You might also like

- Re Industrypack Income Tax 2010Document2 pagesRe Industrypack Income Tax 2010So LokNo ratings yet

- Thin CapitalizationDocument41 pagesThin Capitalizationsobaseki1No ratings yet

- LLPs Offer Limited Liability for PartnersDocument5 pagesLLPs Offer Limited Liability for PartnersGiancarlo CobinoNo ratings yet

- Revisiting Improperly Accumulated Earnings TaxDocument2 pagesRevisiting Improperly Accumulated Earnings TaxTara ManteNo ratings yet

- Which WACC WhenDocument6 pagesWhich WACC Whenkalyan_mallaNo ratings yet

- Tax Watch Bulletin Tax Amendment Bills 2023Document22 pagesTax Watch Bulletin Tax Amendment Bills 2023BonnieNo ratings yet

- 13 Chapter VDocument103 pages13 Chapter VKaRan K KHetaniNo ratings yet

- Tax Implications On Mergers and Acquisitions ProcessDocument13 pagesTax Implications On Mergers and Acquisitions Processgayathris111No ratings yet

- Tax Implications On Mergers and Acquisitions ProcessDocument13 pagesTax Implications On Mergers and Acquisitions Processsiddharth pandeyNo ratings yet

- 2 PDFDocument13 pages2 PDFKaRan K KHetaniNo ratings yet

- Tax II OutlineDocument68 pagesTax II OutlineEdmond MenchavezNo ratings yet

- Introduction of Corporate Tax in The UaeDocument8 pagesIntroduction of Corporate Tax in The UaeOnice BallelosNo ratings yet

- Which Way To Relief From The Double TaxationDocument4 pagesWhich Way To Relief From The Double Taxationarbbee4095305No ratings yet

- Investment Tax Incentives ExplainedDocument12 pagesInvestment Tax Incentives ExplainedSeid KassawNo ratings yet

- Due Diligence-Tax Due Dil - FinalDocument6 pagesDue Diligence-Tax Due Dil - FinalEljoe VinluanNo ratings yet

- Shipping Leasing Offers Tax Efficiencies and FlexibilityDocument6 pagesShipping Leasing Offers Tax Efficiencies and FlexibilityKofikoduah100% (1)

- Taxation Aspects of M&A: Capital GainDocument4 pagesTaxation Aspects of M&A: Capital Gainnikesh_shah_1No ratings yet

- Valuing DTAsDocument20 pagesValuing DTAspsdubyaNo ratings yet

- Elective Paper GST CPTDocument169 pagesElective Paper GST CPTVani BalajiNo ratings yet

- Partnership_taxation_in_the_United_StatesDocument9 pagesPartnership_taxation_in_the_United_StatesjonfernquestNo ratings yet

- HND Unit 30 TaxationDocument12 pagesHND Unit 30 TaxationzoomNo ratings yet

- Corporate Tax PlanningDocument8 pagesCorporate Tax PlanningTumie Lets0% (1)

- A Global Guide To M&A - India: by Vivek Gupta and Rohit BerryDocument14 pagesA Global Guide To M&A - India: by Vivek Gupta and Rohit BerryvinaymathewNo ratings yet

- By Graham HoltDocument5 pagesBy Graham Holtwhosnext886No ratings yet

- Due Diligence-Tax Due DilDocument4 pagesDue Diligence-Tax Due DilEljoe VinluanNo ratings yet

- Budget 2017 Bringing India Closer To Global PracticesDocument13 pagesBudget 2017 Bringing India Closer To Global PracticesTaxpert mukeshNo ratings yet

- First Public ConsultationDocument14 pagesFirst Public ConsultationAnonymous UpWci5No ratings yet

- Chapter Seven Tax Planning BackgroundDocument9 pagesChapter Seven Tax Planning BackgroundTriila manillaNo ratings yet

- Tax Planning, Evasion, AvoidanceDocument16 pagesTax Planning, Evasion, AvoidanceDr. Nathan WafNo ratings yet

- Business Taxation: Rachel Griffith, Helen Miller and Martin O'Connell (IFS)Document12 pagesBusiness Taxation: Rachel Griffith, Helen Miller and Martin O'Connell (IFS)anon_241413889No ratings yet

- Transfer PricingDocument111 pagesTransfer PricingMamun0% (1)

- The 15 Action Points BEPSDocument8 pagesThe 15 Action Points BEPSErique Miguel MachariaNo ratings yet

- Aktin PresentDocument12 pagesAktin PresentErin SinagaNo ratings yet

- Tax Aspects of M&ADocument18 pagesTax Aspects of M&AManeet TutejaNo ratings yet

- Solution Advance Taxation Planning and Fiscal Policy Nov 2007Document6 pagesSolution Advance Taxation Planning and Fiscal Policy Nov 2007Samuel DwumfourNo ratings yet

- Week 7 - Tax PlanningDocument38 pagesWeek 7 - Tax PlanningvincentNo ratings yet

- Tax PlanningDocument48 pagesTax PlanningDaniel MartinsNo ratings yet

- Forensic Accounting 16Document6 pagesForensic Accounting 16silvernitrate1953No ratings yet

- income taxDocument9 pagesincome taxAmit Vikram OjhaNo ratings yet

- TAX AssignmentsDocument2 pagesTAX Assignmentsmshafkan7No ratings yet

- Accounting in A Nutshell 4: Deferred TaxesDocument3 pagesAccounting in A Nutshell 4: Deferred TaxesBusiness Expert PressNo ratings yet

- Dividend Tax Cuts 2002 Bush - DamodaranDocument24 pagesDividend Tax Cuts 2002 Bush - DamodarantoddaeNo ratings yet

- Buckwold 21e - CH 1 & 2 Selected SolutionDocument15 pagesBuckwold 21e - CH 1 & 2 Selected SolutionLucyNo ratings yet

- Recognition of Deferred Taxes: RequirementDocument2 pagesRecognition of Deferred Taxes: Requirementbkoi buildersNo ratings yet

- 2 Tax GropDocument3 pages2 Tax GropPeter MNo ratings yet

- IAS Plus: Amendments To IFRS 2 - Vesting Conditions and CancellationsDocument3 pagesIAS Plus: Amendments To IFRS 2 - Vesting Conditions and CancellationsFarhat ParveenNo ratings yet

- Effects of taxationDocument3 pagesEffects of taxationSancrist ChrisNo ratings yet

- Plugin Taxguide 511 Iht BPR Groups Dec 2011Document17 pagesPlugin Taxguide 511 Iht BPR Groups Dec 2011Rashad ShamimNo ratings yet

- Uae Corporate Tax Law SummaryDocument37 pagesUae Corporate Tax Law SummarypankajNo ratings yet

- Lecture 2 - Income TaxDocument13 pagesLecture 2 - Income TaxMasitala PhiriNo ratings yet

- Controlled Foreign Companies: International TaxationDocument4 pagesControlled Foreign Companies: International TaxationEshaan ShindeNo ratings yet

- Ey Ifrs Devel 191 Ias 12 Amendments May 2021aDocument4 pagesEy Ifrs Devel 191 Ias 12 Amendments May 2021aFRANCISCO JAVIER PEREZ CASANOVANo ratings yet

- Tax Treatment of Stocklending/Sale and Repo TransactionsDocument5 pagesTax Treatment of Stocklending/Sale and Repo TransactionsWasis SusilaNo ratings yet

- Introduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirDocument51 pagesIntroduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirPratik100% (1)

- Cambodia Oil Gas Newsletter 8Document4 pagesCambodia Oil Gas Newsletter 8Murad MuradovNo ratings yet

- Chamber of Real Estate and Builders Associations, Inc., v. The Hon. Executive Secretary Alberto Romulo, Et AlDocument6 pagesChamber of Real Estate and Builders Associations, Inc., v. The Hon. Executive Secretary Alberto Romulo, Et AlMathew Beniga GacoNo ratings yet

- Income Tax ConceptsDocument15 pagesIncome Tax ConceptspraveenhukumarNo ratings yet

- Gross Income: Inclusions: Reference Materials: IRS Publication 17-Your Federal Income Tax (2006)Document20 pagesGross Income: Inclusions: Reference Materials: IRS Publication 17-Your Federal Income Tax (2006)sacha_babaoNo ratings yet

- GTS Calculation PDFDocument1 pageGTS Calculation PDFpablo zarateNo ratings yet

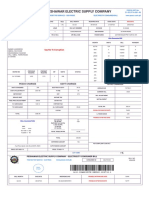

- Pesco Online Billl PDFDocument1 pagePesco Online Billl PDFSaqib RasoolNo ratings yet

- Charge Assumption ReportDocument2 pagesCharge Assumption ReportALi MAlikNo ratings yet

- Economics RP Kartik Goel BBA - LLBDocument21 pagesEconomics RP Kartik Goel BBA - LLBKartikNo ratings yet

- October 2020 Tax AlertDocument5 pagesOctober 2020 Tax AlertRheneir MoraNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

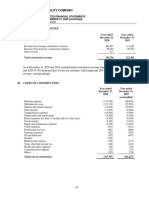

- Comparative Income Statement June OctDocument3 pagesComparative Income Statement June Octnina pascualNo ratings yet

- Q6 Donors TaxDocument7 pagesQ6 Donors TaxGreta DuqueNo ratings yet

- CIR v. BTCDocument7 pagesCIR v. BTCevelyn b t.No ratings yet

- Fort Bonifacio Development Corporation v. CIRDocument34 pagesFort Bonifacio Development Corporation v. CIRAronJamesNo ratings yet

- Peter Fryer, The Battle For Socialism, Socialist Labour League, 1959Document195 pagesPeter Fryer, The Battle For Socialism, Socialist Labour League, 1959danielgaidNo ratings yet

- Income Taxation Notes SummaryDocument6 pagesIncome Taxation Notes SummarySha LeenNo ratings yet

- CREATE Bill Impact on Philippine Company TaxesDocument8 pagesCREATE Bill Impact on Philippine Company TaxesHanee Ruth BlueNo ratings yet

- RMC No. 50-2018 WTWDocument21 pagesRMC No. 50-2018 WTWAris Basco DuroyNo ratings yet

- "Azvirt" Limited Liability Company: 25. Construction RevenueDocument1 page"Azvirt" Limited Liability Company: 25. Construction RevenueŞeyxəli ŞəliyevNo ratings yet

- Final Presentation Con WorldDocument13 pagesFinal Presentation Con WorldMarjorie O. MalinaoNo ratings yet

- Invoice 1708 Narendra Goud Narendra GoudDocument1 pageInvoice 1708 Narendra Goud Narendra GoudNarendra GoudNo ratings yet

- Philippine History and Government Prelim ExamDocument5 pagesPhilippine History and Government Prelim ExamLouisse Del CastilloNo ratings yet

- The Liquid Chemical Company Manufactures and Sells A Range ofDocument2 pagesThe Liquid Chemical Company Manufactures and Sells A Range ofAmit PandeyNo ratings yet

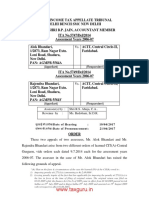

- Alok Bhandari Anr. vs. ACIT ITAT DelhiDocument7 pagesAlok Bhandari Anr. vs. ACIT ITAT DelhivedaNo ratings yet

- Estate Tax and Donor's Tax ComputationDocument8 pagesEstate Tax and Donor's Tax ComputationHeidi KaterineNo ratings yet

- Battle of PlasseyDocument2 pagesBattle of PlasseyD MartinNo ratings yet

- Ey Worldwide Corporate Taxguide 01sept2021Document2,012 pagesEy Worldwide Corporate Taxguide 01sept2021Michael BoulesNo ratings yet

- GST Advance Ruling ProcedureDocument5 pagesGST Advance Ruling ProcedureSaumya AllapartiNo ratings yet

- Manila Memorial Park, Inc v. Secretary of DSWD, 711 Scra 302Document1 pageManila Memorial Park, Inc v. Secretary of DSWD, 711 Scra 302Mary Louis SeñoresNo ratings yet

- Earnings Withholding Order For Taxes: Franchise Tax BoardDocument2 pagesEarnings Withholding Order For Taxes: Franchise Tax BoardMoh SaadNo ratings yet

- On January 1 2010 Pele Company Purchased The Following Two PDFDocument1 pageOn January 1 2010 Pele Company Purchased The Following Two PDFAnbu jaromiaNo ratings yet

- Case DigestDocument2 pagesCase DigestBHEJAY ORTIZNo ratings yet

- LifeBlood - Assessment Process Tax 2Document17 pagesLifeBlood - Assessment Process Tax 2Monjid AbpiNo ratings yet

- IRS Seminar Level 2, Form #12.032Document313 pagesIRS Seminar Level 2, Form #12.032Sovereignty Education and Defense Ministry (SEDM)100% (1)