You might also like

- Database Management Systems: Understanding and Applying Database TechnologyFrom EverandDatabase Management Systems: Understanding and Applying Database TechnologyRating: 4 out of 5 stars4/5 (8)

- Gambar Kerja KlinikDocument24 pagesGambar Kerja KlinikMuh AlfinNo ratings yet

- WSR WK01 20230102-0108Document8 pagesWSR WK01 20230102-0108CHRISMAR ZALSOSNo ratings yet

- 18-Tipikal Tower CC and DD, DDR-Layout1Document1 page18-Tipikal Tower CC and DD, DDR-Layout1randi wirdanaNo ratings yet

- Cot 201009121Document10 pagesCot 201009121andrewbloggerNo ratings yet

- Adobe Scan 8 Sep 2023Document2 pagesAdobe Scan 8 Sep 2023ajayjadeja0758No ratings yet

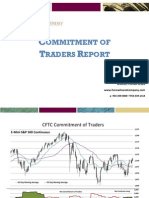

- CoT 09092010Document10 pagesCoT 09092010ZerohedgeNo ratings yet

- WSR WK26 20230626-0702Document9 pagesWSR WK26 20230626-0702CHRISMAR ZALSOSNo ratings yet

- Truly, A Perfect Match For Young, Busy, Productive Family.: @rancamayaestateDocument6 pagesTruly, A Perfect Match For Young, Busy, Productive Family.: @rancamayaestateviviane putriNo ratings yet

- Transit Times Volume 9, Number 3Document5 pagesTransit Times Volume 9, Number 3AC Transit HistorianNo ratings yet

- E Topo 2 Icosahedron 4Document1 pageE Topo 2 Icosahedron 4argaborNo ratings yet

- Gambar Sasana KarateDocument3 pagesGambar Sasana KarateEdyNo ratings yet

- 1001-155-CIV-DWG-BARA-002 Drawing For Foundation Acid 1600 KL (155-TK-17 & 155-TK-18) (R) 08122023Document1 page1001-155-CIV-DWG-BARA-002 Drawing For Foundation Acid 1600 KL (155-TK-17 & 155-TK-18) (R) 08122023mhajaraswadi2023No ratings yet

- Sec Suport BuildingDocument29 pagesSec Suport BuildingIMTIYAZ ALINo ratings yet

- WSR WK27 20230703-0709 1Document9 pagesWSR WK27 20230703-0709 1CHRISMAR ZALSOSNo ratings yet

- Tampak Samping GT GH 2: RevisionsDocument1 pageTampak Samping GT GH 2: Revisionsazrhelmy1No ratings yet

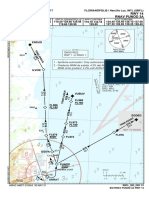

- SBFL Rnav-Punod-3a-Rwy14 Sid 20210520Document1 pageSBFL Rnav-Punod-3a-Rwy14 Sid 20210520jose netoNo ratings yet

- LSTAR Residential Market Activity March 2018Document28 pagesLSTAR Residential Market Activity March 2018matthewtrevithickNo ratings yet

- ZNERA - PROJECTS - Sports Complex PDFDocument15 pagesZNERA - PROJECTS - Sports Complex PDFNajmus ChowdharyNo ratings yet

- Green Corner: Amadeus Gate Kingshop Alfresco Dining CommercialDocument2 pagesGreen Corner: Amadeus Gate Kingshop Alfresco Dining CommercialMumut Mutia FatmawatiNo ratings yet

- Vias 2 Pro. Final Felipe y ShirlyDocument16 pagesVias 2 Pro. Final Felipe y ShirlyCexar Rodriguez CNo ratings yet

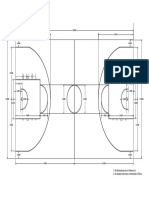

- Basketball CourtDocument1 pageBasketball CourtVaibhav GuptaNo ratings yet

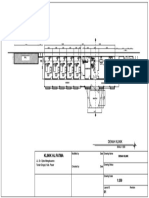

- Denah KlinikDocument1 pageDenah Klinikfajar putraNo ratings yet

- Illustration 1.1: Grande Trek: Account Balances 1 October, 2020Document7 pagesIllustration 1.1: Grande Trek: Account Balances 1 October, 2020J DashNo ratings yet

- 2023 R1 USEN IncentiveTracker 4webDocument1 page2023 R1 USEN IncentiveTracker 4webMelissaNo ratings yet

- DENAHDocument1 pageDENAHMuhammad AbdillahNo ratings yet

- S-12 FCD Almeda 2 CanopyDocument1 pageS-12 FCD Almeda 2 CanopyAlvin SanvictoresNo ratings yet

- 37 U-DitchDocument1 page37 U-DitchDonzNo ratings yet

- Monamani BedudipaDocument1 pageMonamani BedudipaZuna Lihardo PoerbaNo ratings yet

- Lower Trendline Upper Trendline: Jul Jul 2 Jul 3 Jul 4 Jul 5 Jul 8 Jul 9 Jul 10Document1 pageLower Trendline Upper Trendline: Jul Jul 2 Jul 3 Jul 4 Jul 5 Jul 8 Jul 9 Jul 10Haider KHNo ratings yet

- Circle Rates 2009-2010 in Gurgaon For Flats, Plots, and Agricultural Land - Gurgaon PropertyDocument15 pagesCircle Rates 2009-2010 in Gurgaon For Flats, Plots, and Agricultural Land - Gurgaon Propertyqubrex1100% (2)

- Layout Plan For Musical Fountain Viewing Duct in Island at VinayakasagarDocument1 pageLayout Plan For Musical Fountain Viewing Duct in Island at VinayakasagarAecom IndiaNo ratings yet

- Airport Information: Details For PALONEGRODocument50 pagesAirport Information: Details For PALONEGRODaniel CalleNo ratings yet

- SKBG - BucaramangaDocument27 pagesSKBG - Bucaramangajimenezgrajalesjuanjose18No ratings yet

- Pic Building ConcreteDocument23 pagesPic Building ConcreteIMTIYAZ ALINo ratings yet

- Pac56 Mx13specsheet 2021 Final DigitalhiresDocument2 pagesPac56 Mx13specsheet 2021 Final Digitalhiresgaurao.pandeNo ratings yet

- MX 13 Spec SheetDocument2 pagesMX 13 Spec SheetHarish KumarNo ratings yet

- SBVT - Rnav Isila 1b - Sarla 1b Rwy 06 - Star - 20230323Document1 pageSBVT - Rnav Isila 1b - Sarla 1b Rwy 06 - Star - 20230323Valiense FilmesNo ratings yet

- BSI CCF DWG CS 140 - LAUNDRY ModelDocument1 pageBSI CCF DWG CS 140 - LAUNDRY Modelrony 2222No ratings yet

- Ground Floor Plan - 1St Floor PlanDocument1 pageGround Floor Plan - 1St Floor Plankrisna kingNo ratings yet

- Soal PT Buana Laporan KeuanganDocument15 pagesSoal PT Buana Laporan Keuangankakafahreza25No ratings yet

- Brosur Kuantan Regency MlatiDocument9 pagesBrosur Kuantan Regency MlatiDeni JuliyandoNo ratings yet

- Rjaa PDFDocument94 pagesRjaa PDFRokhayati 123100% (2)

- Accounts: Trial Balance Adjustments Adjusted T.BDocument2 pagesAccounts: Trial Balance Adjustments Adjusted T.BJaqueline Sarkis IssaNo ratings yet

- Denah Tampak Potongan Rumah HerbaDocument5 pagesDenah Tampak Potongan Rumah HerbaNoto NotoNo ratings yet

- Hoffman Ben WASH DC IOMDocument25 pagesHoffman Ben WASH DC IOMAbdulNo ratings yet

- SapmDocument22 pagesSapmPraval SantarNo ratings yet

- 02.a3.denah Pintu Dan JendelaDocument1 page02.a3.denah Pintu Dan Jendelabibin capellaNo ratings yet

- Loading: Displacement / Micrometer Force / Micro NewtonDocument7 pagesLoading: Displacement / Micrometer Force / Micro NewtonasamNo ratings yet

- Music Mart FormatDocument3 pagesMusic Mart FormatSana LeeNo ratings yet

- SCP Car Rear Calculator For Other ScalesDocument55 pagesSCP Car Rear Calculator For Other Scalesslakshminarayanan8162No ratings yet

- 2023 4 Trial BalanceDocument4 pages2023 4 Trial BalanceAhmad SyafeiNo ratings yet

- Balance Sheet Current Assets: Cash AR InventoryDocument31 pagesBalance Sheet Current Assets: Cash AR InventoryNguyenNo ratings yet

- Ket CauDocument2 pagesKet CauAnh GiangNo ratings yet

- SMP 1 Weekly Overall Progress 20240113Document262 pagesSMP 1 Weekly Overall Progress 20240113upickrahmanNo ratings yet

- Pha & ABC Combo c1 GT 4-2 (100-1700 MV)Document1 pagePha & ABC Combo c1 GT 4-2 (100-1700 MV)eggboyz 99No ratings yet

- MB ĐỂ XE HẦM 1 BLOCK BDocument1 pageMB ĐỂ XE HẦM 1 BLOCK BVỹ “KEIBA” Nguyễn NgọcNo ratings yet

- 2D + DETAIL RUMAH 8X12mDocument12 pages2D + DETAIL RUMAH 8X12mFajrNurMaulanaNo ratings yet

- BotanikaDocument22 pagesBotanikaMarjan FaberNo ratings yet

- TA 34 E1229 Injector GreaseDocument4 pagesTA 34 E1229 Injector GreasejajajaparudinNo ratings yet

- Engine D8-600Document2 pagesEngine D8-600jajajaparudinNo ratings yet

- Procedure For Cleaning An Engine Lubrication System When Contaminated With Engine Coolant Containing Antifreeze (1000, 1348, 1395) (M0107162-01)Document2 pagesProcedure For Cleaning An Engine Lubrication System When Contaminated With Engine Coolant Containing Antifreeze (1000, 1348, 1395) (M0107162-01)jajajaparudinNo ratings yet

- Trouble Shooting Hydrolik pc210Document5 pagesTrouble Shooting Hydrolik pc210jajajaparudinNo ratings yet

- Fire SurpressionDocument5 pagesFire SurpressionjajajaparudinNo ratings yet

- D T C Kode Error UD QuesterDocument57 pagesD T C Kode Error UD Questerjajajaparudin0% (1)

- Materi 1 - Biodiesel Di IndonesiaDocument50 pagesMateri 1 - Biodiesel Di IndonesiajajajaparudinNo ratings yet

- Thermodynamics II Internal Combustion Engines: Mohsin Mohd SiesDocument50 pagesThermodynamics II Internal Combustion Engines: Mohsin Mohd SiesGareth LeeNo ratings yet

- Battery Charger CalculationDocument7 pagesBattery Charger CalculationBimoBrillianta100% (2)

- 0 50 S Fuel OperationDocument56 pages0 50 S Fuel Operationargentum19619692No ratings yet

- Donaldson Hydraulic Filters Catalog PDFDocument0 pagesDonaldson Hydraulic Filters Catalog PDFRaul MoscosoNo ratings yet

- Fire Officer Reviewer 1Document20 pagesFire Officer Reviewer 1Hazelnuts Inagi100% (6)

- Racecar Le Mans 2014Document68 pagesRacecar Le Mans 2014Mandar Arun HazareNo ratings yet

- Pyrot Assembly InstallationDocument52 pagesPyrot Assembly InstallationDimitris NikouNo ratings yet

- Equivalent Table Lub OilDocument4 pagesEquivalent Table Lub OilDarmawan Putranto100% (1)

- Corolla Engine ControlDocument12 pagesCorolla Engine ControlPatricio ValenciaNo ratings yet

- Bombas de Inyeccion Tipo DistribuidorDocument36 pagesBombas de Inyeccion Tipo DistribuidorEDWINNo ratings yet

- LG Ac VM122H6Document72 pagesLG Ac VM122H6alextroyer100% (1)

- PW Manual MM 1Document388 pagesPW Manual MM 1Alem Martin100% (4)

- EEMUA Storage PDFDocument1 pageEEMUA Storage PDFbenabdallah131No ratings yet

- Function 3 YayayaDocument23 pagesFunction 3 YayayaYusuf Bagus PangestuNo ratings yet

- LNG CourseDocument4 pagesLNG CourseRuslan ZakirovNo ratings yet

- Manual Mtto Arrow C106Document120 pagesManual Mtto Arrow C106Anonymous khOZ5G5We100% (1)

- Nikos Kostas Master ThesisDocument99 pagesNikos Kostas Master ThesisVILLAINZ83No ratings yet

- Brazil Ethanol Industry - Constanza Valdes - BIO02 - 2011Document46 pagesBrazil Ethanol Industry - Constanza Valdes - BIO02 - 2011Jose M. Gomez RuedaNo ratings yet

- GATE Chemical Engineering 2007 PDFDocument31 pagesGATE Chemical Engineering 2007 PDFSHREENo ratings yet

- Acetylated Castor Oil - Preparation and Thermal DecompositionDocument7 pagesAcetylated Castor Oil - Preparation and Thermal DecompositionPee Hai NingNo ratings yet

- Gas Station Bus-WPS OfficeDocument3 pagesGas Station Bus-WPS OfficeAnnabelle BuenaflorNo ratings yet

- YMA Palai - Feb - 19 - 2017Document4 pagesYMA Palai - Feb - 19 - 2017bawihpuiapaNo ratings yet

- Peugeot 5008 Prices and Specifications BrochureDocument14 pagesPeugeot 5008 Prices and Specifications BrochureUroš KroflNo ratings yet

- Conceptual Cost Estimating Manual, Second Edition PDFDocument356 pagesConceptual Cost Estimating Manual, Second Edition PDFEmanuel Frutis67% (3)

- G440X G440QXDocument2 pagesG440X G440QXKhawaja Kashif QadeerNo ratings yet

- PDH Shell and Tube Heat Exchangers - Basic Calculations PDFDocument31 pagesPDH Shell and Tube Heat Exchangers - Basic Calculations PDFmordidomiNo ratings yet

- Autonomous Maintenance Step 4 Lubrication ModuleDocument30 pagesAutonomous Maintenance Step 4 Lubrication ModulejesusmemNo ratings yet

- Performances in Tank CleaningDocument5 pagesPerformances in Tank CleaningGenghu YeNo ratings yet

- Ecu Mazda 3 Motor 2.0Document4 pagesEcu Mazda 3 Motor 2.0lasso2004100% (4)

- Alternative Fuels Text BookDocument466 pagesAlternative Fuels Text BookSAHIL Raj100% (3)