You might also like

- AC 2202 CHAPTER 17 NotesDocument8 pagesAC 2202 CHAPTER 17 NotesKemuel TantuanNo ratings yet

- Accounting for Employee BenefitsDocument6 pagesAccounting for Employee BenefitsHannah Jane Arevalo LafuenteNo ratings yet

- PAS 19 Employee BenefitsDocument62 pagesPAS 19 Employee BenefitsBenj FloresNo ratings yet

- Employee Benefit - 181121Document26 pagesEmployee Benefit - 181121KhansaFatinNo ratings yet

- IAS 19 Employee BenefitDocument20 pagesIAS 19 Employee BenefitAklilNo ratings yet

- Employee Benefits Part 1.1Document5 pagesEmployee Benefits Part 1.1Shanelle SilmaroNo ratings yet

- Employee Benefits Under PAS 19, IAS 19 and RA 7641Document18 pagesEmployee Benefits Under PAS 19, IAS 19 and RA 7641alabwalaNo ratings yet

- IAS 19-Employee BenefitsDocument46 pagesIAS 19-Employee Benefitsmdhuzzal100% (3)

- Ind AS On Employee BenefitDocument81 pagesInd AS On Employee BenefitSanjay GohilNo ratings yet

- Employee Benefits: - CA. (DR.) Anand BankaDocument32 pagesEmployee Benefits: - CA. (DR.) Anand BankaNEHA NAYAKNo ratings yet

- IAS 19 Employee Benefits OverviewDocument8 pagesIAS 19 Employee Benefits OverviewAANo ratings yet

- Employees Benefit PalnDocument60 pagesEmployees Benefit PalnHimanshu GaurNo ratings yet

- Accounting-for-Employee-benefitsDocument35 pagesAccounting-for-Employee-benefitsOnwuchekwa Chidi CalebNo ratings yet

- Employee Benefit 2020Document18 pagesEmployee Benefit 2020harman singhNo ratings yet

- 1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Document13 pages1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Kimberly IgnacioNo ratings yet

- Handout 3.0 ACC 226 Sample Problems Employee BenefitsDocument12 pagesHandout 3.0 ACC 226 Sample Problems Employee BenefitsLyncee BallescasNo ratings yet

- Lecture # 11: Employee Benefits IAS-19Document3 pagesLecture # 11: Employee Benefits IAS-19ali hassnainNo ratings yet

- Employee Benefits P201Document17 pagesEmployee Benefits P201krisha milloNo ratings yet

- Acc 203 FinalsDocument10 pagesAcc 203 Finalspchu4019No ratings yet

- Employee Benefits P201Document18 pagesEmployee Benefits P201krisha milloNo ratings yet

- Ifrs at A Glance IAS 19 Employee BenefitsDocument5 pagesIfrs at A Glance IAS 19 Employee BenefitsnanaNo ratings yet

- Employee BenefitsDocument3 pagesEmployee BenefitsZance JordaanNo ratings yet

- Ias 19 Employee BeneftDocument24 pagesIas 19 Employee Beneftesulawyer2001No ratings yet

- Pas 19Document2 pagesPas 19MMBRIMBAPNo ratings yet

- Salary and Its TaxationDocument12 pagesSalary and Its TaxationBasit BandayNo ratings yet

- IAS 19 Employee BenefitsDocument14 pagesIAS 19 Employee BenefitsShiza ArifNo ratings yet

- Finacc ReviewerDocument4 pagesFinacc Reviewer200617No ratings yet

- Chapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletDocument1 pageChapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletcathNo ratings yet

- EmployeebenefitsreportDocument172 pagesEmployeebenefitsreportMikaela LacabaNo ratings yet

- 74702bos60485 Inter p1 cp6 U1Document27 pages74702bos60485 Inter p1 cp6 U1Saroj dasNo ratings yet

- FEU Institute Employee Benefits NotesDocument8 pagesFEU Institute Employee Benefits NotesAj PotXzs ÜNo ratings yet

- Annexure 3 Compensation FeeDocument3 pagesAnnexure 3 Compensation Feewanjariabhi6235No ratings yet

- Employee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Document10 pagesEmployee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Mica DelaCruzNo ratings yet

- Introduction To Compensation & Reward Management: Dr. Sumita MishraDocument38 pagesIntroduction To Compensation & Reward Management: Dr. Sumita MishraSarthak MohantyNo ratings yet

- IAS 19-EMPLOYEE BENEFITSDocument3 pagesIAS 19-EMPLOYEE BENEFITSfrondagericaNo ratings yet

- For Session DTD 5th Sep by CA Alok Garg PDFDocument46 pagesFor Session DTD 5th Sep by CA Alok Garg PDFLakshmi Narayana Murthy KapavarapuNo ratings yet

- Employee Benefits Related Standards: Pas 19 - Employee Benefits Pas 26 - Accounting & Reporting by Retirement Benefit PlansDocument10 pagesEmployee Benefits Related Standards: Pas 19 - Employee Benefits Pas 26 - Accounting & Reporting by Retirement Benefit PlansallyssajabsNo ratings yet

- Employee Benefit (Ias 19) FinalDocument36 pagesEmployee Benefit (Ias 19) FinalKanbiro OrkaidoNo ratings yet

- Forms of Compensation IncomeDocument6 pagesForms of Compensation IncomeMariaHannahKristenRamirezNo ratings yet

- Chapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsDocument50 pagesChapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsLovely AbadianoNo ratings yet

- PDF 15aug23 0724 SplittedDocument1 pagePDF 15aug23 0724 SplittedAshish ChaudharyNo ratings yet

- Notes IAS 19Document18 pagesNotes IAS 19Nasir IqbalNo ratings yet

- Candidate 1Document2 pagesCandidate 1Fascino WhiteNo ratings yet

- Defined Benefit Plans ExplainedDocument4 pagesDefined Benefit Plans ExplainedJames ScoldNo ratings yet

- Aec64 Audit 2 Notes-19-21Document3 pagesAec64 Audit 2 Notes-19-21Althea RubinNo ratings yet

- FAR23 Employee Benefits - With AnsDocument13 pagesFAR23 Employee Benefits - With AnsAJ Cresmundo100% (1)

- Notes On Employee BenefitsDocument26 pagesNotes On Employee BenefitsSarannyaRajendraNo ratings yet

- Accounting For Employee BenefitsDocument29 pagesAccounting For Employee BenefitsnuggsNo ratings yet

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- IAS-19 at Glance (BDO)Document4 pagesIAS-19 at Glance (BDO)FaraisNo ratings yet

- Employee Benefits Guide to Ind-AS 19Document42 pagesEmployee Benefits Guide to Ind-AS 19amarNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- Chapter Summary Chapter 5Document10 pagesChapter Summary Chapter 5ellyzamae quiraoNo ratings yet

- Ia 3Document3 pagesIa 3Auguste Anthony SisperezNo ratings yet

- IAS 19 Employee Benefits GuideDocument9 pagesIAS 19 Employee Benefits GuideRichie BoomaNo ratings yet

- CFAS NotesDocument27 pagesCFAS NotesMikasa AckermanNo ratings yet

- Pas 19 - Employee BenefitsDocument25 pagesPas 19 - Employee BenefitsBritnys NimNo ratings yet

- Employee BenefitsDocument18 pagesEmployee BenefitsLavillaNo ratings yet

- Employee Benefits: September 21, 2020Document18 pagesEmployee Benefits: September 21, 2020Andrea BaldonadoNo ratings yet

- Taxation Laws ExplainedDocument7 pagesTaxation Laws ExplainedKemuel TantuanNo ratings yet

- AC 2101 CHAPTER 26 NotesDocument5 pagesAC 2101 CHAPTER 26 NotesKemuel TantuanNo ratings yet

- PPE Chapter 23Document4 pagesPPE Chapter 23Kemuel TantuanNo ratings yet

- Consignment Sales AccountingDocument2 pagesConsignment Sales AccountingKemuel TantuanNo ratings yet

- AC 3101 CHAPTER 10 NotesDocument2 pagesAC 3101 CHAPTER 10 NotesKemuel TantuanNo ratings yet

- Taxsheet 10007162Document2 pagesTaxsheet 10007162Narender KapoorNo ratings yet

- PP Rozdział - 4 - MiniMatura - Grupa - ADocument2 pagesPP Rozdział - 4 - MiniMatura - Grupa - AAleksandra Myślińska50% (2)

- Suggested Answer On Tax Planning and Compliance Nov-Dec, 2023Document18 pagesSuggested Answer On Tax Planning and Compliance Nov-Dec, 2023Erfan KhanNo ratings yet

- Taxation LawDocument67 pagesTaxation LawAdv Sheetal SaylekarNo ratings yet

- Ferma ActDocument21 pagesFerma ActJessareth Atilano CapacioNo ratings yet

- Confirmation 1 PDFDocument2 pagesConfirmation 1 PDFENAD TBISHATNo ratings yet

- Taxation NotesDocument33 pagesTaxation NotesNaina AgarwalNo ratings yet

- Chapter 8Document2 pagesChapter 8Kate AllanigueNo ratings yet

- Taxation UK ACCA F6Document9 pagesTaxation UK ACCA F6Ankit DubeyNo ratings yet

- Narrative DescriptionDocument2 pagesNarrative DescriptionAnonymous N9dx4ATEghNo ratings yet

- Wealth Management ProjectDocument10 pagesWealth Management ProjectShirsendu DasNo ratings yet

- TESRDocument4 pagesTESRBakhtar FaiziNo ratings yet

- Declaration of Marital Status FormDocument2 pagesDeclaration of Marital Status FormAshrafNo ratings yet

- A Project Report On Taxation in IndiaDocument59 pagesA Project Report On Taxation in IndiaYash Bhagat100% (1)

- Frequently Asked Questions: Q. What Are The Common Exit Formalities After Resignation?Document12 pagesFrequently Asked Questions: Q. What Are The Common Exit Formalities After Resignation?anshumaan upadhyay100% (1)

- Chapter 8 Employee BenefitsDocument40 pagesChapter 8 Employee BenefitsjammuuuNo ratings yet

- ITR-4 Notified Form AY 2021-22-0Document5 pagesITR-4 Notified Form AY 2021-22-0Kuldeep JatNo ratings yet

- C.M. Hoskins & Co., Inc. vs. Commissioner of Internal RevenueDocument1 pageC.M. Hoskins & Co., Inc. vs. Commissioner of Internal RevenueAlljun SerenadoNo ratings yet

- Incomes Exempt Under Section 10Document10 pagesIncomes Exempt Under Section 10Rahul TiwariNo ratings yet

- Money Saving Strategies: Laura Connerly, PH.D., Assistant Professor - Family and Consumer EconomicsDocument5 pagesMoney Saving Strategies: Laura Connerly, PH.D., Assistant Professor - Family and Consumer EconomicsAhmedinNo ratings yet

- Understanding Tax ExemptionDocument1 pageUnderstanding Tax Exemptionirene ibonNo ratings yet

- Discussion - Accounting ProceduresDocument5 pagesDiscussion - Accounting ProceduresLove KarenNo ratings yet

- Kuenzle V CIRDocument10 pagesKuenzle V CIRRean Raphaelle GonzalesNo ratings yet

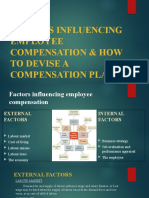

- Factors Influencing Employee Compensation & How To DeviseDocument9 pagesFactors Influencing Employee Compensation & How To DevisesangeethaNo ratings yet

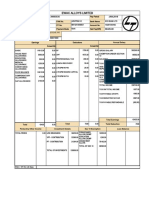

- Ewac Alloys Limited: Uan No Aadhar NoDocument1 pageEwac Alloys Limited: Uan No Aadhar NoNapoleon DasNo ratings yet

- Income Tax Under Canadian RegulationsDocument10 pagesIncome Tax Under Canadian Regulationshemayal0% (1)

- Income Taxation Chapter on Compensation IncomeDocument17 pagesIncome Taxation Chapter on Compensation IncomeSheilamae Sernadilla GregorioNo ratings yet

- SBF Iocl 19.11.12Document18 pagesSBF Iocl 19.11.12ParameshNo ratings yet

- Regular Income Taxation: Inclusion in Gross Income: Chan, John Mark Juganas, Hazel Madayag, Jovie AnnDocument43 pagesRegular Income Taxation: Inclusion in Gross Income: Chan, John Mark Juganas, Hazel Madayag, Jovie AnnAngelica PagaduanNo ratings yet

- FM's External Factors and Competition in ArboriaDocument3 pagesFM's External Factors and Competition in ArboriaWelldy WldNo ratings yet