You might also like

- SARFAESI-Act-of-2002 Lecture - 3Document26 pagesSARFAESI-Act-of-2002 Lecture - 3avipatelfb41No ratings yet

- Securitized Real Estate and 1031 ExchangesFrom EverandSecuritized Real Estate and 1031 ExchangesNo ratings yet

- PPSA Insight Paper 1Document4 pagesPPSA Insight Paper 1MAICA CARMEL SHIRL DIZONNo ratings yet

- IGL, General Banking Law (Riguera Lec)Document12 pagesIGL, General Banking Law (Riguera Lec)Ivan LeeNo ratings yet

- PPSADocument2 pagesPPSAchrislee81No ratings yet

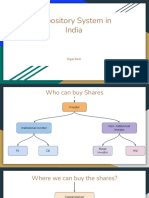

- Depository System in IndiaDocument23 pagesDepository System in IndiaKK SinghNo ratings yet

- Personal Property Security Act Outline StudentDocument10 pagesPersonal Property Security Act Outline StudentJosiah BalgosNo ratings yet

- Nirc of Icai: Ban On Physical Share Transfer of Listed Co-Last Date 31.3.2019 - Problem and SolutionsDocument36 pagesNirc of Icai: Ban On Physical Share Transfer of Listed Co-Last Date 31.3.2019 - Problem and SolutionsABHAYNo ratings yet

- Chapter 2 Banking An Operations 2Document79 pagesChapter 2 Banking An Operations 2ManavAgarwalNo ratings yet

- Types of ChargesDocument30 pagesTypes of ChargesganpatigajanandganeshNo ratings yet

- International Finance NotesDocument4 pagesInternational Finance NotesAbhishek JainNo ratings yet

- Secured TransactionsDocument3 pagesSecured TransactionsMoon MoonNo ratings yet

- Bankruptcy Outline FormattedDocument80 pagesBankruptcy Outline FormattedJohnNo ratings yet

- Security Over Collateral Pakistan Rizvi, Isa, Afridi & AngellDocument7 pagesSecurity Over Collateral Pakistan Rizvi, Isa, Afridi & AngellAmber TajwerNo ratings yet

- CBM T5 Class 15-16 Sec B 2020 FDocument31 pagesCBM T5 Class 15-16 Sec B 2020 FPratyush BaruaNo ratings yet

- (Economy) SARFAESI Act, Asset Reconstruction Company (ARC), Security Receipts (SR), QIB, DRT, Central RegistryDocument9 pages(Economy) SARFAESI Act, Asset Reconstruction Company (ARC), Security Receipts (SR), QIB, DRT, Central RegistryNarmatha BalachandarNo ratings yet

- Tang Hang Wu Intl Trust LawDocument21 pagesTang Hang Wu Intl Trust LawHarpott GhantaNo ratings yet

- Security Interests in Movable Properties in UgandaDocument6 pagesSecurity Interests in Movable Properties in UgandaKiwanuka SilvestNo ratings yet

- Chanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiDocument23 pagesChanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiashishNo ratings yet

- UNIT 2 CorporateDocument14 pagesUNIT 2 Corporatepreeti aggarwalNo ratings yet

- Commercial Law Study QuestionsDocument4 pagesCommercial Law Study QuestionsCara A.No ratings yet

- Lending and Taking Security in Nepal OverviewDocument19 pagesLending and Taking Security in Nepal OverviewNeupane Law AssociatesNo ratings yet

- LEGAL OPINION - Tuguegarao Property1Document3 pagesLEGAL OPINION - Tuguegarao Property1Duane MendozaNo ratings yet

- Lirag V SSS (Art. 1956) - RevisedDocument3 pagesLirag V SSS (Art. 1956) - RevisedMitchell YumulNo ratings yet

- 2022 Indonesia's Debt Restructuring & InsolvencyDocument15 pages2022 Indonesia's Debt Restructuring & InsolvencyAndhika Hananta RNo ratings yet

- Slides 2020 04 20 Wills and Administration of EstatesDocument58 pagesSlides 2020 04 20 Wills and Administration of EstatesFarhan KamarudinNo ratings yet

- Heldlawyersnewsletterjune 2012Document2 pagesHeldlawyersnewsletterjune 2012api-284203178No ratings yet

- PPSA and PPSA Rules PDFDocument5 pagesPPSA and PPSA Rules PDFTricia Montoya0% (1)

- 11.legal Aspects of AdvancesDocument27 pages11.legal Aspects of AdvancesavjoseNo ratings yet

- The Ins and Outs of Complex Commercial Complex Commercial Foreclosure ProceedingsDocument49 pagesThe Ins and Outs of Complex Commercial Complex Commercial Foreclosure ProceedingsArmond TrakarianNo ratings yet

- Task 1 Model Answer TranscriptDocument1 pageTask 1 Model Answer Transcriptk.a.ne.xm.ar.cusNo ratings yet

- Chattel MortgageDocument9 pagesChattel MortgageMa. Louise Aviso0% (1)

- Series 63 NotesDocument8 pagesSeries 63 Notesleo2331100% (2)

- Prepackaged Computer Software On CDS: TH THDocument5 pagesPrepackaged Computer Software On CDS: TH THAnonymous pTQWUdC3UBNo ratings yet

- Pledge of Shares - Law, Dislosures & ImplicationsDocument4 pagesPledge of Shares - Law, Dislosures & ImplicationsNidhi BothraNo ratings yet

- Real Estate in IndiaDocument9 pagesReal Estate in IndiaVandan SapariaNo ratings yet

- Rem V Antichresis Dec 17 2020Document5 pagesRem V Antichresis Dec 17 2020Anathema DeviceNo ratings yet

- Held Lawyers: Law MattersDocument2 pagesHeld Lawyers: Law Mattersapi-284203178No ratings yet

- Pledge of SharesDocument8 pagesPledge of Sharesshubhamgupta04101994No ratings yet

- Unit 2 CFDocument14 pagesUnit 2 CFpreeti aggarwalNo ratings yet

- BrochureDocument1 pageBrochureMarioNo ratings yet

- Legal Regulatory AspectsDocument82 pagesLegal Regulatory AspectsManavAgarwalNo ratings yet

- Restructuring and Insolvency in IndonesiaDocument17 pagesRestructuring and Insolvency in IndonesiaImron MahmudNo ratings yet

- Digest CredtransDocument19 pagesDigest Credtransmlucagbo80773No ratings yet

- Property Law II Life Saver!Document8 pagesProperty Law II Life Saver!Hadi Onimisi TijaniNo ratings yet

- Documentary Stamp TaxDocument2 pagesDocumentary Stamp TaxJoAnne Yaptinchay ClaudioNo ratings yet

- Cases:: Acme Shoe VS CA, 260 SCRA 714Document8 pagesCases:: Acme Shoe VS CA, 260 SCRA 714OmsimNo ratings yet

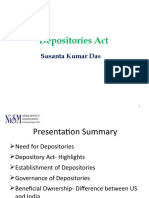

- Depository Act - LLM 21122022Document31 pagesDepository Act - LLM 21122022KavyaNo ratings yet

- Hong Kong Banking and Finance NoteDocument4 pagesHong Kong Banking and Finance NoteArrisNo ratings yet

- 2015 12 15 10 09 51 Law of Property Notes AnswersDocument25 pages2015 12 15 10 09 51 Law of Property Notes AnswersnimishaNo ratings yet

- Share Pledge AgreementDocument7 pagesShare Pledge AgreementVartika KhandujaNo ratings yet

- Law On Secrecy of Bank DepositsDocument4 pagesLaw On Secrecy of Bank DepositsKrizza TerradoNo ratings yet

- Lect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)Document5 pagesLect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)jNo ratings yet

- Lect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)Document7 pagesLect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)jNo ratings yet

- Memorandum L.I.T. GroupDocument3 pagesMemorandum L.I.T. GroupKiptoo EnockNo ratings yet

- Nego PrelimsDocument22 pagesNego PrelimsGrayNo ratings yet

- Law On Other Business TransactionsDocument11 pagesLaw On Other Business TransactionsBuenaventura, Elijah B.No ratings yet

- Lect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)Document7 pagesLect 1 Intro, Legal Background and Refresh Topics Lect 2 Main Frame N Biz Form (Sounds Not V Impt)jNo ratings yet

- Can You Sell Shares Which You Do Not Own? InsiderDocument4 pagesCan You Sell Shares Which You Do Not Own? InsiderKLNo ratings yet

- Who Should Be Liable For Online Anonymous DefamtionDocument15 pagesWho Should Be Liable For Online Anonymous DefamtionTzu MinminNo ratings yet

- The InternetDocument15 pagesThe InternetTzu MinminNo ratings yet

- The Dark Side of Social Media Romance-Civil Recourse For Catfish VictimsDocument25 pagesThe Dark Side of Social Media Romance-Civil Recourse For Catfish VictimsTzu MinminNo ratings yet

- Is Facebook A Publisher in Public It Says No But in Court It Says Yes-2Document4 pagesIs Facebook A Publisher in Public It Says No But in Court It Says Yes-2Tzu MinminNo ratings yet

- Accession TablesDocument5 pagesAccession TablesTzu MinminNo ratings yet

- SSRN Id3913792Document86 pagesSSRN Id3913792Tzu MinminNo ratings yet

- 2022 Chico - v. - Ciudadano20220817 11 103f8euDocument15 pages2022 Chico - v. - Ciudadano20220817 11 103f8euTzu MinminNo ratings yet

- 70789-1975-Amending Article 294 2 of The Revised Penal20220715-11-3xg323Document1 page70789-1975-Amending Article 294 2 of The Revised Penal20220715-11-3xg323Tzu MinminNo ratings yet

- 70885-1976-Amending Article 201 of Revised Penal Code20220624-11-NyvzwjDocument2 pages70885-1976-Amending Article 201 of Revised Penal Code20220624-11-NyvzwjTzu MinminNo ratings yet

- 2022 Basa Egami - v. - Bersales20220823 11 KyayafDocument14 pages2022 Basa Egami - v. - Bersales20220823 11 KyayafTzu MinminNo ratings yet

- Extending Tort Liability To Creators of Fake Profiles On Social NDocument25 pagesExtending Tort Liability To Creators of Fake Profiles On Social NTzu MinminNo ratings yet

- Cariaga v. RepublicDocument30 pagesCariaga v. RepublicTzu MinminNo ratings yet

- 309313-1936-Carriage of Goods by Sea Act20210723-12-11zz8y7Document7 pages309313-1936-Carriage of Goods by Sea Act20210723-12-11zz8y7Tzu MinminNo ratings yet

- Facebook Has A Political Fake News Problem Can We Fix It Without Eroding The First AmendmentDocument5 pagesFacebook Has A Political Fake News Problem Can We Fix It Without Eroding The First AmendmentTzu MinminNo ratings yet

- The History and Theory of The Law of Defamation. IIDocument25 pagesThe History and Theory of The Law of Defamation. IITzu MinminNo ratings yet

- Don't Feed The Trolls' Social Media and The Limits of Free SpeechDocument19 pagesDon't Feed The Trolls' Social Media and The Limits of Free SpeechTzu MinminNo ratings yet

- Social Media and Online Speech How Should Countries Regulate Tech GiantsDocument10 pagesSocial Media and Online Speech How Should Countries Regulate Tech GiantsTzu MinminNo ratings yet

- Roots of The Internet-A Personal HistoryDocument22 pagesRoots of The Internet-A Personal HistoryTzu MinminNo ratings yet

- Media Law and Defamation Torts-Recent DevelopmentsDocument18 pagesMedia Law and Defamation Torts-Recent DevelopmentsTzu MinminNo ratings yet

- Free Speech Savior or Shield For Scoundrels - An Empirical Study oDocument135 pagesFree Speech Savior or Shield For Scoundrels - An Empirical Study oTzu MinminNo ratings yet

- Legal Action Against Fake Account On Social MediaDocument4 pagesLegal Action Against Fake Account On Social MediaTzu MinminNo ratings yet

- Publisher or Platform It Doesnt MatterDocument9 pagesPublisher or Platform It Doesnt MatterTzu MinminNo ratings yet

- A Push To Make Social Media Companies Liable in Defamation Is Great For Newspapers and Lawyers But NoDocument4 pagesA Push To Make Social Media Companies Liable in Defamation Is Great For Newspapers and Lawyers But NoTzu MinminNo ratings yet

- Australia Social Media Users Can Be Publishers of Comments On Their Social Media Posts in To EstablisDocument3 pagesAustralia Social Media Users Can Be Publishers of Comments On Their Social Media Posts in To EstablisTzu MinminNo ratings yet

- .Ph-Attorneys of The PhilippinesDocument15 pages.Ph-Attorneys of The PhilippinesTzu MinminNo ratings yet

- How Facebook and Google Fund Global MisinformationDocument10 pagesHow Facebook and Google Fund Global MisinformationTzu MinminNo ratings yet

- 154250-2008-Bank - of - The - Philippine - Islands - V.20210505-11-1a41o4o 2Document8 pages154250-2008-Bank - of - The - Philippine - Islands - V.20210505-11-1a41o4o 2Tzu MinminNo ratings yet

- The Demise of Anonymity - A Constitutional Challenge To The ConveDocument45 pagesThe Demise of Anonymity - A Constitutional Challenge To The ConveTzu MinminNo ratings yet

- Sharp T&E OutlineDocument179 pagesSharp T&E OutlineJoseph DutsonNo ratings yet

- Situs V AsiatrustDocument2 pagesSitus V AsiatrustCedric100% (3)

- Cruz and Cruz v. Bancom Finance CorporationDocument4 pagesCruz and Cruz v. Bancom Finance CorporationYvonne MallariNo ratings yet

- 402 09a PDFDocument13 pages402 09a PDFAparna GovindbakshNo ratings yet

- TUTORIAL 6 - Aagney - B18ARA01Document6 pagesTUTORIAL 6 - Aagney - B18ARA01Aagney Alex RobinNo ratings yet

- Seville Vs National DevelopmentDocument20 pagesSeville Vs National DevelopmentJohnde MartinezNo ratings yet

- Duenas vs. MBTCDocument10 pagesDuenas vs. MBTCEyah LoberianoNo ratings yet

- The Law On Sales Course Syllabus 2021Document7 pagesThe Law On Sales Course Syllabus 2021boy abundaNo ratings yet

- Land Titles and Deeds - Chua Vs SorianoDocument1 pageLand Titles and Deeds - Chua Vs SorianoAbrahamNo ratings yet

- Law of Sales and Security DevicesDocument79 pagesLaw of Sales and Security DevicesAmsalu BelayNo ratings yet

- Introduction To Real Estate ManagementDocument15 pagesIntroduction To Real Estate ManagementRussel Ngo67% (3)

- Cases in Law On SalesDocument3 pagesCases in Law On SalesJean Jamailah TomugdanNo ratings yet

- Damac - Inventorydetail - Clone 4 Bdrs NiceDocument51 pagesDamac - Inventorydetail - Clone 4 Bdrs NiceAmar ElaskelyNo ratings yet

- WDEULADocument4 pagesWDEULApadremuerteNo ratings yet

- Privity of ContractDocument12 pagesPrivity of ContractR100% (1)

- Rights Leaflet 2007Document2 pagesRights Leaflet 2007SprytnyNo ratings yet

- (CD) 06. Reymundo Vs BandongDocument2 pages(CD) 06. Reymundo Vs BandongNicole ClianoNo ratings yet

- Deed of Conditional Sale SampleDocument2 pagesDeed of Conditional Sale SampleMary Gladys Remudaro-PaguiriganNo ratings yet

- Economics AssignmentDocument4 pagesEconomics AssignmentGIDEON NARTEH AHIANo ratings yet

- Total Value Less Than RM2 MillionDocument9 pagesTotal Value Less Than RM2 MillionAmmar MustaqimNo ratings yet

- Business Law FinalDocument4 pagesBusiness Law Finalibong tiriritNo ratings yet

- Last Will and TestamentDocument3 pagesLast Will and TestamentDiana Rose DalitNo ratings yet

- Land LawsDocument2 pagesLand LawsAman jainNo ratings yet

- Carta Del Govern A La Comissària de Drets Humans Del Consell D'europaDocument2 pagesCarta Del Govern A La Comissària de Drets Humans Del Consell D'europanaciodigitalNo ratings yet

- Heirs of Gregorio LopezDocument58 pagesHeirs of Gregorio LopezdaryllNo ratings yet

- Voluntary DealingsDocument17 pagesVoluntary DealingsdaryllNo ratings yet

- The Law of PropertyDocument75 pagesThe Law of PropertyEdward MokweriNo ratings yet

- Fundamental RightsDocument19 pagesFundamental RightsPankaj ChetryNo ratings yet

- Adverse Possession Case LawDocument251 pagesAdverse Possession Case LawSellappan RathinamNo ratings yet

- Corporate Banking 410 v1Document480 pagesCorporate Banking 410 v1pratik14janNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessFrom EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsFrom EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsRating: 4.5 out of 5 stars4.5/5 (2)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet