- Income Tax IISep Oct 2022Document15 pagesIncome Tax IISep Oct 2022supritha724No ratings yet

- 02 AddDocument14 pages02 AddHà My NguyễnNo ratings yet

- 9706 31 Insert M J 20Document8 pages9706 31 Insert M J 20chirag mehtaNo ratings yet

- National University of Science and TechnologyDocument5 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- ACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalDocument8 pagesACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalMercy Jerop KimutaiNo ratings yet

- Section A Answer ALL Questions in This SectionDocument4 pagesSection A Answer ALL Questions in This SectionBright MuzaNo ratings yet

- Control No 3 V MF XXVIII Tema B SolucionarioDocument7 pagesControl No 3 V MF XXVIII Tema B SolucionarioJohnny TrujilloNo ratings yet

- Liab, SHE, CashvsAccrual, BV & EPSDocument5 pagesLiab, SHE, CashvsAccrual, BV & EPSMimiNo ratings yet

- 01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022Document6 pages01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022hermitpassiNo ratings yet

- Unit 5 - Depreciation - Chat Session 8 (Spring 2020)Document5 pagesUnit 5 - Depreciation - Chat Session 8 (Spring 2020)RealGenius (Carl)No ratings yet

- Practice Problems 3Document6 pagesPractice Problems 3Luigi NocitaNo ratings yet

- Bcom TaxDocument6 pagesBcom TaxAditya .cNo ratings yet

- Management and Cost Accounting 10th Edition Drury Solutions ManualDocument17 pagesManagement and Cost Accounting 10th Edition Drury Solutions Manualeliasvykh6in8100% (27)

- Management and Cost Accounting 10th Edition Drury Solutions Manual Full Chapter PDFDocument38 pagesManagement and Cost Accounting 10th Edition Drury Solutions Manual Full Chapter PDFirisdavid3n8lg100% (10)

- Acc BetaDocument11 pagesAcc BetaHamiz AizuddinNo ratings yet

- Johnson - Cassandra - AC556 Assignment Unit 4Document9 pagesJohnson - Cassandra - AC556 Assignment Unit 4ctp4950_552446766No ratings yet

- tst2f90 Ws PDFDocument10 pagestst2f90 Ws PDFUtsukushī SaigaiNo ratings yet

- ACY 53 Summative Exam 2 CH 26 28 Answer KeyDocument3 pagesACY 53 Summative Exam 2 CH 26 28 Answer KeyAMIKO OHYANo ratings yet

- CGT 1Document25 pagesCGT 1Donald HollistNo ratings yet

- T04 - Profits TaxDocument18 pagesT04 - Profits Taxting ting shihNo ratings yet

- Chapter 11 SolutionsDocument22 pagesChapter 11 SolutionsChander Santos Monteiro100% (3)

- Workshop 2 - Questions - Introduction To Accounting and FinanceDocument7 pagesWorkshop 2 - Questions - Introduction To Accounting and FinanceSu FangNo ratings yet

- AMIS 525 Pop Quiz - Chapter 21: A) The Net Present Value of Project C Will Be The HighestDocument3 pagesAMIS 525 Pop Quiz - Chapter 21: A) The Net Present Value of Project C Will Be The HighestDan Andrei Bongo100% (1)

- CA Final DT A MTP 1 May 23Document14 pagesCA Final DT A MTP 1 May 23Mayur JoshiNo ratings yet

- Ilovepdf MergedDocument84 pagesIlovepdf MergedVinay DugarNo ratings yet

- P6-Corporation TaxDocument16 pagesP6-Corporation TaxAnonymous rePT5rCrNo ratings yet

- Audit of Liabilities Quiz 3Document3 pagesAudit of Liabilities Quiz 3Cattleya50% (2)

- Accounting Final Mock 1 2023Document13 pagesAccounting Final Mock 1 2023diya pNo ratings yet

- Advanced Taxation-Previous YearDocument4 pagesAdvanced Taxation-Previous YearObeng CliffNo ratings yet

- TIE5205201505 Business Studies IV Financial AnalysisDocument12 pagesTIE5205201505 Business Studies IV Financial AnalysisMarlon KamupiraNo ratings yet

- CA Ipcc Taxation Suggested Answers For Nov 2016Document16 pagesCA Ipcc Taxation Suggested Answers For Nov 2016Sai Kumar SandralaNo ratings yet

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- J.K. Lasser's Your Income Tax 2024, Professional EditionFrom EverandJ.K. Lasser's Your Income Tax 2024, Professional EditionNo ratings yet

- Self-Practice Exercise Pack-DFD-2021-22-T2-Jan 2022Document23 pagesSelf-Practice Exercise Pack-DFD-2021-22-T2-Jan 2022LIAW ANN YINo ratings yet

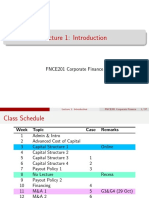

- Lecture 3: Capital Structure 1: FNCE201 Corporate FinanceDocument48 pagesLecture 3: Capital Structure 1: FNCE201 Corporate FinanceLIAW ANN YINo ratings yet

- Quick Check-Exp Cycle-Suggested Solution-Feb 2022Document7 pagesQuick Check-Exp Cycle-Suggested Solution-Feb 2022LIAW ANN YINo ratings yet

- WK 5-Session 5 Notes-Continuous Prob-UploadDocument13 pagesWK 5-Session 5 Notes-Continuous Prob-UploadLIAW ANN YINo ratings yet

- WK 11-Session 11 Notes-Hypothesis Testing (Two Samples) - UploadDocument12 pagesWK 11-Session 11 Notes-Hypothesis Testing (Two Samples) - UploadLIAW ANN YINo ratings yet

- Week 4 - Class ExerciseDocument18 pagesWeek 4 - Class ExerciseLIAW ANN YINo ratings yet

- ACCT418 - AY2122 - T2 - Sample Exam - With AnswersDocument8 pagesACCT418 - AY2122 - T2 - Sample Exam - With AnswersLIAW ANN YINo ratings yet

- ACCT223 AY 21 22 Mid-Term AnswersDocument5 pagesACCT223 AY 21 22 Mid-Term AnswersLIAW ANN YINo ratings yet

- Revenue Cycle - DFDs-ControlMatrix-2022Document13 pagesRevenue Cycle - DFDs-ControlMatrix-2022LIAW ANN YINo ratings yet

- Week 2-1 SlidesDocument30 pagesWeek 2-1 SlidesLIAW ANN YINo ratings yet

- WK 10-Session 10 Notes-Hypothesis Testing (One Sample) - Upload-UpdatedDocument24 pagesWK 10-Session 10 Notes-Hypothesis Testing (One Sample) - Upload-UpdatedLIAW ANN YINo ratings yet

- Database Design - Seminar Illustration Handout - 2022Document11 pagesDatabase Design - Seminar Illustration Handout - 2022LIAW ANN YINo ratings yet

- Week 2 Slides (O&a)Document46 pagesWeek 2 Slides (O&a)LIAW ANN YINo ratings yet

- Lecture 1 IntroductionDocument37 pagesLecture 1 IntroductionLIAW ANN YINo ratings yet

- Seminar 4 Internal Control - StudentDocument49 pagesSeminar 4 Internal Control - StudentLIAW ANN YINo ratings yet

- Lecture 5: Capital Structure 3 Lecture 5: Capital Structure 3Document10 pagesLecture 5: Capital Structure 3 Lecture 5: Capital Structure 3LIAW ANN YINo ratings yet

- Seminar 4 Internal Control - InstructorDocument54 pagesSeminar 4 Internal Control - InstructorLIAW ANN YINo ratings yet

- Lecture 6 FinalDocument30 pagesLecture 6 FinalLIAW ANN YINo ratings yet

- Seminar 1 Assurance Governance and Fraud - Student (1) AnnotatedDocument53 pagesSeminar 1 Assurance Governance and Fraud - Student (1) AnnotatedLIAW ANN YINo ratings yet

- Seminar 5 Audit Evidence - StudentDocument48 pagesSeminar 5 Audit Evidence - StudentLIAW ANN YINo ratings yet

- L2 ACoC G5Document52 pagesL2 ACoC G5LIAW ANN YINo ratings yet

- Tax Homework Chapter 6Document4 pagesTax Homework Chapter 6RosShanique ColebyNo ratings yet

- 2316 Chairman Public School TeacherDocument1 page2316 Chairman Public School TeacherCASUNCAD, GANIE MAE T.No ratings yet

- Translation Taxslipf28Document1 pageTranslation Taxslipf28Ya LiNo ratings yet

- Mahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahDocument4 pagesMahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahMUHAMMAD SALEEM RAZANo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- First StepDocument5 pagesFirst StepBhupendra Nagesh67% (3)

- Summary Regulation CPA NotesDocument2 pagesSummary Regulation CPA Notesjklein2588100% (1)

- Report 1Document2 pagesReport 1Raashid Qyidar Aqiel ElNo ratings yet

- Salient Features of CREATE LawDocument2 pagesSalient Features of CREATE LawJean TomugdanNo ratings yet

- Roxas v. CTADocument2 pagesRoxas v. CTAJoyce Espiritu100% (1)

- TX2 101Document3 pagesTX2 101Pau SantosNo ratings yet

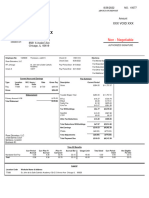

- Tax Invoice: Bhadrak Gstin/Uin: 21AAKFP2695N1ZR State Name: Odisha, Code: 21Document1 pageTax Invoice: Bhadrak Gstin/Uin: 21AAKFP2695N1ZR State Name: Odisha, Code: 21Ashish ParidaNo ratings yet

- Salaryslip June 2022Document1 pageSalaryslip June 2022Anup Kumar sharmaNo ratings yet

- SS Line 1Document3 pagesSS Line 1marlenemartinez119No ratings yet

- E Tax 20200504201259Document3 pagesE Tax 20200504201259monitganatra100% (1)

- Crrptreport - 2023-07-27T145326.989Document1 pageCrrptreport - 2023-07-27T145326.989MAHA AutomationsNo ratings yet

- Amended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesDocument2 pagesAmended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesKel TranNo ratings yet

- Fabm Week 1 Asnd 2Document5 pagesFabm Week 1 Asnd 2John Calvin GerolaoNo ratings yet

- Assignment III-LGS311-12th-DECDocument2 pagesAssignment III-LGS311-12th-DECMohammad Iqbal SekandariNo ratings yet

- Faris Handsome PunyaDocument12 pagesFaris Handsome PunyaYanNo ratings yet

- BAM 208 - P2 Quiz #2Document4 pagesBAM 208 - P2 Quiz #2trishaNo ratings yet

- Republic v. Razon and Jai Alai CorporationDocument3 pagesRepublic v. Razon and Jai Alai CorporationYanz RamsNo ratings yet

- RMC 102-2017 HighlightsDocument3 pagesRMC 102-2017 HighlightsmmeeeowwNo ratings yet

- 5th Chapter Assessement of IndividualDocument13 pages5th Chapter Assessement of IndividualManjunath R IligerNo ratings yet

- UV Plastic Manufacturing: Estimate/QuotationDocument1 pageUV Plastic Manufacturing: Estimate/QuotationManoj EmmidesettyNo ratings yet

- Dinsha C001 200905 2023057263210824609387135Document1 pageDinsha C001 200905 2023057263210824609387135pradeepppatil12No ratings yet

- IRS Publication 15 Withholding Tax Tables 2010Document73 pagesIRS Publication 15 Withholding Tax Tables 2010Wayne Schulz100% (1)

- Tax Invoice ELITE TRADERS - 2019-2020 1810 20-Feb-2020: MM EnterprisesDocument1 pageTax Invoice ELITE TRADERS - 2019-2020 1810 20-Feb-2020: MM EnterprisesALPHA INTERNET CAFENo ratings yet

- Commissioner of Internal Revenue vs. Mcgeorge Food Industries, IncDocument1 pageCommissioner of Internal Revenue vs. Mcgeorge Food Industries, IncRaquel DoqueniaNo ratings yet

- US Acceptable DocumentationDocument5 pagesUS Acceptable DocumentationMargie LamarreNo ratings yet