You might also like

- Macroeconomics For Financial MarketDocument88 pagesMacroeconomics For Financial MarketNeeraj Kumar67% (3)

- Aliran Tunai Untuk 50,000 Ekor AyamDocument1 pageAliran Tunai Untuk 50,000 Ekor AyamMaharaja LelaNo ratings yet

- Chetan Jain - Legal NoticeDocument4 pagesChetan Jain - Legal NoticePrassad BataviaNo ratings yet

- MBS Corporate Finance 2023 Slide Set 3Document104 pagesMBS Corporate Finance 2023 Slide Set 3PGNo ratings yet

- The Indian Payments Handbook 2021 2026Document34 pagesThe Indian Payments Handbook 2021 2026scienceplexNo ratings yet

- Performance Report: Cat 6050 FS and 6060 FS at La Herradura Gold Mine (Sonora, Mexico)Document24 pagesPerformance Report: Cat 6050 FS and 6060 FS at La Herradura Gold Mine (Sonora, Mexico)EVCY100% (1)

- Activity-Based Cost Systems: The Classic Pen Company A Case AnalysisDocument14 pagesActivity-Based Cost Systems: The Classic Pen Company A Case AnalysisSarveshwar Sharma50% (2)

- This Budget Is Interactive: INPUT DATA: Your Values in The Unprotected or Highlighted CellsDocument15 pagesThis Budget Is Interactive: INPUT DATA: Your Values in The Unprotected or Highlighted CellsGeros dienosNo ratings yet

- Mojakoe: Modul Jawaban KoeliahDocument17 pagesMojakoe: Modul Jawaban KoeliahGhithrifNo ratings yet

- AC2105 Seminar 3 Group 3Document37 pagesAC2105 Seminar 3 Group 3Kwang Yi JuinNo ratings yet

- TUT 3 - Relevant Information&decision MakingDocument10 pagesTUT 3 - Relevant Information&decision MakingKim Chi LeNo ratings yet

- This Budget Is InteractiveDocument24 pagesThis Budget Is InteractiveGeros dienosNo ratings yet

- Classic Pen HandoutsDocument1 pageClassic Pen HandoutsSuraj KumarNo ratings yet

- MVV - Assignment 1 - ManyaDocument14 pagesMVV - Assignment 1 - ManyaManya SrivastavaNo ratings yet

- Sample ComputationDocument13 pagesSample ComputationKathleen AngidNo ratings yet

- ClassicPenCompany 2023B2PGPMX012 KshitijDocument3 pagesClassicPenCompany 2023B2PGPMX012 KshitijSuraj KumarNo ratings yet

- Classic Pen Co HandoutDocument1 pageClassic Pen Co HandoutbharathtgNo ratings yet

- Review Session 2024 SolutionsDocument3 pagesReview Session 2024 SolutionsHitesh MehtaNo ratings yet

- This Budget Is Interactive: INPUT DATA: Your Values in The Unprotected or Highlighted CellsDocument31 pagesThis Budget Is Interactive: INPUT DATA: Your Values in The Unprotected or Highlighted CellsGeros dienosNo ratings yet

- Discount Rate 7Document1 pageDiscount Rate 7CliefSengkeyNo ratings yet

- Wrapitup 54% 102% 44%: Case Exhibit 1 Restaurant Industry Turnover Rates 2006 2008Document14 pagesWrapitup 54% 102% 44%: Case Exhibit 1 Restaurant Industry Turnover Rates 2006 2008Melvin ShajiNo ratings yet

- Group 14 Disha Gupta (PGP36358) Godavarthi Srikanth (PGP36363) Priy Ranjan Kumar (PGP36378) Udhav Khanna (PGP36399)Document10 pagesGroup 14 Disha Gupta (PGP36358) Godavarthi Srikanth (PGP36363) Priy Ranjan Kumar (PGP36378) Udhav Khanna (PGP36399)PRIY RANJAN KUMARNo ratings yet

- 2020 - Onion BudgetDocument13 pages2020 - Onion BudgetGeros dienosNo ratings yet

- Ch.4 Book Exercise + AnswerDocument7 pagesCh.4 Book Exercise + Answertomsuen63No ratings yet

- Managerial AnalysisDocument5 pagesManagerial AnalysisIsaac OmwengaNo ratings yet

- Classic Pen Working HandoutsDocument1 pageClassic Pen Working HandoutsTushar DuaNo ratings yet

- CBA SampleDocument9 pagesCBA Samplemonderoclyde24No ratings yet

- Cases On Activity Based Costing SystemDocument6 pagesCases On Activity Based Costing SystemEnusah PeterNo ratings yet

- Measuring and Managing Process Performance: QuestionsDocument4 pagesMeasuring and Managing Process Performance: QuestionsAshik Uz ZamanNo ratings yet

- Measuring and Managing Process Performance: QuestionsDocument4 pagesMeasuring and Managing Process Performance: QuestionsAshik Uz ZamanNo ratings yet

- Cost Per Test BC 3600 DPLDocument2 pagesCost Per Test BC 3600 DPLRifky AdytianNo ratings yet

- Managerial Accounting Final Presentation: Seligram, Inc.: Electronic Testing OperationsDocument12 pagesManagerial Accounting Final Presentation: Seligram, Inc.: Electronic Testing OperationsJuragan BiasaNo ratings yet

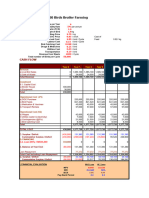

- Description (1) Amount (2) Percentage of Total COQ (3) (2) ÷ $1,820,000 Percentage of Revenues (4) (2) ÷ $45,000,000Document3 pagesDescription (1) Amount (2) Percentage of Total COQ (3) (2) ÷ $1,820,000 Percentage of Revenues (4) (2) ÷ $45,000,000Elliot RichardNo ratings yet

- Group 5Document16 pagesGroup 5Amelia AndrianiNo ratings yet

- FAMA '22 SolutionDocument4 pagesFAMA '22 SolutionRushil JoshiNo ratings yet

- Chapter 5Document9 pagesChapter 5Dishantely SamboNo ratings yet

- Management AccountingDocument11 pagesManagement Accountingsongoro072889No ratings yet

- 2020-Cabbage BudgetDocument15 pages2020-Cabbage BudgetGeros dienosNo ratings yet

- Particulars Current Post Repositioning (Scenario 1) Post Repositioning (Scenario 2) Per Unit Total Per Unit Total Per Unit RevenuesDocument4 pagesParticulars Current Post Repositioning (Scenario 1) Post Repositioning (Scenario 2) Per Unit Total Per Unit Total Per Unit RevenuesALLtyNo ratings yet

- Performance Drinks Case 2 QureshiDocument9 pagesPerformance Drinks Case 2 QureshiRabia Qureshi100% (2)

- Cop Beef FeedlotfinishingDocument18 pagesCop Beef Feedlotfinishinganthonius70No ratings yet

- Chicken PriceDocument1 pageChicken PriceLin DanNo ratings yet

- KEDGE BS-IBB4 - Management Control & Operations: The French Cost Accounting Method CorrectionDocument2 pagesKEDGE BS-IBB4 - Management Control & Operations: The French Cost Accounting Method CorrectionArnaud DelacourNo ratings yet

- CH 7 Support Department Cost AllocationDocument45 pagesCH 7 Support Department Cost Allocationsalsa azzahraNo ratings yet

- Cost Accou5Document1 pageCost Accou5suuNo ratings yet

- Geronimo e - Assignment 1Document2 pagesGeronimo e - Assignment 1Geronimo EnguitoNo ratings yet

- CVP Analysis SolutionsDocument6 pagesCVP Analysis SolutionsAlaine Milka GosycoNo ratings yet

- Financial FatteningDocument17 pagesFinancial FatteningEskinder KebedeNo ratings yet

- City Buildings Business PowerPoint TemplateDocument15 pagesCity Buildings Business PowerPoint TemplateSalman SajidNo ratings yet

- RMC-LUCBAN MAAM SANDY-3000PSI @28 Days G1Document1 pageRMC-LUCBAN MAAM SANDY-3000PSI @28 Days G1Eljoy C. AgsamosamNo ratings yet

- CH SolutionsDocument6 pagesCH SolutionsPink MagentaNo ratings yet

- Chapter 5 - Relevant Information and Decision MakingDocument56 pagesChapter 5 - Relevant Information and Decision Making040404.anniNo ratings yet

- Chapter 01Document45 pagesChapter 01Adam AbdullahiNo ratings yet

- AMUL Case Study in Context of Financial Management, Cost and Management Accounting, Production & Operation ManagementDocument26 pagesAMUL Case Study in Context of Financial Management, Cost and Management Accounting, Production & Operation ManagementtwinkalNo ratings yet

- GroupNo 4Document6 pagesGroupNo 4aakash9117No ratings yet

- Responsibility AccountingDocument21 pagesResponsibility AccountingMicaella GrandeNo ratings yet

- Jawaban Akhir AML 2022Document6 pagesJawaban Akhir AML 2022Reviandi RamadhanNo ratings yet

- Total Cost To Be Allocated To The Deposit and Loan Departments $ 1,147,500Document15 pagesTotal Cost To Be Allocated To The Deposit and Loan Departments $ 1,147,500Gillu BilluNo ratings yet

- Chapter 12 PDFDocument11 pagesChapter 12 PDFgerNo ratings yet

- D4 - 2a - Amp - Minggu6 - 205134024 - Putty Humaira NurgiaDocument6 pagesD4 - 2a - Amp - Minggu6 - 205134024 - Putty Humaira NurgiaNur LaelahNo ratings yet

- Book Ak Bi P-11 Contoh Soal Joint Cost Physical Method + JawabanDocument2 pagesBook Ak Bi P-11 Contoh Soal Joint Cost Physical Method + JawabanRynaldo xf100% (1)

- Tugas Akuntansi Manajemen Lanjutan PROBLEM 4.32 Dan 4.35: Teuku Aldefa Angkasa Wangsa Banowo 2006623132Document3 pagesTugas Akuntansi Manajemen Lanjutan PROBLEM 4.32 Dan 4.35: Teuku Aldefa Angkasa Wangsa Banowo 2006623132Teuku AldefaNo ratings yet

- ACCOUNTING FOR LABOR AND OH LectureDocument13 pagesACCOUNTING FOR LABOR AND OH LectureNah HamzaNo ratings yet

- Tutorial 5 NotesDocument2 pagesTutorial 5 NotesNikki MathysNo ratings yet

- Tutorial 2 NotesDocument3 pagesTutorial 2 NotesNikki MathysNo ratings yet

- Tutorial 3 NotesDocument3 pagesTutorial 3 NotesNikki MathysNo ratings yet

- Tutorial 4 NotesDocument2 pagesTutorial 4 NotesNikki MathysNo ratings yet

- Week 2 - Lecture 3Document5 pagesWeek 2 - Lecture 3Nikki MathysNo ratings yet

- Tutorial HomeworkDocument7 pagesTutorial HomeworkNikki MathysNo ratings yet

- Tutorial Homework 2Document4 pagesTutorial Homework 2Nikki MathysNo ratings yet

- Practice For Accounting TestDocument5 pagesPractice For Accounting TestNikki MathysNo ratings yet

- ABC Example 1Document4 pagesABC Example 1Nikki MathysNo ratings yet

- ACCTN101 Cheat SheetDocument8 pagesACCTN101 Cheat SheetNikki MathysNo ratings yet

- Test Question AnswerDocument4 pagesTest Question AnswerNikki MathysNo ratings yet

- Lecture 2 - Measurement of Business Transactions & GSTDocument9 pagesLecture 2 - Measurement of Business Transactions & GSTNikki MathysNo ratings yet

- Lecture 1 - Concepts and EthicsDocument10 pagesLecture 1 - Concepts and EthicsNikki MathysNo ratings yet

- Sun - MORNING NEWS DAILY, Dec 2020, SV PDFDocument6 pagesSun - MORNING NEWS DAILY, Dec 2020, SV PDFSHARON TVNo ratings yet

- Delil Thesis Paper FinalDocument88 pagesDelil Thesis Paper FinalSingitan YomiyuNo ratings yet

- File 5Document436 pagesFile 5Irshad mohammedNo ratings yet

- Strategic Alliance FinalDocument10 pagesStrategic Alliance FinalVarun TejaNo ratings yet

- Vitasek, K. 2016 Strategic Sourcing Business ModelsDocument18 pagesVitasek, K. 2016 Strategic Sourcing Business ModelsKevin Velásquez SalazarNo ratings yet

- Linear Programming FormulationDocument27 pagesLinear Programming FormulationDrama ArtNo ratings yet

- Automatic Gearbox 0B6 Four-Wheel DriveDocument185 pagesAutomatic Gearbox 0B6 Four-Wheel DriveergdegNo ratings yet

- University of The Immaculate Conception: Master in Business Administration ProgramDocument21 pagesUniversity of The Immaculate Conception: Master in Business Administration ProgramCINDY MAE DUMAPIASNo ratings yet

- WMM Plant CalibrationDocument13 pagesWMM Plant CalibrationDeepakNo ratings yet

- Partlist SLC480Document19 pagesPartlist SLC480Alessandro MalocciNo ratings yet

- Lecture Notes C3Document12 pagesLecture Notes C3Levent ŞaşmazNo ratings yet

- Company BackgroundDocument8 pagesCompany BackgroundAbdullah Ahmad AfhammuddinNo ratings yet

- Slide Tax Incentives For Green Technology Industry 27 Feb 2018Document30 pagesSlide Tax Incentives For Green Technology Industry 27 Feb 2018rexNo ratings yet

- Paragraf Siklus BisnisDocument2 pagesParagraf Siklus BisnisMaryaNo ratings yet

- Solution and AnswerDocument4 pagesSolution and AnswerMicaela EncinasNo ratings yet

- Kuru Dec2019Document52 pagesKuru Dec2019Rafi S ANo ratings yet

- Principles of Microeconomics (PMI511S) : Lecturer: Mr. Mally LikukelaDocument10 pagesPrinciples of Microeconomics (PMI511S) : Lecturer: Mr. Mally LikukelaRax-Nguajandja KapuireNo ratings yet

- Privatization and Deregulation in Ethiopia - Final - Docx1Document33 pagesPrivatization and Deregulation in Ethiopia - Final - Docx1kassahun meseleNo ratings yet

- Upstream Petroleum Activities - April 2021: Inset NorthDocument1 pageUpstream Petroleum Activities - April 2021: Inset NorthumairahmedbaigNo ratings yet

- Unit One Process CostingDocument9 pagesUnit One Process CostingDzukanji SimfukweNo ratings yet

- Orders ListDocument59 pagesOrders Listsivasaidatta.kotikalapudiNo ratings yet

- Ge - CH 1Document25 pagesGe - CH 1Nur SyafawaniNo ratings yet

- Capitalism Will Eat Democracy - Unless We Speak UpDocument10 pagesCapitalism Will Eat Democracy - Unless We Speak UpNot Charlie GriffithNo ratings yet

- Group Assignment 2014Document3 pagesGroup Assignment 2014Samuel AberaNo ratings yet

- Point: Cryptocurrencies in KenyaDocument7 pagesPoint: Cryptocurrencies in KenyaMETANOIANo ratings yet