You might also like

- 21 100casesgb PDFDocument172 pages21 100casesgb PDFbenzekriziedNo ratings yet

- Egmont Group - 100 CasesDocument172 pagesEgmont Group - 100 CasesKhalid Shamim ShipluNo ratings yet

- Enforcing Global Law International ArbitDocument42 pagesEnforcing Global Law International ArbitYassine BenasserNo ratings yet

- Transparency and Accountability in Government Financial ManagementDocument80 pagesTransparency and Accountability in Government Financial ManagementMata KAmi Tao100% (1)

- 1 PDFDocument54 pages1 PDFSanaz NeczadNo ratings yet

- Using Third Party Information Reports To Assist Taxpayers Meet Their Return Filing Obligations - Country Experiences With The Use of Pre-Populated Personal Tax ReturnsDocument24 pagesUsing Third Party Information Reports To Assist Taxpayers Meet Their Return Filing Obligations - Country Experiences With The Use of Pre-Populated Personal Tax ReturnsAli MiftahudinNo ratings yet

- Advance Tax Rulings Rarely Used Despite Legal UncertaintyDocument36 pagesAdvance Tax Rulings Rarely Used Despite Legal UncertaintySushil JindalNo ratings yet

- Audit Plans Audit S Papers Archiv Es Freque Ntly Asked Questi Ons (FAQ) RAA Photo GalleryDocument11 pagesAudit Plans Audit S Papers Archiv Es Freque Ntly Asked Questi Ons (FAQ) RAA Photo GalleryZakia ElhamNo ratings yet

- The Place of Arbitration in The Conflict of Laws of InternationalDocument39 pagesThe Place of Arbitration in The Conflict of Laws of InternationalBeatta RamirezNo ratings yet

- Reviewing The OECD Harmful Tax Initiative: The St. Vincent and The Grenadines Perspective by Louise MitchellDocument16 pagesReviewing The OECD Harmful Tax Initiative: The St. Vincent and The Grenadines Perspective by Louise MitchellLogan's LtdNo ratings yet

- More Tax Evasion Research Required in New Millennium: Crime, Law & Social Change 31: 91-104, 1999Document14 pagesMore Tax Evasion Research Required in New Millennium: Crime, Law & Social Change 31: 91-104, 1999Silvia MagdiciNo ratings yet

- Function of WtoDocument12 pagesFunction of WtoSuman ChaudharyNo ratings yet

- TAX AVOIDANCE VS EVASION VS MITIGATIONDocument14 pagesTAX AVOIDANCE VS EVASION VS MITIGATIONShajed100% (1)

- Tax Fraud and The Rule of Law: January 2018Document38 pagesTax Fraud and The Rule of Law: January 2018amanualNo ratings yet

- A PEA 2000AOSMcLeayOrdelheideYoungDocument21 pagesA PEA 2000AOSMcLeayOrdelheideYoungWirdaNo ratings yet

- FATF GAFI. Annual Report 1995 - 1996.Document48 pagesFATF GAFI. Annual Report 1995 - 1996.Tadeo Leandro FernándezNo ratings yet

- The Case For Accounting Regulation: A Theoretical Approach: SearchDocument5 pagesThe Case For Accounting Regulation: A Theoretical Approach: SearchbabylovelylovelyNo ratings yet

- Good GovernanceDocument272 pagesGood GovernanceVenianNo ratings yet

- Some Aspects About International Tax Com PDFDocument50 pagesSome Aspects About International Tax Com PDFMohammedAlmohammedNo ratings yet

- EScholarship UC Item 6zn9p98bDocument20 pagesEScholarship UC Item 6zn9p98bHoang PhuNo ratings yet

- Ejournal of Tax ResearchDocument21 pagesEjournal of Tax ResearchhenfaNo ratings yet

- 2004 2005 ML Typologies ENGDocument95 pages2004 2005 ML Typologies ENGEugeniu CaţaveicăNo ratings yet

- Report On Presumptive Direct TaxationDocument161 pagesReport On Presumptive Direct TaxationTanvi DeshmukhNo ratings yet

- Introduction To Principles and Application KEVIN HOLMES 2Document116 pagesIntroduction To Principles and Application KEVIN HOLMES 2DogeNo ratings yet

- ICTD International Tax Literature Review - V2Document54 pagesICTD International Tax Literature Review - V2Chiara WhiteNo ratings yet

- 56 1palan PDFDocument27 pages56 1palan PDFavijitfNo ratings yet

- PHD Research Outline Proposal 2011 Clement ChakDocument6 pagesPHD Research Outline Proposal 2011 Clement ChakDiego P00No ratings yet

- Analysis of Financial Accounting Standards and Their Effects On Financial Reporting and Practices of Modern Business Organizations in Nigeria.Document9 pagesAnalysis of Financial Accounting Standards and Their Effects On Financial Reporting and Practices of Modern Business Organizations in Nigeria.Alexander DeckerNo ratings yet

- CRP11 Add1 Tax EvasionDocument19 pagesCRP11 Add1 Tax EvasionLenin FernándezNo ratings yet

- FATF GAFI. Annual Report 1998 - 1999.Document74 pagesFATF GAFI. Annual Report 1998 - 1999.Tadeo Leandro FernándezNo ratings yet

- International Tax Evasion in The Global Information Age (David S. Kerzner, David W. Chodikoff)Document443 pagesInternational Tax Evasion in The Global Information Age (David S. Kerzner, David W. Chodikoff)Sora FonNo ratings yet

- International Taxation of Hybrid EntitiesDocument11 pagesInternational Taxation of Hybrid EntitiesNilormi MukherjeeNo ratings yet

- Chapter Two Golis UniversityDocument40 pagesChapter Two Golis UniversityCabdixakiim-Tiyari Cabdillaahi AadenNo ratings yet

- 2018 Design Assessment Tax Incentives UN CIATDocument187 pages2018 Design Assessment Tax Incentives UN CIATyaredNo ratings yet

- CRM 316 Module 1Document16 pagesCRM 316 Module 1Raymart LogadorNo ratings yet

- Rusia Moralul FiscalDocument84 pagesRusia Moralul FiscalIonut-Mihai MitritaNo ratings yet

- Tax Havens and Money Laundering in IndiaDocument12 pagesTax Havens and Money Laundering in IndiaVaishali RathiNo ratings yet

- Financial Transparency Index Outlines Research ProposalDocument8 pagesFinancial Transparency Index Outlines Research Proposalpatrick_joyNo ratings yet

- Foro Daf Comp GF WD (2018) 66.enDocument4 pagesForo Daf Comp GF WD (2018) 66.enJASSEN BAZANNo ratings yet

- Tax Compliance and Self-Assessment Models ExploredDocument16 pagesTax Compliance and Self-Assessment Models ExploredarekdarmoNo ratings yet

- Assignment 2Document10 pagesAssignment 2Mohammad ArafatNo ratings yet

- Integrated Learning Product: Journal of Economics, Finance and Administrative ScienceDocument12 pagesIntegrated Learning Product: Journal of Economics, Finance and Administrative ScienceKevin LozanoNo ratings yet

- FATF GAFI. Annual Report 1994 - 1995.Document24 pagesFATF GAFI. Annual Report 1994 - 1995.Tadeo Leandro FernándezNo ratings yet

- Research Paper: Tax Haven Listing in Multiple Hues: Blind, Winking or Conniving?Document54 pagesResearch Paper: Tax Haven Listing in Multiple Hues: Blind, Winking or Conniving?Ardis Septi ERNo ratings yet

- Forecasting Fra Forecasting Fraudulent Financial Statementsudulent Financial StatementsDocument7 pagesForecasting Fra Forecasting Fraudulent Financial Statementsudulent Financial StatementskhuongcomputerNo ratings yet

- Journal of Law and Society - 2020 - Feria - Tax Fraud and Selective Law EnforcementDocument31 pagesJournal of Law and Society - 2020 - Feria - Tax Fraud and Selective Law EnforcementHassan AbbasNo ratings yet

- Qmul It TestDocument4 pagesQmul It Testmondon.marie24No ratings yet

- Court Fees: Charging The User As A Way To Mitigate Judicial CongestionDocument15 pagesCourt Fees: Charging The User As A Way To Mitigate Judicial Congestionluibook97No ratings yet

- Fiscal ParadiseDocument24 pagesFiscal ParadiseAndreea Telegdi MoodyNo ratings yet

- Current Challenges Identifying Beneficial Owners PDFDocument15 pagesCurrent Challenges Identifying Beneficial Owners PDFErnesto CordovaNo ratings yet

- Avi-Yonah The 1923 Report and The International Tax RevolutionDocument11 pagesAvi-Yonah The 1923 Report and The International Tax RevolutionRoberto RamosNo ratings yet

- Full Cost Accounting: An Agenda For ActionDocument174 pagesFull Cost Accounting: An Agenda For ActionAtif RehmanNo ratings yet

- 2019 - BTR - Issue - 4 - Print - Anton (25.08.2019)Document25 pages2019 - BTR - Issue - 4 - Print - Anton (25.08.2019)Milway Tupayachi AbarcaNo ratings yet

- Factors that contribute to profitability & historical rules for allocating taxing rightsDocument9 pagesFactors that contribute to profitability & historical rules for allocating taxing rightsdhirendraNo ratings yet

- Taxation Law ProjectDocument20 pagesTaxation Law ProjectJain Rajat ChopraNo ratings yet

- Fact-Finding in Collective Bargaining: A Proven Dispute Resolution ToolFrom EverandFact-Finding in Collective Bargaining: A Proven Dispute Resolution ToolRating: 5 out of 5 stars5/5 (1)

- State Tax Competition ("Guerra Fiscal"): comparative study of the Brazilian and Swiss tax collection power and revenue sharing systemsFrom EverandState Tax Competition ("Guerra Fiscal"): comparative study of the Brazilian and Swiss tax collection power and revenue sharing systemsNo ratings yet

- CFA (76) 7part4rev1EFDocument28 pagesCFA (76) 7part4rev1EFHoracio VianaNo ratings yet

- Rlstricted Co-Operation and Development: Mr. PhilippDocument8 pagesRlstricted Co-Operation and Development: Mr. PhilippHoracio VianaNo ratings yet

- 2009 6 29 ST - 11538 - 2009 - INIT - enDocument1 page2009 6 29 ST - 11538 - 2009 - INIT - enHoracio VianaNo ratings yet

- L'C - Ri,' - 26th TH Uary,: Co-O .., TIO1TDocument10 pagesL'C - Ri,' - 26th TH Uary,: Co-O .., TIO1THoracio VianaNo ratings yet

- Council Report on Code of Conduct Group Business TaxationDocument8 pagesCouncil Report on Code of Conduct Group Business TaxationHoracio VianaNo ratings yet

- 1960 WP FC-WP14 (60) 2EDocument5 pages1960 WP FC-WP14 (60) 2EHoracio VianaNo ratings yet

- 1960 Fiscal Committee FC-M (60) 5EDocument11 pages1960 Fiscal Committee FC-M (60) 5EHoracio VianaNo ratings yet

- 1996 Arbitration Report DAFFE-CFA-WP6 (96) 2EDocument17 pages1996 Arbitration Report DAFFE-CFA-WP6 (96) 2EHoracio VianaNo ratings yet

- 1982 Corresp Adj DAFFE-CFA-WP1 (82) 2EDocument4 pages1982 Corresp Adj DAFFE-CFA-WP1 (82) 2EHoracio VianaNo ratings yet

- 1986 Biac Comments DAFFE-CFA-WP1 (86) 8EDocument40 pages1986 Biac Comments DAFFE-CFA-WP1 (86) 8EHoracio VianaNo ratings yet

- Public CommentsDocument413 pagesPublic CommentsHoracio VianaNo ratings yet

- Money Laundering and Illegal Wildlife TradeDocument72 pagesMoney Laundering and Illegal Wildlife TradeHoracio VianaNo ratings yet

- 1980 Report Correp Adjust DAF-CFA-WP6 (80) 10EDocument9 pages1980 Report Correp Adjust DAF-CFA-WP6 (80) 10EHoracio VianaNo ratings yet

- What Is CryptocurrencyDocument4 pagesWhat Is Cryptocurrencypratham KadamNo ratings yet

- Explai The Business Model of Nagad and SurjopayDocument5 pagesExplai The Business Model of Nagad and SurjopayGolam ZelaniNo ratings yet

- 2023 PTD 541 161BDocument8 pages2023 PTD 541 161BYour AdvocateNo ratings yet

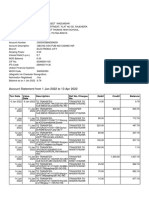

- Account Statement From 1 Jan 2022 To 13 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 1 Jan 2022 To 13 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubhojeet MazumdarNo ratings yet

- Jesse A Stancil: On-Line Self Select PIN Without Direct Debit Tax Return Signature/Consent To DisclosureDocument11 pagesJesse A Stancil: On-Line Self Select PIN Without Direct Debit Tax Return Signature/Consent To DisclosureJesse StancilNo ratings yet

- David Navera FL Only PDFDocument2 pagesDavid Navera FL Only PDFDavid N. Navera JrNo ratings yet

- Ripple CryptocurrencyDocument5 pagesRipple CryptocurrencyRipple Coin NewsNo ratings yet

- Swiggy Order 44287204323 PDFDocument2 pagesSwiggy Order 44287204323 PDFAmazon AmazonNo ratings yet

- Bir Form No. Title of The Form Description Filing Date Where To File 1901Document2 pagesBir Form No. Title of The Form Description Filing Date Where To File 1901cessbrightNo ratings yet

- Corporate Taxation in BangladeshDocument8 pagesCorporate Taxation in Bangladeshskn092No ratings yet

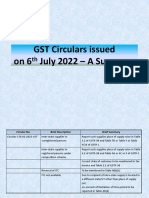

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- PaymentsDocument6 pagesPaymentsDoniNo ratings yet

- CGST & Central Excise - Range OfficeDocument2 pagesCGST & Central Excise - Range OfficeAYUSH PRADHANNo ratings yet

- Account Statement From 1 Mar 2019 To 12 Feb 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 1 Mar 2019 To 12 Feb 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAkhil ThannikalNo ratings yet

- U.S. Visa Application Fee Deposit SlipDocument2 pagesU.S. Visa Application Fee Deposit SlipAya KhalifaNo ratings yet

- CIR v. de La SalleDocument3 pagesCIR v. de La SalleGabriel AdoraNo ratings yet

- Financial Projection: Total Goods Available For SalesDocument7 pagesFinancial Projection: Total Goods Available For SalesClau MagahisNo ratings yet

- Print GSTDocument1 pagePrint GSTSourav GhoshNo ratings yet

- Account Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSumon SarkarNo ratings yet

- What is an Open Check? (39 charactersDocument5 pagesWhat is an Open Check? (39 charactersEfren ChanNo ratings yet

- Tax Guide On Philippine Taxation - Bureau of Internal RevenueDocument11 pagesTax Guide On Philippine Taxation - Bureau of Internal RevenueRadh KamalNo ratings yet

- Donors TaxDocument16 pagesDonors TaxNikkolae LibreaNo ratings yet

- TMC Vs CIRDocument3 pagesTMC Vs CIREllaine BernardinoNo ratings yet

- TAXATION KEY POINTSDocument3 pagesTAXATION KEY POINTScherry blossomNo ratings yet

- Collection Information Statement For Wage Earners and Self-Employed IndividualsDocument7 pagesCollection Information Statement For Wage Earners and Self-Employed IndividualsAnonymous dfLfinUrp60% (5)

- G.R. No. 147188 September 14, 2004 Commissioner of Internal Revenue Vs - The Estate of Benigno P. Toda, JR.Document2 pagesG.R. No. 147188 September 14, 2004 Commissioner of Internal Revenue Vs - The Estate of Benigno P. Toda, JR.micheleNo ratings yet

- Mar 16 BillDocument1 pageMar 16 BillanandNo ratings yet

- Invoice 18Document1 pageInvoice 18kuldeep singhNo ratings yet

- PresentationDocument5 pagesPresentationAnsh RebelloNo ratings yet

- 2022 CALIFORNIA EMPLOYER'S GUIDE TO PAYROLL TAXESDocument126 pages2022 CALIFORNIA EMPLOYER'S GUIDE TO PAYROLL TAXESreddymspNo ratings yet