You might also like

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Financial ServicesDocument10 pagesFinancial ServicesDinesh Sugumaran100% (4)

- Acca f6 Smart Notes Fa19 40 PagesDocument43 pagesAcca f6 Smart Notes Fa19 40 PagesAlex RomarioNo ratings yet

- Lala2017 Audit ReportDocument146 pagesLala2017 Audit ReportEm SanNo ratings yet

- C0.Entreprenuership 5th Ed BarringerDocument8 pagesC0.Entreprenuership 5th Ed BarringermnornajamudinNo ratings yet

- COA Cir No. 2009-001-Submission of Pos, ContractsDocument28 pagesCOA Cir No. 2009-001-Submission of Pos, Contractscrizalde de dios100% (1)

- NFJPIA - Mockboard 2011 - MAS PDFDocument7 pagesNFJPIA - Mockboard 2011 - MAS PDFAbigail Faye RoxasNo ratings yet

- Basic Accounting Training for Non-AccountantsDocument123 pagesBasic Accounting Training for Non-Accountantsnelia d. onteNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- San Miguel Executive Summary 2011Document12 pagesSan Miguel Executive Summary 2011Justine CastilloNo ratings yet

- Esperanza Executive Summary 2011Document5 pagesEsperanza Executive Summary 2011Rowena MahusayNo ratings yet

- Executive Summary: in Thousands of PesosDocument6 pagesExecutive Summary: in Thousands of PesosDAS MAGNo ratings yet

- Municipal Financials and Audit Report SummaryDocument5 pagesMunicipal Financials and Audit Report SummaryThe ApprenticeNo ratings yet

- Aurora Executive Summary 2012Document7 pagesAurora Executive Summary 2012Mary Joy Sedenio LopezNo ratings yet

- 01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009Document50 pages01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009himamaylancitywatchNo ratings yet

- San Miguel Executive Summary 2012Document4 pagesSan Miguel Executive Summary 2012imnikki.gonzalesNo ratings yet

- San Agustin Executive Summary 2018Document4 pagesSan Agustin Executive Summary 2018minds2magicNo ratings yet

- Executive Summary: A. IntroductionDocument6 pagesExecutive Summary: A. IntroductionCrislyn BayawaNo ratings yet

- Alegria Executive Summary 2015Document8 pagesAlegria Executive Summary 2015Reyna YlenaNo ratings yet

- Executive Summary of Lugait Municipality Audit ReportDocument4 pagesExecutive Summary of Lugait Municipality Audit ReportOZ La NB AnamiNo ratings yet

- KalingaProv ES2015Document4 pagesKalingaProv ES2015J JaNo ratings yet

- CebuCity ES08Document7 pagesCebuCity ES08Jess JessNo ratings yet

- Dasmariñas City 2020 Financial ReportDocument228 pagesDasmariñas City 2020 Financial ReportJuswa DanyelNo ratings yet

- Guimba Executive Summary 2014Document5 pagesGuimba Executive Summary 2014Winter KimNo ratings yet

- Titay ZS ES2016Document5 pagesTitay ZS ES2016J JaNo ratings yet

- Oton Executive Summary 2017Document5 pagesOton Executive Summary 2017Franz FulhamNo ratings yet

- BinalonanWD-R1 ES2018Document4 pagesBinalonanWD-R1 ES2018J JaNo ratings yet

- Esperanza Executive Summary 2018Document5 pagesEsperanza Executive Summary 2018Ma. Danice Angela Balde-BarcomaNo ratings yet

- TaclobanCity2017 Audit Report PDFDocument170 pagesTaclobanCity2017 Audit Report PDFJulPadayaoNo ratings yet

- 03-Casiguran Aurora09 Executive SummaryDocument4 pages03-Casiguran Aurora09 Executive SummaryKasiguruhan AuroraNo ratings yet

- OdionganDocument7 pagesOdionganJohn Claude TabanNo ratings yet

- Luna Executive Summary 2012Document4 pagesLuna Executive Summary 2012The ApprenticeNo ratings yet

- Executive Summary: A. Highlights of Financial OperationDocument10 pagesExecutive Summary: A. Highlights of Financial OperationGloria AlamilNo ratings yet

- 01-LBP2016 Transmittal LettersDocument6 pages01-LBP2016 Transmittal LettersADRIAN 18No ratings yet

- Ormoc City 2018 Executive Summary and Audit ReportDocument6 pagesOrmoc City 2018 Executive Summary and Audit Reportsandra bolokNo ratings yet

- Maigo Executive Summary 2021Document8 pagesMaigo Executive Summary 2021Rowena MahusayNo ratings yet

- Alicia Executive Summary 2014Document6 pagesAlicia Executive Summary 2014Gier Rizaldo BulaclacNo ratings yet

- Municipality of Concepcion Financial Report and Audit SummaryDocument9 pagesMunicipality of Concepcion Financial Report and Audit SummaryJames SusukiNo ratings yet

- Executive Summary Highlights of Financial OperationsDocument4 pagesExecutive Summary Highlights of Financial OperationsSteve RodriguezNo ratings yet

- Villaba Executive Summary 2021Document5 pagesVillaba Executive Summary 2021Johanna Mae AutidaNo ratings yet

- Kalayaan Executive Summary 2014Document6 pagesKalayaan Executive Summary 2014Aira Kathrina PerezNo ratings yet

- 01-Angadanan2020 Transmittal LettersDocument14 pages01-Angadanan2020 Transmittal LettersAlicia NhsNo ratings yet

- Conner Executive Summary 2013Document5 pagesConner Executive Summary 2013Drei GoNo ratings yet

- Sipocot Executive Summary 2012Document6 pagesSipocot Executive Summary 2012Tintin N. XiaoNo ratings yet

- Cordon Isabela ES2018Document5 pagesCordon Isabela ES2018MelvinBuyagawonNo ratings yet

- Tanauan City Executive Summary 2021Document13 pagesTanauan City Executive Summary 2021Hannah Isabel ContiNo ratings yet

- La-Paz-Executive-Summary-2019Document10 pagesLa-Paz-Executive-Summary-2019Rene BalloNo ratings yet

- Moalboal Executive Summary 2018Document5 pagesMoalboal Executive Summary 2018Reyna YlenaNo ratings yet

- La Paz Executive Summary 2021Document5 pagesLa Paz Executive Summary 2021kmarkcramosNo ratings yet

- San Antonio Executive Summary 2019Document6 pagesSan Antonio Executive Summary 2019Jay AnnNo ratings yet

- Bislig City Executive Summary 2017Document8 pagesBislig City Executive Summary 2017liezeloragaNo ratings yet

- San Fernando Municipality Audit Report SummaryDocument3 pagesSan Fernando Municipality Audit Report SummaryJ JaNo ratings yet

- Quezon Executive Summary 2021 PDFDocument4 pagesQuezon Executive Summary 2021 PDFEsnar de Castro Jr.No ratings yet

- Executive SummaryDocument9 pagesExecutive SummaryGier Rizaldo BulaclacNo ratings yet

- Malabang Executive Summary 2018Document5 pagesMalabang Executive Summary 2018Evan LoirtNo ratings yet

- SurigaoDelNorte ES2010Document5 pagesSurigaoDelNorte ES2010J JaNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- Guimbal Executive Summary 2013Document5 pagesGuimbal Executive Summary 2013Jan M.No ratings yet

- Conner Executive Summary 2019Document8 pagesConner Executive Summary 2019The ApprenticeNo ratings yet

- San Pablo City Executive Summary 2013Document11 pagesSan Pablo City Executive Summary 2013Asteraceae ChrysanthNo ratings yet

- Siquijor Executive Summary 2018Document6 pagesSiquijor Executive Summary 2018roimar peraltaNo ratings yet

- Surallah-Executive-Summary-2020Document5 pagesSurallah-Executive-Summary-2020Kynard PatrickNo ratings yet

- Moalboal Executive Summary 2014Document6 pagesMoalboal Executive Summary 2014Horace CimafrancaNo ratings yet

- Bamban Executive Summary 2017Document6 pagesBamban Executive Summary 2017Reyna YlenaNo ratings yet

- Buenavista Executive Summary 2015Document9 pagesBuenavista Executive Summary 2015Virgo Philip Wasil ButconNo ratings yet

- Sablayan Executive Summary 2016Document5 pagesSablayan Executive Summary 2016Leo M. SalibioNo ratings yet

- Fxloan PrimerDocument2 pagesFxloan PrimerHenry AunzoNo ratings yet

- Appendix 67 RAAFDocument2 pagesAppendix 67 RAAFHenry AunzoNo ratings yet

- GL As of Aug 31, 2022 (Regular Agency Fund)Document118 pagesGL As of Aug 31, 2022 (Regular Agency Fund)Henry AunzoNo ratings yet

- Las Nieves Executive Summary 2015Document7 pagesLas Nieves Executive Summary 2015Henry AunzoNo ratings yet

- AMLADocument58 pagesAMLAGlaiza GiganteNo ratings yet

- Prohibiting Use of Gov Vehicles for Non-Official PurposesDocument5 pagesProhibiting Use of Gov Vehicles for Non-Official PurposesHenry AunzoNo ratings yet

- Liilippines: Oak R Erlf 'Document4 pagesLiilippines: Oak R Erlf 'Henry AunzoNo ratings yet

- Shareholders' Equity: PROBLEM 1: Prepare Journal Entries To Record Each of The FollowingDocument14 pagesShareholders' Equity: PROBLEM 1: Prepare Journal Entries To Record Each of The FollowingAccounting LayfNo ratings yet

- RECENT AMENDMENTS TO COMPANIES ACT 2013Document39 pagesRECENT AMENDMENTS TO COMPANIES ACT 2013warner313No ratings yet

- Intermediate Accounting 1 - InventoriesDocument9 pagesIntermediate Accounting 1 - InventoriesLien LaurethNo ratings yet

- Sample Problems On AnnuityDocument3 pagesSample Problems On Annuityboj VillanuevaNo ratings yet

- IRDA Project - Akanksha - LLMDocument9 pagesIRDA Project - Akanksha - LLMPULKIT KHANDELWALNo ratings yet

- ECON8Document3 pagesECON8DayLe Ferrer AbapoNo ratings yet

- Capital StructureDocument73 pagesCapital Structuresourav kumar dasNo ratings yet

- Trial Balance Ud Mudah HasilDocument1 pageTrial Balance Ud Mudah HasilSani SausanNo ratings yet

- Q1 PRE TechnoScanDocument2 pagesQ1 PRE TechnoScanmuhammad al aminNo ratings yet

- Entrepreneurship Challenges & Way ForwardDocument17 pagesEntrepreneurship Challenges & Way ForwardDr Pranjal Kumar PhukanNo ratings yet

- Ca Rohit Chola: ProfileDocument2 pagesCa Rohit Chola: ProfileThe Cultural CommitteeNo ratings yet

- Balance Sheet: Telenor Group As of 31 December 2008-09Document14 pagesBalance Sheet: Telenor Group As of 31 December 2008-09born2win_sattiNo ratings yet

- Fire InsuranceDocument3 pagesFire InsuranceAwasthi BrajendraNo ratings yet

- Withholding Tax Remittance Return: Kawanihan NG Rentas InternasDocument4 pagesWithholding Tax Remittance Return: Kawanihan NG Rentas InternasMHILET BasanNo ratings yet

- Analysis of The BankingDocument3 pagesAnalysis of The Bankingarnav singhNo ratings yet

- TATA MOTORS Profit and Loss SheetDocument1 pageTATA MOTORS Profit and Loss SheetKaushal RautNo ratings yet

- Project Finance: - Project Should Be Technically Feasible. - Project Should Be Economically ViableDocument18 pagesProject Finance: - Project Should Be Technically Feasible. - Project Should Be Economically ViableLaviNo ratings yet

- Swaps: Options, Futures, and Other John C. Hull 2008Document34 pagesSwaps: Options, Futures, and Other John C. Hull 2008KiranNo ratings yet

- PRTC 1stPB - 05.22 Sol FARDocument7 pagesPRTC 1stPB - 05.22 Sol FARCiatto SpotifyNo ratings yet

- Policybazaar: Indian Institute of Management RaipurDocument7 pagesPolicybazaar: Indian Institute of Management RaipurKaran SardaNo ratings yet

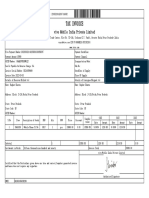

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- Salvatore Study-Guide Ch21Document8 pagesSalvatore Study-Guide Ch21jesNo ratings yet

- Wealth Management Asia: ParsimonyDocument3 pagesWealth Management Asia: ParsimonyJohn RockefellerNo ratings yet

- PERCENTAGEDocument7 pagesPERCENTAGEPrakash KumarNo ratings yet

- Global Recession and RecoveryDocument54 pagesGlobal Recession and RecoveryPaven RajNo ratings yet