You might also like

- Design and Analysis of Algorithms ExamDocument2 pagesDesign and Analysis of Algorithms ExamA kayNo ratings yet

- Programming in Java: Instruction To CandidatesDocument2 pagesProgramming in Java: Instruction To CandidatesDas KumNo ratings yet

- Design of Machine Elements-I: Instructions To CandidatesDocument2 pagesDesign of Machine Elements-I: Instructions To CandidatesAnil KumarNo ratings yet

- Database Management System: Instruction To CandidatesDocument2 pagesDatabase Management System: Instruction To CandidateslovebanglaNo ratings yet

- QT (1st) Dec2018Document3 pagesQT (1st) Dec2018Cyril RaymondNo ratings yet

- Docu Date The Same Date in Doc CW Tower Exp gl-621001 Mention Text As A GPX in Front Move Entry ClearingDocument2 pagesDocu Date The Same Date in Doc CW Tower Exp gl-621001 Mention Text As A GPX in Front Move Entry Clearing20cab244 NavineshNo ratings yet

- ARB Eastern New Price List MAY 2012Document1 pageARB Eastern New Price List MAY 2012Amit KumarNo ratings yet

- CAD/CAM Exam QuestionsDocument2 pagesCAD/CAM Exam QuestionsAnjaiah MadarapuNo ratings yet

- Advertising Management: Instruction To CandidatesDocument2 pagesAdvertising Management: Instruction To CandidatesManjul VaidyaNo ratings yet

- Linux Operating System Exam QuestionsDocument2 pagesLinux Operating System Exam QuestionsNick JamesNo ratings yet

- Engineering Mathematics II Differential EquationsDocument3 pagesEngineering Mathematics II Differential EquationsHemant VermaNo ratings yet

- Shipment Monitoring FinalDocument303 pagesShipment Monitoring FinalArvin TejonesNo ratings yet

- Ii Dece Attendance Report-2023-24.Document6 pagesIi Dece Attendance Report-2023-24.Dhana lakshmiNo ratings yet

- Auction Calendar January, 23Document3 pagesAuction Calendar January, 23rashedul islamNo ratings yet

- Artificial Intelligence: Instruction To CandidatesDocument2 pagesArtificial Intelligence: Instruction To CandidatesUtsavNo ratings yet

- Talat MCDocument1,346 pagesTalat MCsoumya itteeraNo ratings yet

- 2023070442Document4 pages2023070442kafzal2311No ratings yet

- PJB - Labview - Interface 14-Jun-23 16 - 25 - 04Document28 pagesPJB - Labview - Interface 14-Jun-23 16 - 25 - 04Thenut PaisantaraNo ratings yet

- DMT Villahermosa Grocery 2Document2 pagesDMT Villahermosa Grocery 2Captain ObviousNo ratings yet

- Insentif 2019Document50 pagesInsentif 2019yujiookami_958766114No ratings yet

- The University of Burdwan: Provisional Results of 3 Years LL.B Hons. Semester Ii Examination, 2022Document15 pagesThe University of Burdwan: Provisional Results of 3 Years LL.B Hons. Semester Ii Examination, 2022adv.saritghoshNo ratings yet

- Examination Duty Chart - Google Sheets9Document1 pageExamination Duty Chart - Google Sheets9Rajni VermaNo ratings yet

- Maximum Retail Price List: ISO 9001:2008 CoDocument6 pagesMaximum Retail Price List: ISO 9001:2008 CoAvinash GautamNo ratings yet

- Updated Sitting Plan - 13.12.23 - 2nd Shift (11am) - 3rd InsemDocument7 pagesUpdated Sitting Plan - 13.12.23 - 2nd Shift (11am) - 3rd Insemstudent-01-91958273d0deNo ratings yet

- Relatório Da 20773Document9 pagesRelatório Da 20773Andre Luiz JuniorNo ratings yet

- Bihar NEET PG Security Deposit Refund List 2023Document44 pagesBihar NEET PG Security Deposit Refund List 2023divyabingi555No ratings yet

- Sem 1Document2 pagesSem 1Fauzan FyroneNo ratings yet

- Historial GPS: Equipo Nombre Equipo Nombre Interno Fecha ReporteDocument35 pagesHistorial GPS: Equipo Nombre Equipo Nombre Interno Fecha ReporteLuswing Raul Rueda HernandezNo ratings yet

- Year 1 Expenses and Cashflow ForecastDocument1 pageYear 1 Expenses and Cashflow ForecastTully HamutenyaNo ratings yet

- ME (1st) Dec2018Document2 pagesME (1st) Dec2018Deep InNo ratings yet

- TABLE: Element Forces - Frames Frame PDocument7 pagesTABLE: Element Forces - Frames Frame Pmoshi3824No ratings yet

- MEI CashflowDocument2 pagesMEI CashflowTshephang MorolongNo ratings yet

- Earth Hour Savings 2014Document4 pagesEarth Hour Savings 2014nashNo ratings yet

- 2023 - Plantilla para IR-6 e IR-17 - C.A.Document153 pages2023 - Plantilla para IR-6 e IR-17 - C.A.Wingston GuzmanNo ratings yet

- AbfzsdgfhDocument5 pagesAbfzsdgfhReza MurdaniNo ratings yet

- Accounts Fy 22 23 BaluchistanDocument104 pagesAccounts Fy 22 23 BaluchistanFarooq MaqboolNo ratings yet

- Housing Costs Ledger 2022 Jan To NovDocument6 pagesHousing Costs Ledger 2022 Jan To NovIan MusiimeNo ratings yet

- CG (5th) Dec2018Document2 pagesCG (5th) Dec2018Onkar SinghNo ratings yet

- Indent Track ReportDocument10 pagesIndent Track ReportOmkarNo ratings yet

- EOI Pool Selections Table (Nov-3-2020) PDFDocument18 pagesEOI Pool Selections Table (Nov-3-2020) PDFkbpatel123No ratings yet

- Rut 22696064-3 Realizadas 4Document9 pagesRut 22696064-3 Realizadas 4d.menaresabogadaNo ratings yet

- Data To Be Informed To The PartiesDocument34 pagesData To Be Informed To The Partieskavin kumarNo ratings yet

- Customer Statement Using TRN REF NO-233 (Sami)Document42 pagesCustomer Statement Using TRN REF NO-233 (Sami)samson27gNo ratings yet

- Libro 4Document12 pagesLibro 4LORENA CUESTANo ratings yet

- EXDS009Document51 pagesEXDS009Andi AlfianNo ratings yet

- UCP student fee payment challanDocument1 pageUCP student fee payment challanMahad ElahiNo ratings yet

- With SeismicDocument20 pagesWith Seismicmmm RumNo ratings yet

- Apm 2022 - 2024 Registro en AplicativoDocument30 pagesApm 2022 - 2024 Registro en AplicativoRICKNo ratings yet

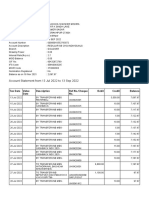

- Bank Statement Account SummaryDocument7 pagesBank Statement Account SummaryShashwat MishraNo ratings yet

- Cost Accounting-Ii: Instruction To CandidatesDocument2 pagesCost Accounting-Ii: Instruction To CandidatessumanNo ratings yet

- Lazada order transaction details reportDocument6 pagesLazada order transaction details reportJoriz SerillanoNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018Document10 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018MaricrisNo ratings yet

- EIM QT CheckerDocument4 pagesEIM QT Checkersir pahwNo ratings yet

- Bill Sivareddy2Document1 pageBill Sivareddy2yogikorramutlaNo ratings yet

- AICK - CWS Cost Operating Budget - FY 2023/2024Document41 pagesAICK - CWS Cost Operating Budget - FY 2023/2024m.fadhlyaugustami fadhlyNo ratings yet

- DCL ADocument4 pagesDCL AMohammad Bilal SagerNo ratings yet

- WZZ Cabin Attendant Workwear Regulations Revision 02Document55 pagesWZZ Cabin Attendant Workwear Regulations Revision 02Alex RoșuNo ratings yet

- Book 1Document50 pagesBook 1Prathamesh ShetyeNo ratings yet

- Screenshot 2023-06-23 at 12.20.38 PMDocument232 pagesScreenshot 2023-06-23 at 12.20.38 PMAshish KumauniNo ratings yet

- InternetDocument24 pagesInternetPrashant SinghNo ratings yet

- Intoduction To Computer NetworksDocument9 pagesIntoduction To Computer NetworksPrashant SinghNo ratings yet

- E PaymentDocument8 pagesE PaymentPrashant SinghNo ratings yet

- E CommerceDocument8 pagesE CommercePrashant SinghNo ratings yet

- AM (1st) Dec2019Document2 pagesAM (1st) Dec2019Prashant SinghNo ratings yet

- Accounts 2019 FinalDocument210 pagesAccounts 2019 FinalPrashant Singh100% (1)

- Fiscal policy explainedDocument4 pagesFiscal policy explainedPrashant SinghNo ratings yet

- Monetary Policy Approaches in IndiaDocument30 pagesMonetary Policy Approaches in IndiaRanjith DayalanNo ratings yet

- Fiscal Policy - 1Document6 pagesFiscal Policy - 1Prashant SinghNo ratings yet

- May 2022 PayslipDocument1 pageMay 2022 PayslipJustice Agbeko100% (1)

- Income Document UpdateDocument2 pagesIncome Document Update恩恩No ratings yet

- Cashflow Forecasting Using Montecarlo SimulationDocument111 pagesCashflow Forecasting Using Montecarlo SimulationDavid Esteban Meneses RendicNo ratings yet

- H12021 Egypt Venture Investment ReportDocument17 pagesH12021 Egypt Venture Investment ReportAmr ShakerNo ratings yet

- Debit Note TitleDocument6 pagesDebit Note TitleBhavesh Dinesh GohilNo ratings yet

- Cost AccountingDocument12 pagesCost AccountingAntonNo ratings yet

- IAS36 impairment quiz answersDocument4 pagesIAS36 impairment quiz answersTram Nguyen100% (1)

- Topic 1 Financial EnvironmentDocument26 pagesTopic 1 Financial EnvironmentThorapioMayNo ratings yet

- Session 6 SlidesDocument24 pagesSession 6 SlidesJay AgrawalNo ratings yet

- Memo of Part SatisfactnDocument5 pagesMemo of Part SatisfactnVandhiya ThevanNo ratings yet

- Polar SportsDocument15 pagesPolar SportsjordanstackNo ratings yet

- J&J FS AnalysisDocument5 pagesJ&J FS AnalysisEarl Justine FerrerNo ratings yet

- Intrinsic Values and Stock Prices PDFDocument2 pagesIntrinsic Values and Stock Prices PDFPhil Singleton100% (1)

- Straw ManDocument48 pagesStraw ManSilverBaronNo ratings yet

- Broker Business PlanDocument24 pagesBroker Business Plan陈永章0% (1)

- The Greatest Options Strategy Ever MadeDocument14 pagesThe Greatest Options Strategy Ever MadeAnkur DasNo ratings yet

- Ali Cloud Investment ProfileDocument23 pagesAli Cloud Investment ProfileFarhan SheikhNo ratings yet

- Bank Reconciliation MethodsDocument12 pagesBank Reconciliation MethodsKalven Perry Agustin80% (5)

- Tutorial 4 Q and ADocument7 pagesTutorial 4 Q and ASwee Yi LeeNo ratings yet

- MD Shohag Al-Mamun MBS ACMADocument6 pagesMD Shohag Al-Mamun MBS ACMATaslima AktarNo ratings yet

- Main Objects Clause in MOADocument5 pagesMain Objects Clause in MOApradeep15101981100% (1)

- Working Capital ManagementDocument7 pagesWorking Capital ManagementIsmail MarzukiNo ratings yet

- Solved Perry Chandler A Broker With Caveat Emptor LTD Offers FreeDocument1 pageSolved Perry Chandler A Broker With Caveat Emptor LTD Offers FreeM Bilal SaleemNo ratings yet

- Simon Property Group - Quick ReportDocument1 pageSimon Property Group - Quick Reporttkang79No ratings yet

- ISO Green and Sustainable FinanceDocument9 pagesISO Green and Sustainable FinanceWilliams wamboNo ratings yet

- Fabm1 Module 5Document16 pagesFabm1 Module 5Randy Magbudhi50% (4)

- Overview of Insurance Industry of BanglaDocument20 pagesOverview of Insurance Industry of BanglamR. sLimNo ratings yet

- Bes 104 - MarrDocument4 pagesBes 104 - MarrMahusay Neil DominicNo ratings yet

- FTFM - Final - MagandaDocument573 pagesFTFM - Final - MagandaJewelyn C. Espares-CioconNo ratings yet

- Sub Order LabelsDocument1 pageSub Order LabelsLubhNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)