You might also like

- Analysis of cash flows and profitability ratios for ABC CompanyDocument5 pagesAnalysis of cash flows and profitability ratios for ABC Companynikhil hoodaNo ratings yet

- Analyzing cash flow trends and profitability ratios of Ceres companyDocument7 pagesAnalyzing cash flow trends and profitability ratios of Ceres companyShilpi Gautam100% (1)

- Year 2003 2004 2005 2006E Operating Cash Flow 2,019 838 250 226Document6 pagesYear 2003 2004 2005 2006E Operating Cash Flow 2,019 838 250 226Budhaditya basuNo ratings yet

- IMT CeresDocument5 pagesIMT CeresKAJAL SHARMANo ratings yet

- Name Annapoorneshwari .S. UDocument4 pagesName Annapoorneshwari .S. Uannapoorneshwari suNo ratings yet

- Ceres Gardening Company Submission TemplateDocument5 pagesCeres Gardening Company Submission TemplateVishalNo ratings yet

- Ceres Gardening Company - Spreadsheet For StudentsDocument1 pageCeres Gardening Company - Spreadsheet For Studentsandres felipe restrepo arango0% (1)

- Imt CeresDocument10 pagesImt CeresProshanjit DeyNo ratings yet

- Write Your Answer For Part A HereDocument9 pagesWrite Your Answer For Part A HereMATHEW JACOBNo ratings yet

- Write Your Answer For Part A HereDocument8 pagesWrite Your Answer For Part A Heresuraj dhruvNo ratings yet

- Ceres Gardening Company Submission PDFDocument7 pagesCeres Gardening Company Submission PDFnikki tamboli81% (16)

- Cash Flow Analysis Love VermaDocument8 pagesCash Flow Analysis Love Vermalove vermaNo ratings yet

- IMT CeresDocument9 pagesIMT CeresDEEKSHA DNo ratings yet

- IMT CeresDocument5 pagesIMT Ceresrithvik royNo ratings yet

- Analyzing Cash Flow Trends and Profitability RatiosDocument7 pagesAnalyzing Cash Flow Trends and Profitability RatiosASISH SABATNo ratings yet

- IMT CeresDocument7 pagesIMT CeresRajat KumarNo ratings yet

- Name Neethu Nair: Write Your Answer For Part A HereDocument9 pagesName Neethu Nair: Write Your Answer For Part A HereNeethu Nair67% (3)

- IMT CeresDocument6 pagesIMT CeresPRANAYNo ratings yet

- Name Karandeep Singh: $226 (In Thousands)Document5 pagesName Karandeep Singh: $226 (In Thousands)Rishabh TiwariNo ratings yet

- Operating Working Capital (INV+AR-AP)Document33 pagesOperating Working Capital (INV+AR-AP)Neethu Nair40% (5)

- Name Suhail Abdul Rashid TankeDocument9 pagesName Suhail Abdul Rashid TankeIram ParkarNo ratings yet

- Operating Cash Flow AnalysisDocument5 pagesOperating Cash Flow AnalysisRahul PandeyNo ratings yet

- Name Email: Ganesh Bhushan Misra: A: Cash Flow From Operations Is The Section of A Company's Cash Flow Statement ThatDocument6 pagesName Email: Ganesh Bhushan Misra: A: Cash Flow From Operations Is The Section of A Company's Cash Flow Statement ThatGanesh Misra100% (1)

- Q&A-Business Communication (Optional Included)Document54 pagesQ&A-Business Communication (Optional Included)Madan G Koushik100% (2)

- Ceres Gardening Company Submission TemplateDocument2 pagesCeres Gardening Company Submission TemplateAnirban Bhattacharya0% (1)

- Q&a-Mcq (HR & Ob)Document124 pagesQ&a-Mcq (HR & Ob)Madan G Koushik100% (1)

- IMT LisaBenton Vikram ShermaleDocument6 pagesIMT LisaBenton Vikram Shermalevikram shermaleNo ratings yet

- Name Atikesh Gupta: Write Your Answer For Part A HereDocument7 pagesName Atikesh Gupta: Write Your Answer For Part A HereDeblina Mitra100% (2)

- OPSCM ProjectDocument7 pagesOPSCM ProjectRish JayNo ratings yet

- IMT LisaBenton Deblina MitraDocument5 pagesIMT LisaBenton Deblina MitraDeblina MitraNo ratings yet

- Question 1 (13 Marks) : Graded QuestionsDocument5 pagesQuestion 1 (13 Marks) : Graded QuestionsKamaljeet Singh Malhotra25% (4)

- IMT CastrolDocument8 pagesIMT CastrolJayanth Kn0% (1)

- Question 1 (13 Marks)Document4 pagesQuestion 1 (13 Marks)SUDHIR KAUSHIK20% (5)

- Consumer Decision Notes PDFDocument7 pagesConsumer Decision Notes PDFRish JayNo ratings yet

- Ceres Gardening Company Graded QuestionsDocument4 pagesCeres Gardening Company Graded QuestionsSai KumarNo ratings yet

- Regression Analysis Random MotorsDocument11 pagesRegression Analysis Random MotorsNivedita Nautiyal100% (1)

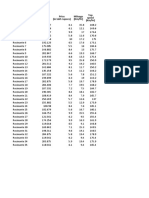

- Cars Sales (In 1,000 Units) Price (In Lakh Rupees) Mileage (KM/LTR) Top Speed (KM/HR)Document10 pagesCars Sales (In 1,000 Units) Price (In Lakh Rupees) Mileage (KM/LTR) Top Speed (KM/HR)Rishabh TiwariNo ratings yet

- OPSCMProject - Ashutosh SangleDocument7 pagesOPSCMProject - Ashutosh SangleRish Jay100% (2)

- Random Motors BriefingDocument43 pagesRandom Motors BriefingAndy KumarNo ratings yet

- Random Motors Presentation Ganesh MisraDocument10 pagesRandom Motors Presentation Ganesh MisraGanesh Misra100% (2)

- IMT Covid19Document6 pagesIMT Covid19Jayanth KnNo ratings yet

- OPSCM Project - Vimalakar - PolamarasettyDocument6 pagesOPSCM Project - Vimalakar - PolamarasettyvimalakarpolamarasettyNo ratings yet

- IMT Covid19Document10 pagesIMT Covid19Ganesh MisraNo ratings yet

- Ganesh Bhushan Misra: Write Your Answer HereDocument8 pagesGanesh Bhushan Misra: Write Your Answer HereGanesh Misra100% (1)

- Question 1 (A&B) : Respectfully, Mahesh Iyer Co Founder, SineflexDocument2 pagesQuestion 1 (A&B) : Respectfully, Mahesh Iyer Co Founder, SineflexRahul Dinesh60% (5)

- IMT LisaBentonDocument6 pagesIMT LisaBentonPRANAYNo ratings yet

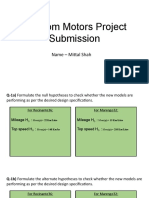

- Final Presentation by Mittal ShahDocument10 pagesFinal Presentation by Mittal ShahPradeep Nambiar100% (3)

- IMT Lisabenton TejeswiniDocument8 pagesIMT Lisabenton Tejeswinitejeswini albertNo ratings yet

- IMT Castrol SSDocument7 pagesIMT Castrol SSSandeep Surendran100% (1)

- Ceres+Gardening+Company+Submission Shradha PuroDocument6 pagesCeres+Gardening+Company+Submission Shradha PuroShradha PuroNo ratings yet

- OPSCM Project - Shahzar AhmedDocument7 pagesOPSCM Project - Shahzar AhmedShahzar AhmedNo ratings yet

- Random Motors Project Submission: Name - Avanish Pratap PauliDocument10 pagesRandom Motors Project Submission: Name - Avanish Pratap Pauliavanish pratap100% (1)

- Analyzing cash flows and profitability of Ceres Gardening CompanyDocument5 pagesAnalyzing cash flows and profitability of Ceres Gardening CompanyShubham MishraNo ratings yet

- Alap Kavishwar - Project - Submission - ChangeManagementDocument12 pagesAlap Kavishwar - Project - Submission - ChangeManagementA KNo ratings yet

- Ceres Gardening CalculationsDocument11 pagesCeres Gardening CalculationsOwaisKhan75% (4)

- IMT CeresDocument8 pagesIMT CeresDeepika Chandrashekar100% (1)

- IMT - LisaBenton - Rajeev RanjanDocument6 pagesIMT - LisaBenton - Rajeev RanjanRajeev RanjanNo ratings yet

- Tushar Wadhwa - Project Submission - Change ManagementDocument13 pagesTushar Wadhwa - Project Submission - Change ManagementTushar WadhwaNo ratings yet

- IMT - Ceres Case StudyDocument7 pagesIMT - Ceres Case Studynikitapansare208No ratings yet

- Ceres Gardening Company Submission TemplateDocument7 pagesCeres Gardening Company Submission Templatenikitapansare208No ratings yet

- Random Motors Project Submission: Name - Debasish PattanaikDocument10 pagesRandom Motors Project Submission: Name - Debasish PattanaikDebasish PattanaikNo ratings yet

- DigitalBusinessInnovation - Debasish PattanaikDocument6 pagesDigitalBusinessInnovation - Debasish PattanaikDebasish PattanaikNo ratings yet

- IMT LisaBentonDocument4 pagesIMT LisaBentonDebasish PattanaikNo ratings yet

- Lisa Benton Case IMT RegularDocument37 pagesLisa Benton Case IMT RegularDebasish PattanaikNo ratings yet

- Project EvaluationDocument23 pagesProject EvaluationDebasish PattanaikNo ratings yet

- Debasish Pattanaik - Project Submission - LeadershipDocument5 pagesDebasish Pattanaik - Project Submission - LeadershipDebasish PattanaikNo ratings yet

- VIRO AnalysisDocument1 pageVIRO AnalysisDebasish PattanaikNo ratings yet

- SimulationDocument8 pagesSimulationDebasish PattanaikNo ratings yet

- IMT EverestDocument2 pagesIMT EverestDebasish PattanaikNo ratings yet

- Discontinued OperationsDocument22 pagesDiscontinued OperationsJeff KinutsNo ratings yet

- Accounting assignments on amortization tables and financial instrumentsDocument5 pagesAccounting assignments on amortization tables and financial instrumentsGerald GiovanniNo ratings yet

- Sap S4Hana TRM: Treasury Management and Cash ManagementDocument41 pagesSap S4Hana TRM: Treasury Management and Cash ManagementNAMOOD-E-SAHAR KunwerNo ratings yet

- Fin Acc Exam CompilationDocument27 pagesFin Acc Exam CompilationRiza100% (1)

- PFR On Biodegradable Plastic BagsDocument35 pagesPFR On Biodegradable Plastic BagsArsh Adeeb Ghazi0% (1)

- Far JpiaDocument14 pagesFar JpiaJNo ratings yet

- 12Document24 pages12Maria G. BernardinoNo ratings yet

- Chapter 4 Business CombinationsDocument8 pagesChapter 4 Business CombinationsTilahun GirmaNo ratings yet

- AFM Chapter 2 Balance SheetDocument41 pagesAFM Chapter 2 Balance SheetSarah Shahnaz IlmaNo ratings yet

- Jam Althea O. Agner Prelec Output 1Document3 pagesJam Althea O. Agner Prelec Output 1JAM ALTHEA AGNERNo ratings yet

- Gen 010 Q1 Sy2223Document5 pagesGen 010 Q1 Sy2223CLAIRE PAJONo ratings yet

- JLL Real Estate As A Global Asset ClassDocument9 pagesJLL Real Estate As A Global Asset Classashraf187100% (1)

- Far410 Chapter 2 Conceptual Framework EditedDocument60 pagesFar410 Chapter 2 Conceptual Framework EditedWAN AMIRUL MUHAIMIN WAN ZUKAMALNo ratings yet

- Cash Flow Statement for K BarrettDocument4 pagesCash Flow Statement for K BarrettRajay BramwellNo ratings yet

- EAM OTL IntegrationDocument17 pagesEAM OTL Integrationsayantani janaNo ratings yet

- Review of Financial StatementsDocument8 pagesReview of Financial StatementsHaseeb AliNo ratings yet

- Service Schedule For Cakes A. in DaysDocument43 pagesService Schedule For Cakes A. in DaysPhilip Dan Jayson LarozaNo ratings yet

- ACCA2 1 Handout No. 1 - Conceptual Framework For Financial ReportingDocument3 pagesACCA2 1 Handout No. 1 - Conceptual Framework For Financial ReportingZia May LauretaNo ratings yet

- Inflation AccountingDocument13 pagesInflation AccountingtrinabhagatNo ratings yet

- Fabm Reviewer 1Document4 pagesFabm Reviewer 1Cameron VelascoNo ratings yet

- CFA Level 1Document90 pagesCFA Level 1imran0104100% (2)

- The Objective of Chapter 9 Is To Address The Question of Whether A Currently Owned Asset Should Be Kept in Service or Immediately ReplacedDocument24 pagesThe Objective of Chapter 9 Is To Address The Question of Whether A Currently Owned Asset Should Be Kept in Service or Immediately ReplacedAykut YıldızNo ratings yet

- 25 Profit-Performance Measurements & Intracompany Transfer PricingDocument13 pages25 Profit-Performance Measurements & Intracompany Transfer PricingLaurenz Simon ManaliliNo ratings yet

- Accounting For Single Entry and Incomplete RecordsDocument18 pagesAccounting For Single Entry and Incomplete RecordsCA Deepak Ehn77% (13)

- Practice Cases For Chapter 12 Case 1Document3 pagesPractice Cases For Chapter 12 Case 1Lê Minh TríNo ratings yet

- First Time Adoption of PFRSDocument5 pagesFirst Time Adoption of PFRSPia ArellanoNo ratings yet

- Unit 3: Indian Accounting Standard 113: Fair Value MeasurementDocument26 pagesUnit 3: Indian Accounting Standard 113: Fair Value MeasurementgauravNo ratings yet

- Mock CPA Board Examinations ReviewDocument8 pagesMock CPA Board Examinations ReviewLara Lewis Achilles100% (1)

- Case Solution - A New Financial Policy at Swedish Match - ANIDocument20 pagesCase Solution - A New Financial Policy at Swedish Match - ANIAnisha Goyal33% (3)