You might also like

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Absorption and Variable Costing: Types of Product Costing MethodDocument2 pagesAbsorption and Variable Costing: Types of Product Costing MethodKuya ANo ratings yet

- D - Absorption and Variable CostingDocument5 pagesD - Absorption and Variable Costingian dizonNo ratings yet

- Variable and Absorption CostingDocument2 pagesVariable and Absorption CostingLaura OliviaNo ratings yet

- 1491820614costing by CA Jitender Singh (Overhead, Labour, Material, Marginal, Ratio, Machine Hour RateDocument311 pages1491820614costing by CA Jitender Singh (Overhead, Labour, Material, Marginal, Ratio, Machine Hour RateRam IyerNo ratings yet

- Mas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsDocument3 pagesMas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsClyde RamosNo ratings yet

- Absorption MarginalDocument17 pagesAbsorption MarginalSHIVANSH BANSALNo ratings yet

- Module 4 Absorption and Variable Costing NotesDocument3 pagesModule 4 Absorption and Variable Costing NotesMadielyn Santarin Miranda100% (3)

- Marginal Costing TYBAFDocument13 pagesMarginal Costing TYBAFAkash BugadeNo ratings yet

- Absorption and Marginal CostingDocument19 pagesAbsorption and Marginal CostingsadikzeenatNo ratings yet

- MODULE 1 Variable and Absorption CostingDocument9 pagesMODULE 1 Variable and Absorption Costingjerico garciaNo ratings yet

- Topic 3 Variable Costing and Absorption CostingDocument3 pagesTopic 3 Variable Costing and Absorption CostingdigididoghakdogNo ratings yet

- Mas 02 - CVPDocument24 pagesMas 02 - CVPAlexis RiveraNo ratings yet

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingDhona Mae FidelNo ratings yet

- Profit Modelling Variable Costing Absorption CostingDocument17 pagesProfit Modelling Variable Costing Absorption CostingLeslie Beltran ChiangNo ratings yet

- Absorption Vs VariableDocument10 pagesAbsorption Vs VariableRonie Macasabuang CardosaNo ratings yet

- Lecture-9.1 Variable & Absorption Costing PDFDocument24 pagesLecture-9.1 Variable & Absorption Costing PDFNazmul-Hassan Sumon100% (1)

- Lecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmDocument41 pagesLecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmmurtaza haiderNo ratings yet

- STCM 03AbsorptionandVariableCostingDocument5 pagesSTCM 03AbsorptionandVariableCostingdin matanguihanNo ratings yet

- Absorption and Variable Costing NotesDocument4 pagesAbsorption and Variable Costing NotesGerald Nitz PonceNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- Module - Absorption and Variable CostingDocument10 pagesModule - Absorption and Variable CostingUchayya100% (1)

- Management Advisory Services NotesDocument2 pagesManagement Advisory Services NotesKyla RoxasNo ratings yet

- 3MA 03 Absortion and Variable CostingDocument3 pages3MA 03 Absortion and Variable CostingAbigail Regondola BonitaNo ratings yet

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- Strat Cost Handout 02 CVP Analysis Updated 0212 - CompressDocument17 pagesStrat Cost Handout 02 CVP Analysis Updated 0212 - CompressAerwyna AfarinNo ratings yet

- Costman Variable CostingDocument2 pagesCostman Variable CostingJeremi BernardoNo ratings yet

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- Notes in SCM Chapter 3: Product CostingDocument2 pagesNotes in SCM Chapter 3: Product CostingMy PhotographsNo ratings yet

- OR Cost of Inventory: Absorption Costing Variable CostingDocument2 pagesOR Cost of Inventory: Absorption Costing Variable CostingKim TaehyungNo ratings yet

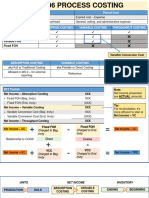

- MS 06-06 Process CostingDocument6 pagesMS 06-06 Process CostingxernathanNo ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Absorption and Variable CostingDocument22 pagesAbsorption and Variable CostingJamaica David100% (4)

- 04 Variable and Absorption CostingDocument8 pages04 Variable and Absorption CostingJunZon VelascoNo ratings yet

- Cost and Management Accounting Unit 2Document38 pagesCost and Management Accounting Unit 2Minisha GuptaNo ratings yet

- STRATCOST Quiz 2 Reviewer by Diamla, Foronda, GanDocument15 pagesSTRATCOST Quiz 2 Reviewer by Diamla, Foronda, GanAhga MoonNo ratings yet

- CMA-Unit 5 - Absorbtion Costing, Operation Costing & by Product Costing - 18-19Document23 pagesCMA-Unit 5 - Absorbtion Costing, Operation Costing & by Product Costing - 18-19rohit vermaNo ratings yet

- Mas - Absorption and Variable Costing PDFDocument11 pagesMas - Absorption and Variable Costing PDFNicole Anne M. ManansalaNo ratings yet

- Management Accounting Absorption and Variable Costing Absorption CostingDocument10 pagesManagement Accounting Absorption and Variable Costing Absorption CostingnaddieNo ratings yet

- CVP TheoryDocument7 pagesCVP Theoryhassan malikNo ratings yet

- CVP AnalysisDocument18 pagesCVP Analysiskhyla Marie NooraNo ratings yet

- Week 3 Absorption VariableDocument21 pagesWeek 3 Absorption VariableHallie KuronumaNo ratings yet

- Cost Acc 2nd Term ReviewerDocument20 pagesCost Acc 2nd Term ReviewerMary Mia CenizaNo ratings yet

- Absorption and Variable CostingDocument20 pagesAbsorption and Variable CostingEarl EzekielNo ratings yet

- Absorption Variable Costing1Document3 pagesAbsorption Variable Costing1Jasmine LimNo ratings yet

- Module 3 CVP and Breakeven AnalysisDocument4 pagesModule 3 CVP and Breakeven Analysiskhaireyah hashimNo ratings yet

- F2-08 Absorption and Marginal CostingDocument16 pagesF2-08 Absorption and Marginal CostingJaved ImranNo ratings yet

- Topic 7 - Absorption & Marginal CostingDocument8 pagesTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- Marginal CostDocument12 pagesMarginal CostShakyaprabha RoyNo ratings yet

- Review Session 01 MA Topics 1-6 BeforeDocument32 pagesReview Session 01 MA Topics 1-6 BeforemisalNo ratings yet

- Review Session 01 MA Topics 1-6 AfterDocument32 pagesReview Session 01 MA Topics 1-6 AftermisalNo ratings yet

- Mas-03: Absorption & Variable CostingDocument4 pagesMas-03: Absorption & Variable CostingClint AbenojaNo ratings yet

- Ringkasan Materi - Akuntansi ManajemenDocument7 pagesRingkasan Materi - Akuntansi ManajemenFahmi Nur AlfiyanNo ratings yet

- SIM - Variable and Absorption Costing - 0Document5 pagesSIM - Variable and Absorption Costing - 0lilienesieraNo ratings yet

- Chapter 9 Standard Costing - SynopsisDocument8 pagesChapter 9 Standard Costing - SynopsissajedulNo ratings yet

- T10 - NoteDocument7 pagesT10 - NoterbnbalachandranNo ratings yet

- Module 4 Absorption Variable Throughput CostingDocument3 pagesModule 4 Absorption Variable Throughput CostingSky Soronoi100% (1)

- Module 4 Absorption Variable Throughput CostingDocument3 pagesModule 4 Absorption Variable Throughput CostingSky SoronoiNo ratings yet

- MR Hamad S.HajiDocument26 pagesMR Hamad S.HajiNoronha Company LimitedNo ratings yet

- CH 10 NotesDocument13 pagesCH 10 NotesmohamedNo ratings yet

- Midterm ReviewerDocument4 pagesMidterm ReviewerMarriah Izzabelle Suarez RamadaNo ratings yet

- Management Advisory Services: Costs and Cost ConceptsDocument45 pagesManagement Advisory Services: Costs and Cost ConceptsUnknown 01No ratings yet

- Corporate GovernanceDocument3 pagesCorporate GovernanceMarriah Izzabelle Suarez RamadaNo ratings yet

- Health Declaration FormDocument1 pageHealth Declaration FormMarriah Izzabelle Suarez RamadaNo ratings yet

- 07 Module 03 AVC PDFDocument12 pages07 Module 03 AVC PDFMarriah Izzabelle Suarez RamadaNo ratings yet

- Quiz 1: Basic ConsiderationsDocument4 pagesQuiz 1: Basic ConsiderationsMarriah Izzabelle Suarez RamadaNo ratings yet

- LM 1 Basic ConsiderationsDocument6 pagesLM 1 Basic ConsiderationsMarriah Izzabelle Suarez RamadaNo ratings yet

- LM 2 Mas Cost EstimationDocument2 pagesLM 2 Mas Cost EstimationMarriah Izzabelle Suarez RamadaNo ratings yet

- Working Capital ManagementDocument5 pagesWorking Capital ManagementMarriah Izzabelle Suarez RamadaNo ratings yet

- Gipa SearchDocument5 pagesGipa SearchMarriah Izzabelle Suarez RamadaNo ratings yet

- QuestionsDocument3 pagesQuestionsUgaas DirieNo ratings yet

- Johnson Beverage CaseDocument5 pagesJohnson Beverage CaseKom Boonna100% (2)

- Group 1 Pa204 Public Administration and Management An Introduction 1Document23 pagesGroup 1 Pa204 Public Administration and Management An Introduction 1Marivic Penarubia100% (1)

- Stellarleack Business PlanDocument14 pagesStellarleack Business Planleackyotieno4No ratings yet

- Human Resource PlanningDocument45 pagesHuman Resource PlanningVora Kevin100% (6)

- Developing Creative Leadership in A Public Service OrganisationDocument11 pagesDeveloping Creative Leadership in A Public Service OrganisationAzim MohammedNo ratings yet

- Action Research HandoutDocument2 pagesAction Research HandoutgeethamadhuNo ratings yet

- MBO Unit 2Document21 pagesMBO Unit 2vimalaNo ratings yet

- ACC Vs DJC CaseletDocument2 pagesACC Vs DJC CaseletErin ComptonNo ratings yet

- STANDARD COSTING and Variance AnalysisDocument28 pagesSTANDARD COSTING and Variance AnalysisDanica VillaganteNo ratings yet

- SAG GRC Audit-Management WP Feb12 Print 0Document14 pagesSAG GRC Audit-Management WP Feb12 Print 0sdm_pedroNo ratings yet

- Human Resource ManagementDocument7 pagesHuman Resource ManagementT S Kumar KumarNo ratings yet

- Center of Excellence (COE)Document6 pagesCenter of Excellence (COE)sridhar_ee100% (1)

- W11-Course Descriptions FINDocument163 pagesW11-Course Descriptions FINjalnajjaNo ratings yet

- Newell's Corporate StrategyDocument1 pageNewell's Corporate StrategyAmogh Suman0% (1)

- A Study On Inventory ManagementDocument6 pagesA Study On Inventory ManagementMahaManthra100% (1)

- College Management Project PlanDocument7 pagesCollege Management Project PlanC TharmaNo ratings yet

- Sap (STRATEGIC ADVANTAGE PROFILE.)Document9 pagesSap (STRATEGIC ADVANTAGE PROFILE.)Shubhajit Nandi83% (12)

- Business Continuity Planning Audit Work Program Sample 3Document19 pagesBusiness Continuity Planning Audit Work Program Sample 3Juan Pascual CosareNo ratings yet

- BSBOPS502 Student Project Portfolio - Jacob Lloyd JonesDocument19 pagesBSBOPS502 Student Project Portfolio - Jacob Lloyd JonesBui AnNo ratings yet

- Vacancy Farm Manager - Elite Plants - NyahururuDocument2 pagesVacancy Farm Manager - Elite Plants - Nyahururututorfelix777No ratings yet

- NSTP-CWTS Syllabus Prelim-MidtermDocument16 pagesNSTP-CWTS Syllabus Prelim-MidtermKobe BryNo ratings yet

- Entrepreneurship IntroductionDocument25 pagesEntrepreneurship IntroductionRoveline GenonNo ratings yet

- Cross DockingDocument12 pagesCross DockingpisoyNo ratings yet

- Chapter 5 - PROCESS SELECTIONDocument8 pagesChapter 5 - PROCESS SELECTIONLong Đoàn PhiNo ratings yet

- Buygrid Framework Buygrid Framework: DescriptionDocument2 pagesBuygrid Framework Buygrid Framework: DescriptionSreekant100% (1)

- Solution To Assignment 1Document3 pagesSolution To Assignment 1Khyla DivinagraciaNo ratings yet

- Chapter 5Document18 pagesChapter 5Ezaz ChowdhuryNo ratings yet

- DFD of Ford Purchasing SystemDocument27 pagesDFD of Ford Purchasing SystemAdam OngNo ratings yet

- Industrial STPDocument9 pagesIndustrial STPraveendramanipalNo ratings yet